USD: Positive US Data Surprises Point To More USD Support In The Near Term

Thursday's session delivered positive US data surprises across a number of releases. Retail sales was well above expectations, while initial jobless claims ticked lower and the Philly Fed business outlook surged back to Q1 levels. The Citi US economic surprise index is now back close to May highs and this index is generally outperforming equivalent readings for other major economies/region. In turn this points to more support for the USD, all else equal in the near term.

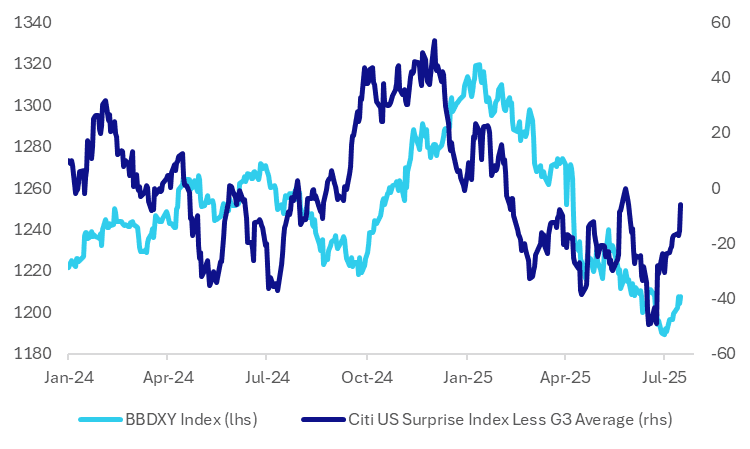

- The first chart below plots the differential between the US Citi surprise index and an unweighted average of the surprise indices for the EU area, China and Japan, against the USD BBDXY index.

- At face value improved US data outcomes are evident, relative to expectations, compared with the other major economies/regions. The differential troughed before the recent bottoming in the USD index.

- This differential is approaching 0, but is well off late 2024 levels, when US data was consistently outperforming.

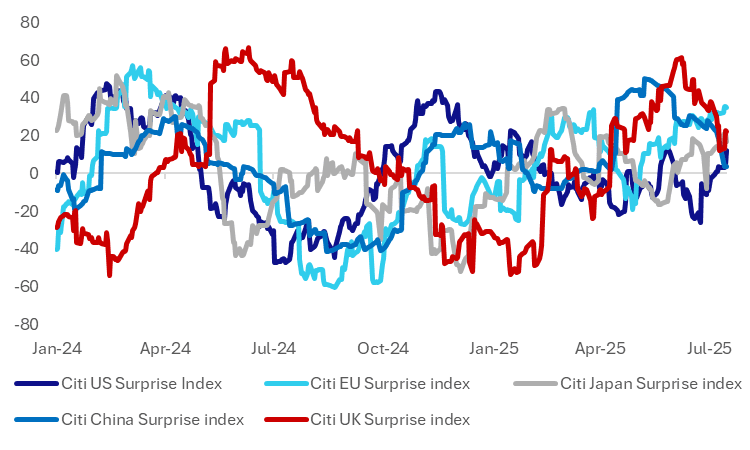

- The second chart below plots the trends for the major Citi surprise indices, with the UK index added as well. The US index is improving from a low base, while readings for China and the UK have fallen from elevated levels. The EU reading continues to track higher, but in relative terms, the US reading has risen more quickly in recent weeks.

- The caveat with this backdrop from a broader USD standpoint assumes we continue to see relative data outperformance, while the status quo is maintained from a Fed standpoint. This reflects both the near term policy outlook, along with Fed Chair Powell staying in the current role (as earlier this week demonstrated, an abrupt sacking of Powell is likely to be USD negative). The other watch point will Aug 1 tariff outcomes/trade negotiations.

- The broader market consensus is also for USD weakness over the medium term.

Fig 1: USD BBDXY Versus Citi US -G3 Surprise Index Differential

Source: Citi/Bloomberg Finance L.P./MNI

Fig 2: Citi Economic Surprise Indices By Major Economy/Region

Source: Citi/Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Richer With US Tsys, Risk-Off As US Weighs Greater Involvement

ACGBs (YM +3.0 & XM +3.0) are modestly stronger after US tsys finished with a bull-flattener.

- Yesterday, President Trump cut short his appearance at the G7 leaders’ summit.

- Pres Trump: "We know exactly where the so-called “Supreme Leader” is hiding. He is an easy target, but is safe there - We are not going to take him out (kill!), at least not for now."

- Otherwise, markets await Wednesday's FOMC policy announcement.

- US Retail sales fell for a second month, down 0.9% m/m in May as lower auto sales dragged down the headline figure – a reversal of prior front-loaded tariff-related gains — but even the ex-auto sales and gas figure fell 0.1% m/m.

- Cash ACGBs are 3bps richer with the AU-US 10-year yield differential at -16bps.

- The bills strip has bull-flattened, with pricing flat to +3.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in July is given an 85% probability, with a cumulative 78bps of easing priced by year-end.

- Today, the local calendar will see the Westpac Leading Index. May's jobs data is on Thursday.

- The AOFM plans to sell A$900mn of the 2.75% 21 June 2035 bond today and A$800mn of the 1.00% 21 December 2030 bond on Friday.

