US: POLITICAL RISK: Daily Brief 11 Dec-25

Dec-11 13:23

Download Full Report Here

Executive summary:

- The Trump administration and Pentagon have potentially taken another step towards all-out war with Venezuela following the attempted seizure of an oil tanker off the coast of the country.

- Two notable votes take place today in the Senate regarding the status of Obamacare subsidies, which at present are due to expire in January 2026. Neither is likely to have the requisite support, raising the likelihood of the expiration of the subsidies. Discharge petitions in the House on the same issue risk further blowback on Speaker Mike Johnson (R-LA) amid an increasingly restive House Republican Conference.

- Secretary of Homeland Security Kristi Noem appears before the House Committee on Homeland Security today at 10:00ET 15:00 GMT to deliver testimony on the topic of “Worldwide Threats to the Homeland”. However, Beltway reporting suggests that threats to Noem may be closer to home, with rumours she could be removed/asked to leave office in the new year.

- Poll of the Day: Latest polling from Maine shows a dead-heat ahead of a must-win contest if the Democrats want to flip control of the Senate in 2026

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Weekly ADP Employment React

Nov-11 13:22

- Treasuries extending recent highs after weekly ADP "employment pulse" data comes out weaker than expected.

- Currently, the Dec'25 10Y contract trades +6.5 at 112-28.5 (H). A short-term bear theme in Treasuries remains in place, however.

- Attention is on a reversal trigger at 112-06, the Sep 25 low, and the 100-DMA, at 112-08. A clear break of these price points would expose a trendline support at 112-02. The trendline is drawn from the May 22 low. Resistance to watch is 113-02, the Nov 5 and 7 high. Clearance of this level would highlight a potential bullish reversal.

- Bbg US$ index dips -0.24 at 1218.47; SPX eminis softer -13.75 at 6843.0.

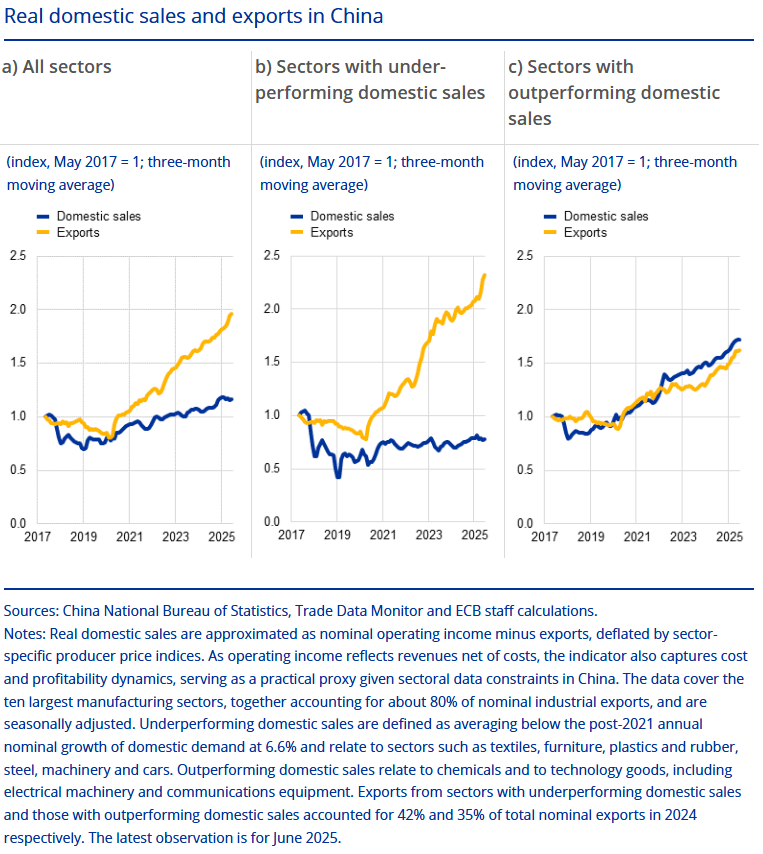

INTERNATIONAL TRADE: Weak Chinese Domestic Demand Weighs On EZ Trade Balance-ECB

Nov-11 13:00

MNI (London) - China's weak domestic demand rather than U.S.-China trade tensions is the key factor for the strong rise of exports to Europe and the stagnation of imports, the European Central Bank published in its latest Economic Bulletin on Tuesday.

- China’s real estate downturn and policies promoting self-reliance under “Made in China 2025” have eroded household demand and curbed imports, particularly of consumer and intermediate goods, with weak domestic sales and falling export prices prompting firms to seek foreign markets - notably in sectors such as motor vehicles and steel, where exports have grown by about 75% since 2022, the ECB said.

- The Bulletin adds to previous reports (1, 2) suggesting China has built significant manufacturing overcapacity in recent years, indicated by domestic supply rising faster global demand, rising numbers of lossmaking industrial firms in the country, as well as declining capacity utilization, which may weigh on demand for German products.

- Back to more specific EU implications from today's study: "Weak domestic demand appears to be the missing link in explaining China’s strong exports to Europe – more so than tariff-related trade diversion. Escalating trade tensions between the United States and China might result in a further diversion of Chinese exports to Europe. However, the rise in China’s exports to the EU predates the latest tensions and coincides instead with the onset of weakness in domestic demand in China."

- In 4Q24 "the average monthly value of domestic sales was around four times higher than total exports and over 28 times larger than exports to the United States. This suggests the pool of goods that could be redirected to the EU is much broader than trade data alone would suggest. Redirecting even a small share of domestic sales abroad could boost overall exports – including to the EU – more than a sizeable diversion of exports from the United States."

BOE: VIEW CHANGE: J.P.Morgan Add One More Cut To Call, Terminal Seen At 3.50%

Nov-11 12:59

J.P.Morgan now expect three more BoE rate cuts, coming in December, March, & June, which would leave the terminal rate at 3.25% (previously they looked for cuts in February & April, to a terminal rate of 3.50%).

- They note that “clearer evidence of slack helps the case for more easing, but growth resilience and sticky forward-looking pay are likely to remain a constraint on the pace and magnitude””.