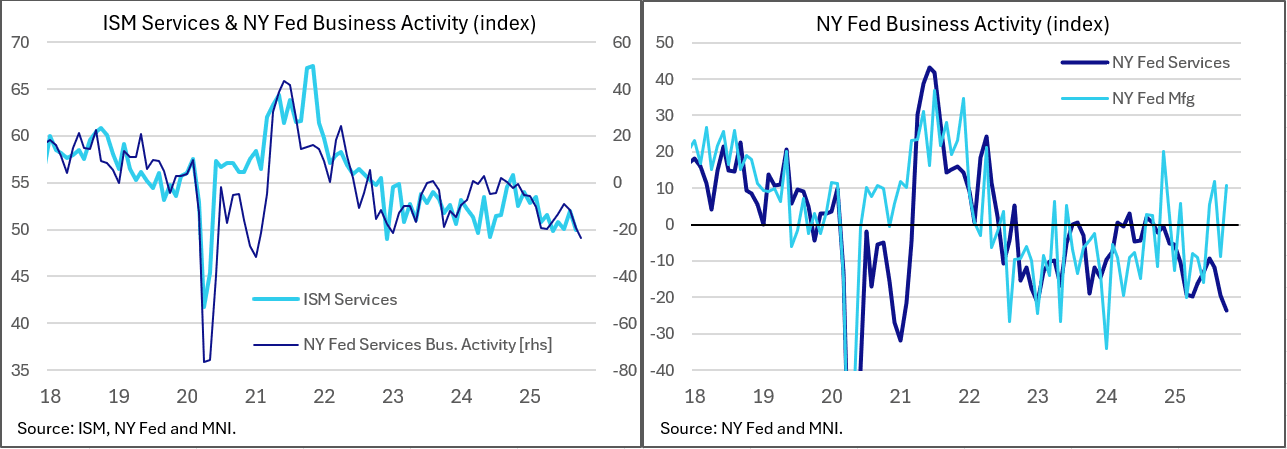

US DATA: Poor NY Fed Services Report A Warning Signal For Activity

The New York Fed's Business Leaders Survey showed a sharp pullback in activity in October, with the headline business activity index dropping to -23.6 from -19.4. That marks the lowest reading since January 2021, and the the 3rd consecutive month of deterioration.

- The survey was weak across the board, with the business climate moving more negative, and various sub-categories also poor: "Employment edged lower, and wage growth remained modest. Supply availability continued to worsen....On the whole, firms were slightly pessimistic about the outlook."

- The latest NY Fed submission to the Federal Reserve Beige Book reflected weakness through the September reporting period, but this now seems to have worsened. "Activity in the service sector continued to decline moderately this period. Firms in the retail, leisure and hospitality, and business services sectors reported moderate declines, and firms in the information sector reported a particularly sharp contraction."

- We would never want to read much into a single report. But this is the first regional Fed services survey of the month, and with government data in short supply, this is a bit of a warning signal for near-term activity. The general direction of the NY Fed survey tends to align with broader national ISM Services trends. And the decoupling with manufacturing - which in the corresponding NY Fed survey fared better in October - is also an interesting development.

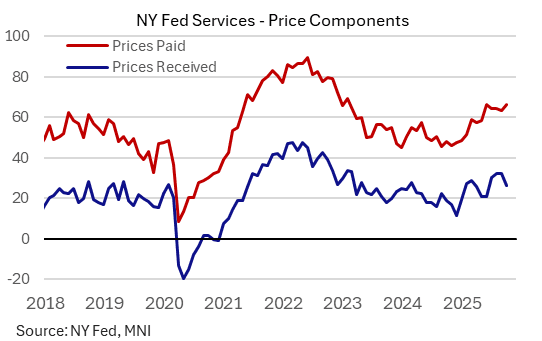

- The current prices paid gauge rose to 66.4 from 63.2, fully reversing 3 consecutive declines to post the highest since June (and 2nd highest since early 2023). Prices received however pulled back, to 26.4 from 32.2 for a 4-month low. We caution not to read too much into month-to-month moves but overall it seems that regional services firms haven't been able to aggressively raise prices paid by clients. The NY Fed Beige Book entry noted of the broader regional business sector, "The pace of price increases was mostly unchanged; selling prices continued to rise moderately while input prices again rose strongly."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Back Near Pre-Retail Sales Levels After Two-Way Moves

- Treasuries have on the whole pushed back to pre-retail sales levels, having sold off on the stronger than expected release before what was a hard to square away rally shortly after.