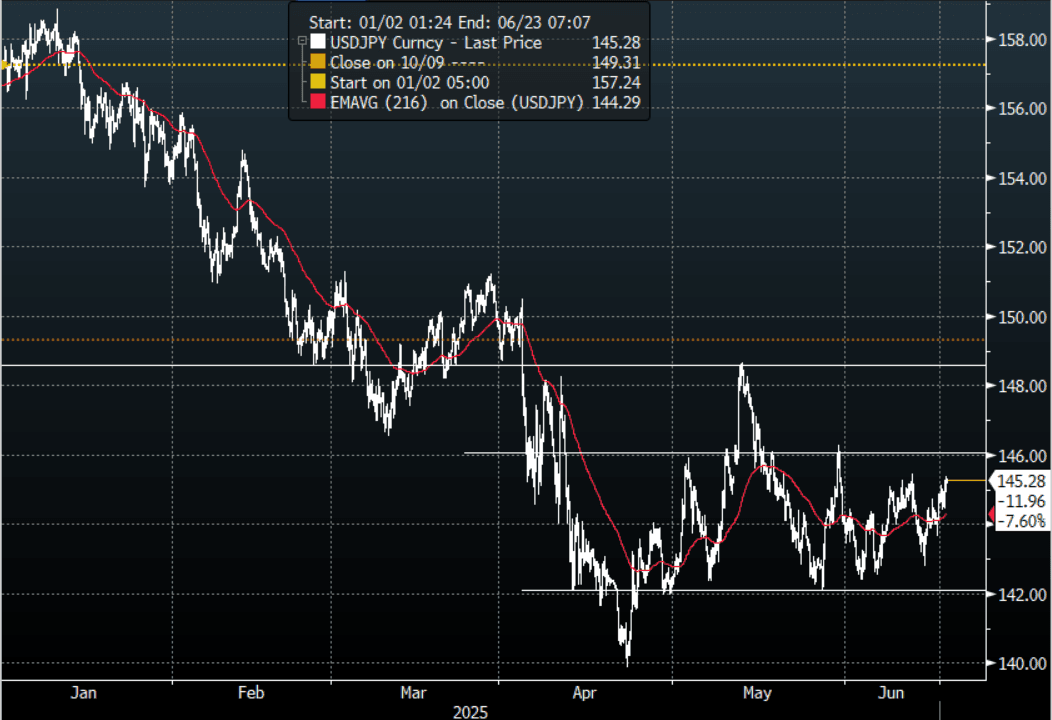

JPY: USD/JPY - Price Action Hints At A Market Long JPY

The overnight range was 144.41 - 145.38, Asia is currently trading around 145.35. With the USD bouncing across the board as risk digests the potential of the US entering the fray in the middle east, the long JPY positions continue to be challenged. You would normally expect the JPY to outperform in this scenario but the outsized move in oil and a market that is already positioned very long is providing headwinds to the trade.

- (Bloomberg) - “US President Donald Trump and Japanese Prime Minister Shigeru Ishiba failed to reach an agreement on a trade package on the sidelines of the Group of Seven summit, an outcome that leaves the Asian notation inching closer to a possible recession as the pain of US tariffs hits its economy."

- “Setting aside the human tragedy, the Israel-Iran clash poses serious upside risk to Japan’s inflation. The spike in oil prices has likely caught the Bank of Japan off guard — just as it was counting on easing energy costs to temper consumer-price pressures. Japan depends on oil for about 35% of its energy needs and sources nearly all of its crude from the Middle East.”(BBG)

- USD/JPY found decent demand yesterday every time it had a look towards the 144.50 area. This price action stands out considering the risk backdrop and could hint at a market that is already very long JPY.

- Price is back in its recent 142.00 - 147.00 range and will need a break either side of that to get a clearer direction.

- The market is clearly looking for a move lower in USD/JPY but with positioning quite large now we have seen the risk of pullbacks increase. A break above 147.00 would be needed to challenge the conviction of any shorts.

- Options : Close significant option expiries for NY cut, based on DTCC data: 144.00($725m). Upcoming Close Strikes : 146.00($1.92b June 20), 143.00($925m June 20)

- CFTC data shows Asset managers maintained their already extensive JPY longs, leveraged funds looked to have pared back their own longs once more.

Data/Event : Trade Balance, Core Machine Orders

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

BONDS: NZGBS: Little Changed Despite Risk-Off Rally In US Tsys

In local morning trade, NZGBs are little changed, with the NZ-US 10-year yield differential 4bps wider, after US tsys finished with a bull-flattener.

- Rising Middle East tensions, including the possibility that the US will join the war, lent risk-off support for US tsys on Tuesday.

- Pres Trump: "We know exactly where the so-called “Supreme Leader” is hiding. He is an easy target but is safe there - We are not going to take him out (kill!), at least not for now. But we don’t want missiles shot at civilians, or American soldiers. Our patience is wearing thin. Thank you for your attention to this matter!"

- Otherwise, markets await Wednesday's FOMC policy announcement.

- NZ’s current account deficit narrowed to NZ$2.32 billion in the first quarter (-NZ$2.2 billion est). The current account deficit was 5.7% of GDP in the 12 months through March, narrowing from a revised 6.1% in Q4.

- Swap rates are little changed.

- RBNZ dated OIS pricing is little changed across meetings. 4bps of easing is priced for July, with a cumulative 27bps by November 2025.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 2.75% Apr-37 bond and NZ$50mn of the 2.75% May-51 bond.