US TSYS: Post Data React Update

Jul-17 13:00

- Treasuries have completely recovered from post-data sell-off, currently mixed with Bonds leading rebound at the moment, 2s through 10s down 1-2, Bonds/ultra-bonds +1-3.

- Curves flatter: 2s10s -1.483 at 54.458, 5s30s -.845 at 100.801.

- Cross asset: Bbg US$ index still bid, +4.55 at 1208.66 -- off initial post-data high of 1210.75; stocks gaining (SPX eminis +9.50 at 6312.75); gold unwinds yesterday's gains currently -36.00 at 3311.20.

- Fed speak at 0915ET: Fed Gov Kugler on housing market, economic outlook

- Next data at 1000ET: NAHB Housing Market Index and Business Inventories

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Small Hawkish Fed Repricing As Ctrl Group Outweighs Headline Retail Sales

Jun-17 12:59

Initial dovish market readthrough from the softer-than-expected headline retail sales data & negative revisions is more than countered by the firmer-than-expected retail sales control group reading (and positive revision) and firmer-than-expected import prices (which will have been influenced by the weaker USD).

- That leaves Fed Funds pricing 0bp of cuts for this month, 3bp through July, 18bp through September, 31.5bp through October and 48bp through December.

- This compares to 0bp, 3.5bp, 19.5bp, 32.5bp and 49.5bp ahead of the release.

- SOFR implied terminal rate pricing (SFRZ6) stands at 3.30% vs. 3.29% ahead of the data. Contract sticks comfortably within the 3.165-3.500% implied rate range in play since May 9.

