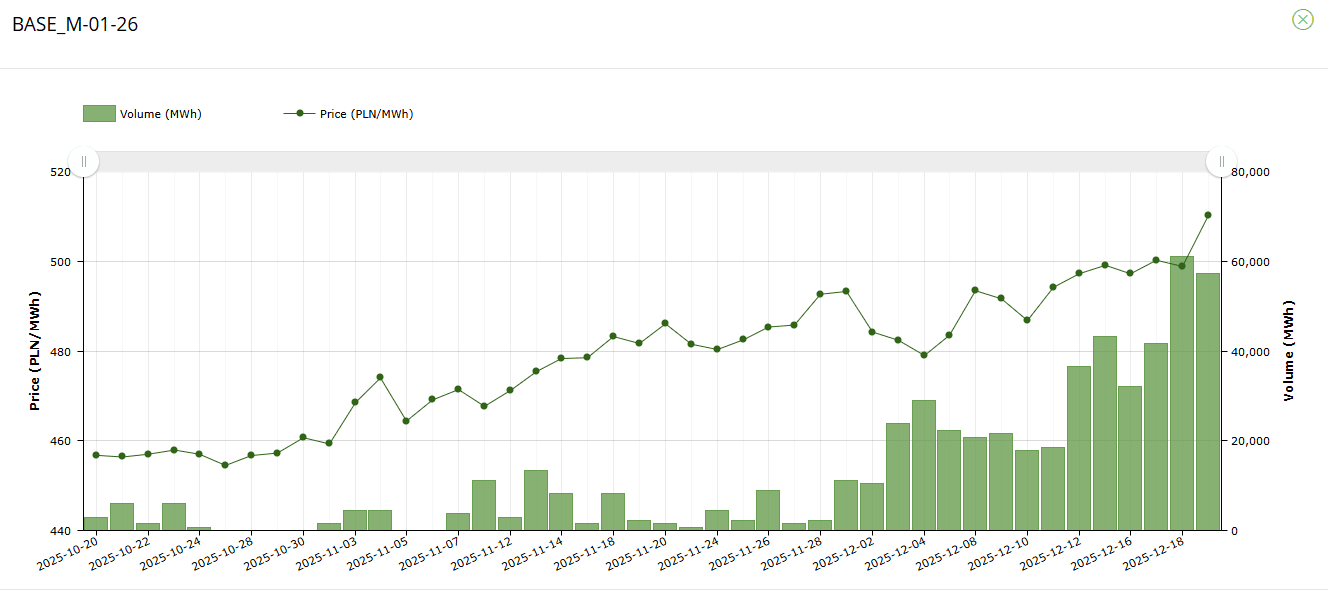

POWER: Poland's Front Month Breaks PLN500/MWh Level Again, Hits Fresh High

Poland’s January rebounded to end sharply higher on the week and break the PLN500/MWh level for the second time to reach a fresh all-time high amid revised lower temperatures, with firm European coal and EU ETS price lending some support.

- Poland’s January baseload power settled at PLN510.22/MWh compared to its settled price of PLN498.83/MWh on 18 December, according to data on Polish power exchange TGE.

- EUA DEC 26 up 0.5% at 86.93 EUR/MT

- Rotterdam Coal JAN 26 down 0.2% at 96 USD/MT

- UKAs are tracking a sharp weekly increase with optimism towards the UK-EU ETS linkage and lower free allowances in 2026. EUAs are edging higher today, while tracking a small weekly increase.

- The 630MW Plock power plant will still be disconnected over 9-24 January, while the 670MW Gryfino unit 9 at the 1.34GW Gryfino power plant will be still be offline over 1-5 January.

- However, works at other key power plants will be limited over the month, still keeping supply firm.

- Average temperatures in Warsaw were mostly revised lower over 1-31 January and are still expected to be below the seasonal throughout the entirety of January, reaching as low as -4.5C compared to -4C in the previous forecast yesterday.

- Closer in, average temperatures in Warsaw were mostly revised lower over 20-24 December by as much as 0.8C. Temperatures are expected to be below the seasonal norm throughout the 14-day ECMWF forecast – albeit all temperatures will remain above negative.

- The 910MW Jaworzno 2 power plant unplanned 230MW curtailment will still last until 21 December, extended from 20 December, while the 474MW Patnow power plant will have unplanned works over 25-31 December.

- The day-ahead rose to PLN506.68/MWh for Friday delivery from PLN427.73/MWh for Friday amid wind expected at 14% load factor tomorrow compared to 42% today.

Looking ahead, wind is anticipated to be at a 1.14GW, or a 12% load factor on 22 December (Monday) – which could have limited impact on rising costs due to higher power demand from the weekend.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SWAPS: Pressure On Gilt Swap Spreads Extends

Underperformance for gilts vs. swaps extends further in recent trade, indicating increased fiscal and political risk premium in light of overnight reports questioning the long-term prospects of PM Starmer leading the Labour Party.