- The recent losses go against S&P 500 futures holding and recently extending their intraday decline, after earlier losses initially appeared to be supporting the bid in bonds.

- TYZ5 is back to 113-12+ (-02+) from an earlier high of 113-18, having seen a post-0830ET data low of 113-08+. Cumulative volumes are on the low side again, having just nudged over 800k.

- Resistance remains at 113-29 (Sep 5 high), as part of a bullish trend sequence, whilst support is seen at 112-25+ (20-day EMA).

- Cash yields range from 1bp lower (2s) to 1bp higher (10s and 20s) on the day, with 20s continuing to modestly underperform with upcoming supply.

- $13bn 20Y re-open at 1300ET (912810UN6). Last week’s 30Y auction was on the screws but with stronger details. That’s in contrast to last month’s 20Y auction which was in-line but with the bid-to-cover slipping from 2.79 to 2.54 and indirect take-up dropping from 67.4% to 60.6%.

- Beyond retail sales, the day’s data was mixed with stronger import prices partly offset by further large downward revisions to prior months, with a similar story for IP and a surprisingly soft NY Fed services survey.

MNI EXCLUSIVE: EU Officials On Inflation Implications From CO2 Trading Scheme

European officials and parliamentarians look at the implications of ETS2 CO2 trading rules for inflation. -- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

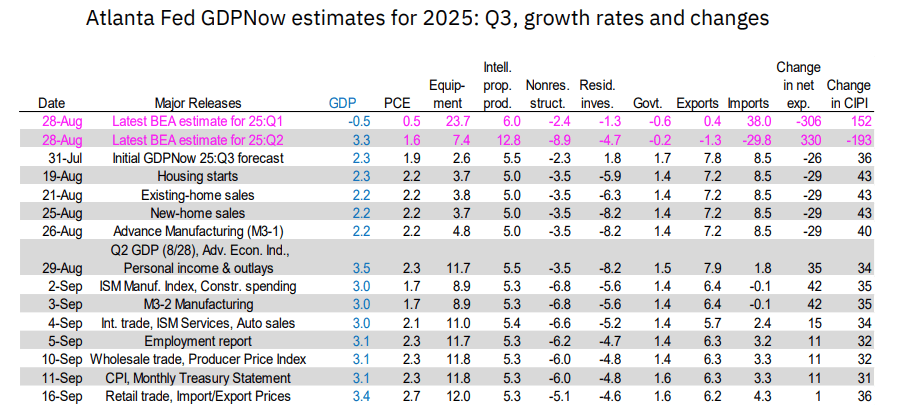

US OUTLOOK/OPINION: GDPNow Suggests Pickup In Private Domestic Demand In Q3

The Atlanta Fed's latest GDPNow estimate for Q3 jumped to 3.41% from 3.09% in the last full update on September 10 (and 3.3% posted in Q2). This was very much a domestic demand-driven upgrade, with real PCE now seen contributing well over half of growth (1.85pp vs 1.54pp in the previous estimate) thanks to better-than-expected advance retail sales.

- The underlying details from the GDPNow estimate imply final sales to private domestic purchasers, closely watched by the Fed, is growing at around 2.4%, a pickup after 1.9% in both Q1 and Q2.

- "After recent releases from the US Census Bureau, US Bureau of Labor Statistics, and Treasury's Bureau of the Fiscal Service, the nowcasts of third-quarter real personal consumption expenditures growth and real gross private domestic investment growth increased from 2.3 percent and 6.2 percent, respectively, to 2.7 percent and 6.9 percent, while the nowcast of the contribution of net exports to third-quarter real GDP growth decreased from 0.23 percentage points to 0.08 percentage points."

- The next release will be Wednesday after housing starts/permits data.