POWER: Poland's Front Month Climbs to Fresh All-Time High

Poland’s January continued to climb on the back of price increases in European coal and below seasonal temperatures throughout most of January. However, price falls in EU ETS limited rise.

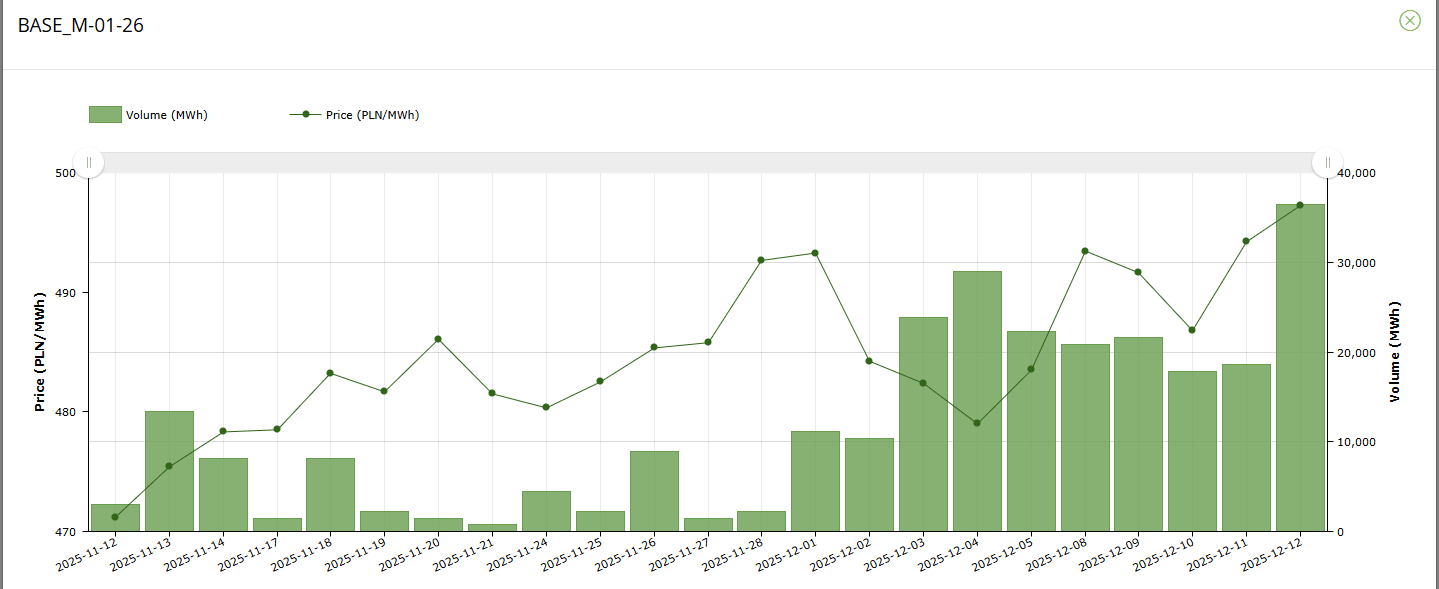

- Poland’s January baseload power settled at PLN497.24/MWh compared to its settled price of PLN494.20/MWh on 11 December, according to data on Polish power exchange TGE.

- EUA DEC 26 down 0.2% at 85.99 EUR/MT

- Rotterdam Coal JAN 26 up 0.2% at 95.35 USD/MT

- EUAs Dec25 are rangebound today and are on track for weekly gains of about 2.7%, reaching the highest level since Oct 2023, amid bullish sentiment ahead of tightening supply in 2026.

- Mean temperatures in Warsaw were mixed, with upward revisions over 1-10 January and downward revisions noted over 11-25 January. Despite this, temperatures are expected to be mostly below the seasonal norm throughout the period, ranging between -2.6C and -0.9C.

- The 630MW Plock power plant will still be disconnected over 9-24 January. However, works at other key power plants will be limited over the month, keeping supply firm.

- Closer in, average temperatures in Warsaw were mostly revised higher over 13-17 December. Despite this, temperatures are expected to be above the seasonal norm throughout most of the 14-day ECMWF forecast – only flipping below on 26 December.

- The 910MW Jaworzno 2 power plant unplanned 230MW curtailment will still last until 20 December before fully returning to the grid the next day, latest Remit data show.

- The day-ahead dropped to PLN448.49/MWh for Saturday delivery from PLN539.37/MWh for Friday amid typically lower weekend power demand.

- However, wind is expected at 16% load factor tomorrow compared to 29% today, which placed a floor on costs.

Looking ahead, wind is anticipated to be at a 2.53GW, or a 27% load factor on 15 December (Mon) – which could cap rises is spot costs from increased demand from the weekend.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OIL: Fallout From OPEC+ Report Still Driving Crude Weakness

Weakness in crude benchmarks has extended through the afternoon, with Brent futures now down over 2.5% on the session at ~$63.50. As noted in earlier posts, the trigger for the selloff has been the latest Monthly Oil Market report from OPEC+. The report pointed to a market surplus forming in Q3, contrary to prior expectations for a deficit.

- Our commodities team notes that OPEC has typically been the most bullish vis a vis supply-demand fundamentals and the Q3 surplus reinforces concerns for an oversupplied market.

- Initial support in COF6 is the November 6 low at $62.84, which shields the bear trigger at $59.97 (Oct 20 low).

GILTS: Off Pullback Lows, Bulls Remain In Control

Gilts draw support from the bid in EGBs and cross-market inputs (oil lower & equities off highs) detailed in recent bullets.

- Bears failed to close yesterday’s opening gap higher in futures and the technical picture in the contract remains bullish, with key resistance located at 93.98.

SOFR OPTIONS: Midcurve Put strip

2QX5 96.75/96.68p strip, bought for half in 4k.