EM ASIA CREDIT: POSCO Holdings: Serious safety issue at Posco factory

(POHANG, Baa1/A-neg/NR)

"1 KILLED, 3 INJURED AS SUSPECTED TOXIC GAS LEAKS AT POSCO PLANT IN SOUTH KOREA" - BBG

The situation is reported to be under control, though the cause is still unknown. There will be an investigation to determine if there were any safety breaches.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BUND TECHS: (Z5) Corrective Cycle Still In Play

- RES 4: 129.50 High Aug 5

- RES 3: 129.44 High Sep 10 and key short-term resistance

- RES 2: 129.13 High Sep 17

- RES 1: 128.84 61.8% retracement of the Sep 10 - 25 bear leg

- PRICE: 128.44 @ 05:42 BST Oct 6

- SUP 1: 128.24/127.88 Low Oct 1 / Low Sep 25

- SUP 2: 127.61 Low Sep 3 and the bear trigger

- SUP 3: 127.46 1.00 proj of the Aug 14 - 15 - 28 price swing

- SUP 4: 127.13 1.236 proj of the Aug 14 - 15 - 28 price swing

Bund futures are holding on to the bulk of their latest gains. The recent climb appears corrective. Key support and the bear trigger lies at 127.61, the Sep 3 low. Clearance of this level would confirm a continuation of the medium-term bear cycle. For bulls, a clear reversal higher would refocus attention on key resistance at 129.44, the Sep 10 high. First resistance is 128.84, 61.8% of the Sep 10 - 25 bear leg.

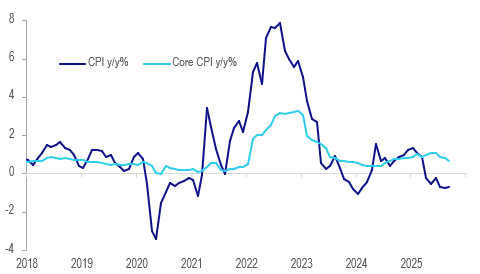

THAILAND: Rate Cut Likely On Weak Growth & Disappointing September CPI

September Thai inflation was lower than expected with headline printing at -0.7% y/y after -0.8% and core at +0.65% y/y following August’s +0.8%. The Bank of Thailand decision is announced Wednesday, the first with new pro-growth Governor Vitai, and it is widely forecast to cut rates 25bp to 1.25%. The soft September CPI print along with lacklustre growth reinforces those expectations.

- Core inflation was its lowest in just over a year despite 100bp of easing begun in October 2024 as domestic growth remains weak. Government energy subsidies and lower food prices from good harvests pushed headline into negative territory where it has been for six straight months.

- Consumer data have generally been soft with August with consumer confidence falling to its lowest since December 2022, July private consumption down 0.3% y/y and August tourist arrivals contracting 12.8% y/y. Q2 real consumption growth slowed to 2.1% y/y from 2.5%. Recent political instability has been unhelpful but the new government is looking at ways to support households although it has also promised new elections.

- There was downward pressure on core inflation from clothing, housing, and personal & medical care.

Thailand CPI y/y%

Source: MNI - Market News/LSEG

JGBS: Curves Steeper, But Sub Recent Highs, 30yr Debt Auction Tomorrow

All the action today has away from the 10yr JGB, which has been fairly steady, last near 1.67%. The front end is weaker, back end firmer in yield terms as markets have moved to price in less BoJ hike risks, as well greater fiscal uncertainty. The 2/10s curve was last +76.5bps, +4.5bps for the session, while the 2/30s was +239bps, up 17bps.

- We noted earlier after the initial adjustment to Takaichi's victory, sentiment may stabilize and await cabinet announcements and early policy outcomes before taking the curve to fresh highs. The early Sep high for 2/30s was +245bps. The 30yr outright was last 3.30%, the 40yr 3.53%, while the 2yr was near 0.91%.

- These moves have largely been mirrored in the swap space, although yield moves haven't been as large at the back end (with JGBs likely more susceptible to fiscal policy concerns).

- BoJ tightening risk has fallen dramatically for Oct, with just 6bps of tightening priced in against recent highs of 17bps, as Takaichi stated the government and BoJ should be coordinated on economic policy. Takaichi has been a critic of BoJ hikes in the past (but her rhetoric wasn't as strong during this most recent LDP leadership campaign).

- JGB futures are back to flat, last 135.93, +.02, but well off earlier highs of 136.53.

- Note tomorrow, we get on the data front, Aug Household spending prints. Greater focus will be on 30yr dent auction, the first test for the new Takaichi regime.