MNI: US REDBOOK: JUN STORE SALES +5.0% V YR AGO MO

Jun-17 12:55

- MNI: US REDBOOK: JUN STORE SALES +5.0% V YR AGO MO

- US REDBOOK: STORE SALES +5.2% WK ENDED JUN 14 V YR AGO WK

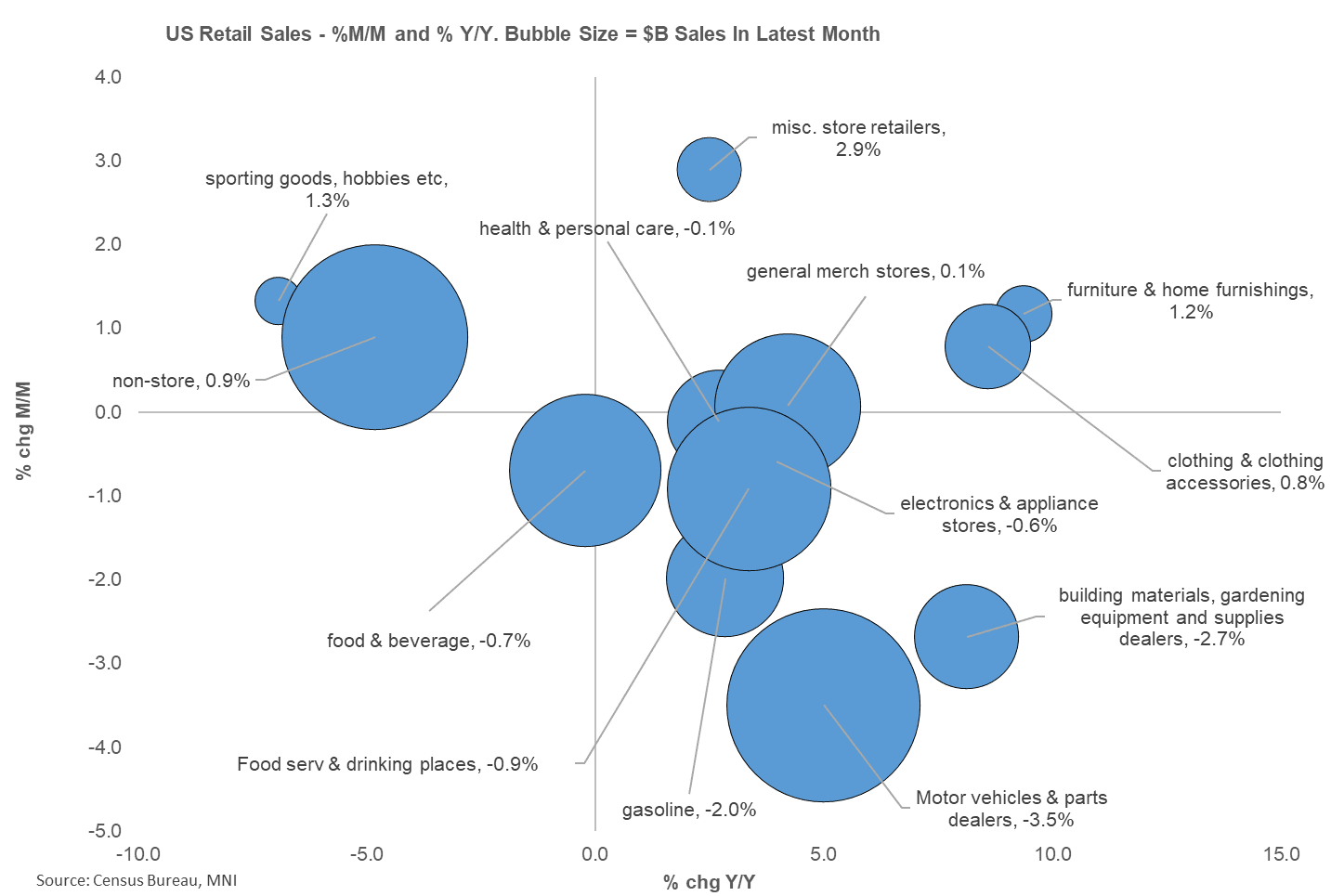

US DATA: Control Group Flatters Mixed Retail Sales Report

Jun-17 12:51

May saw the biggest month-to-month drop in retail sales (-0.91% M/M SA unrounded, vs -0.6% consensus and -0.1% April rev from +0.1%) since March 2023, with ex-autos/gas weaker than expected (-0.1% vs +0.3%) and surprisingly decelerating from April (0.1%, rev down from 0.2%). Likewise, ex-auto sales unexpectedly fell, by 0.3% (+0.2% expected, 0.0% prior rev down from 0.1%).

- Bucking the trend was the closely-watched Control Group, which rose more than expected at 0.4% (0.3% consensus), with prior revised up (April -0.1%, from -0.2%).

- The reason for the Control Group "beat" was the poor performance of several major categories of retail sales that aren't included in Control: vehicle sales, which dropped the fastest in 11 months at 3.9% M/M in line with expectations for a sharp decline (-0.6% prior); gasoline sales, which fell 2.0% (-0.7% prior) also as expected given 2.6% CPI deflation in this category; building materials/gardening sales, which fell 2.7% M/M for the biggest decline in 16 months (0.3% prior); and food services and drinking places, whose fall of 0.9% (biggest drop in 27 months) looks to have been unexpected, versus strength in the prior two months.

- The pullback in restaurant sales is somewhat concerning from a discretionary spending perspective, though of course all of the individual series are volatile. But the Control Group performance flatters the broader report in terms of gauging the health of consumption. Motor Vehicles/Parts and Food Services/Drinking Places, plus Food/Beverage stores (-0.7%) are three of the top four categories of retail sales by size making up 60% of the total, and each contracted.

- The standout was on the upside was non-store retail, the second-largest category, which impressed with 0.9% M/M gains; the smaller categories of clothing (+0.8%), miscellaneous scores (+2.9%), furniture (+1.2%) sporting goods (+1.3%) which were all arguably tariff-impacted categories saw gains albeit largely in a rebound from a poor month or two prior, though electronics stores (-0.6%) weakened.