- The rally in wider risk assets will also be factoring in.

- 30-Year swap spreads now set for the lowest close since October 14, ~8bp off cycle closing highs registered in late October.

- Clean downside extension through the October 14 closing level (-85.77bp) would switch focus to the September closing low (-90.14bp).

PIPELINE: Corporate Bond Update - No Jumbos Today

- Date $MM Issuer (Priced *, Launch #)

- 11/19 $Benchmark Avalon Bay 5Y +95a

- 11/19 $500M VSP Optical WNG 10Y +170

- 11/19 $Benchmark Element Fleet 5Y +125a

- 11/19 $Benchmark SMBC Aviation 10Y +145a

- 11/19 $500M FIBRA Prologis WNG 10Y +170a

- 11/19 $Benchmark EOG Resources +5Y, 30Y tap

- 11/19 $Benchmark Bangkok Bank 5Y +115a, 10Y +130a

- 11/19 $Benchmark Western Alliance Bank 10NC5 +312a

- 11/19 $Benchmark Baxter 3Y +130a, 5Y +155a, 10Y +185a

- 11/19 $Benchmark First Abu Dhabi Bank (FAB) investor calls

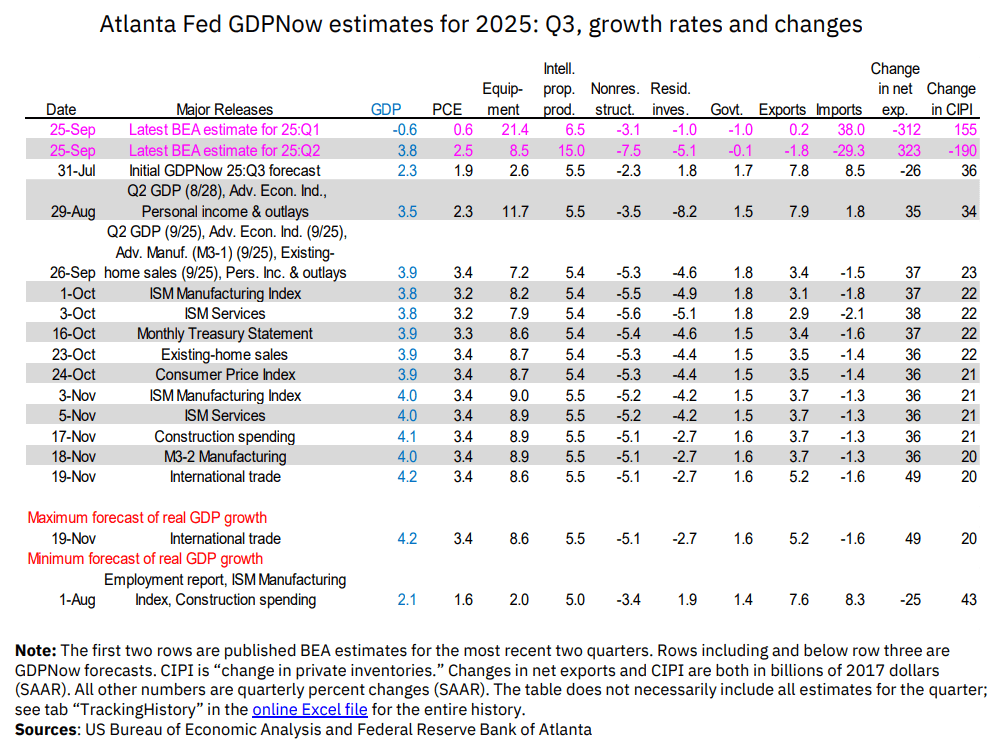

US DATA: Atlanta Fed GDPNow Sees Cycle High 4.2% GDP In Q3

The Atlanta Fed's GDPNow estimate for Q3 is now up to a cycle high 4.23% Q/Q SAAR - up from 4.05% prior. That is the highest estimate yet for Q3 from the Atlanta Fed, and if their model is correct, it would be the strongest since Q3 2023.

- "After recent releases from the US Census Bureau and the US Bureau of Economic Analysis, a decrease in the nowcast of third-quarter real gross private domestic investment growth from 4.9 percent to 4.8 percent was more than offset by an increase in the nowcast of the contribution of net exports to third-quarter real GDP growth from 0.57 percentage points to 0.78 percentage points."

- Indeed inventories and net exports make up 1.11pp of that growth, so final domestic demand is running closer to 3%, but apart from weak structure (both residential and nonresidential) investment, the economy looks to be firing on all cylinders with PCE estimated to grow 3.4% Q/Q SAAR.

- As noted earlier, MNI expects the BEA to be able to provide a Q3 advance GDP estimate by early December.