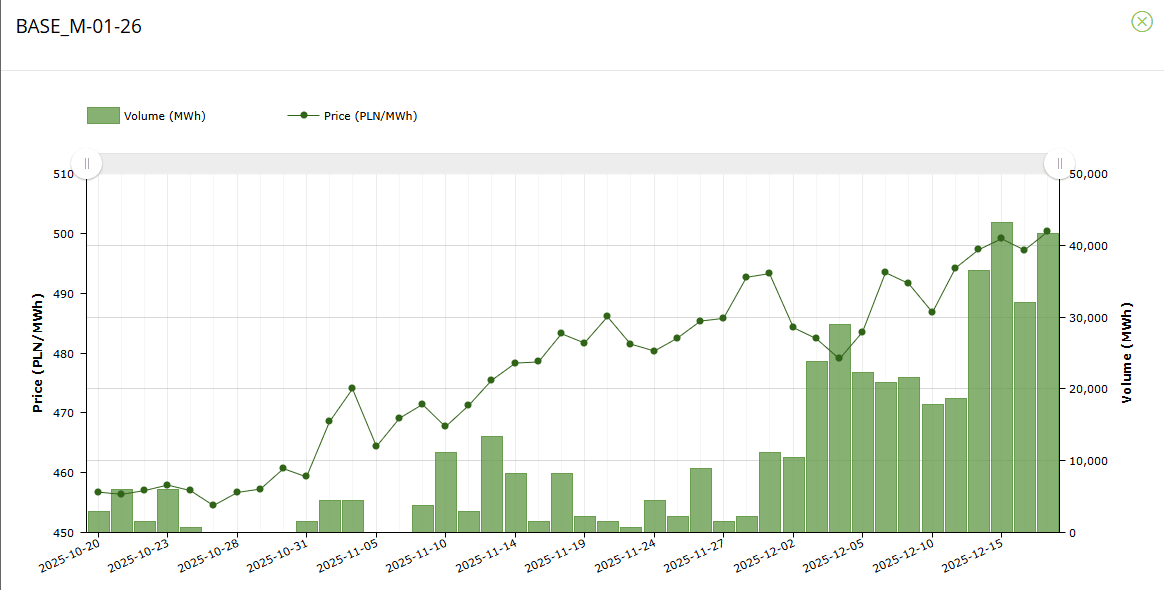

POWER: Poland's Front Month Breaks PLN500/MWh For First Time

Poland’s January rebounded to break the PLN500/MWh level for the first time since becoming liquid amid sharp price increases in EU coal and a downward revision of temperatures for most of next month.

- Poland’s January baseload power settled at PLN500.23/MWh compared to its settled price of PLN497.20/MWh on 16 December, according to data on Polish power exchange TGE.

- EUA DEC 26 down 0.3% at 87.13 EUR/MT

- TTF Gas JAN 26 up 2.1% at 27.315 EUR/MWh

- The EUA Dec26-UKA Dec26 spread is narrowing on Wednesday to the lowest since the 10 December close with stronger gains in the UK market, after the British government confirmed it had set a timeline to finalise talks on relinking the two ETS systems.

- The 630MW Plock power plant will still be disconnected over 9-24 January, while the 1.34GW Jaworzno 3 power plant will be curtailed by up to 775MW from 6-17 January amid works at three 225MW units.

- However, works at other key power plants will be limited over the month, still keeping supply firm.

- Average temperatures in Warsaw were mostly revised lower over 1-30 January and is expected to be below the seasonal for most days over the period, only returning above over 14-18 January.

- Closer in, average temperatures in Warsaw were mostly revised lower over 18-22 December. Temperatures are expected to be above the seasonal norm until flipping below from 25 December – reaching as low as -5.3C on 27 December.

- The 910MW Jaworzno 2 power plant unplanned 230MW curtailment will still last until 20 December, while the 1.83GW Turow power plant will fully return to grid on 23 December.

- The day-ahead decline to PLN514.57/MWh for Thursday delivery from PLN530.06/MWh for Wednesday amid wind expected at 22% load factor tomorrow compared to 18% today.

- Looking ahead, wind is anticipated to be at a 3.5GW, or a 38% load factor on 19 December (Friday) – which could weigh on costs.

- Separately, Polish utility ZE PAK has secured a PLN2.16bn (€500mn) loan to fund its 562MW gas-fired power plant.

And Polish TSO PSE has unveiled its Strategy to 2040, aiming to ensure a zero-emission power system, with renewables projected to supply 60% of Poland’s electricity by 2035.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY OPTIONS: Dec'25/Mar'26 10Y Call Spread

- 10,300 TYZ5 113/TYF6 113.5 call spds, 18 net/Jan over vs. 112-25/0.03%

OAT: Modest Widening Vs. Bunds, Sell-Side Remain Cautious

OAT/Bunds 0.5bp wider at 74bp after registering a multi-month low of ~71.5bp on Thursday.

- Softer European equities and risks to PM Lecornu’s deficit target (4.7%) present widening impulses as National Assembly discussions on the revenue side of the Budget resume this week.

- Passage of the Budget presents the clearest risk to the 70bp mark in the coming weeks, although ongoing structural fiscal issues and political risks continue to limit the scope for spread tightening and promote a degree of caution within the sell-side (only modest scope for spread tightening noted across sell-side notes we have read).

- Goldman Sachs: The market will put more weight on near-term political stability than on the more medium-term cost of the pension freeze, which, given the risks already embedded in OATs, is the right judgement in our view. That said, while recent news is constructive, we note that the budget process is still uncertain, with votes on other parts of the bill to come and the 2026 deficit bottom line still unclear. We thus expect some volatility in the spread in coming weeks but maintain our 70bp forecast for 10-Year OAT/Bund by year-end.

- J.P.Morgan: Despite our base case of the 2026 budget getting eventually approved with no government crisis, we find no political risk premia priced in current level of French spreads as quite optimistic. At the same time, we do not find outright underweights in France attractive as under our base case of French budget approval we do expect 10-Year France-Germany to settle around 70bp, close to current levels. We have been partly hedging our overweight carry exposure with underweights in France to partly express our cautious stance on France and partly to hedge carry exposure against risk-offs coming from global factors.

- Societe Generale: Our view on France remains broadly unchanged from September. The challenge lies in timing, given political unpredictability. We expect stable to wider spreads next year, depending on how political stress evolve. Attention will shift to the 2027 presidential elections from 2H26

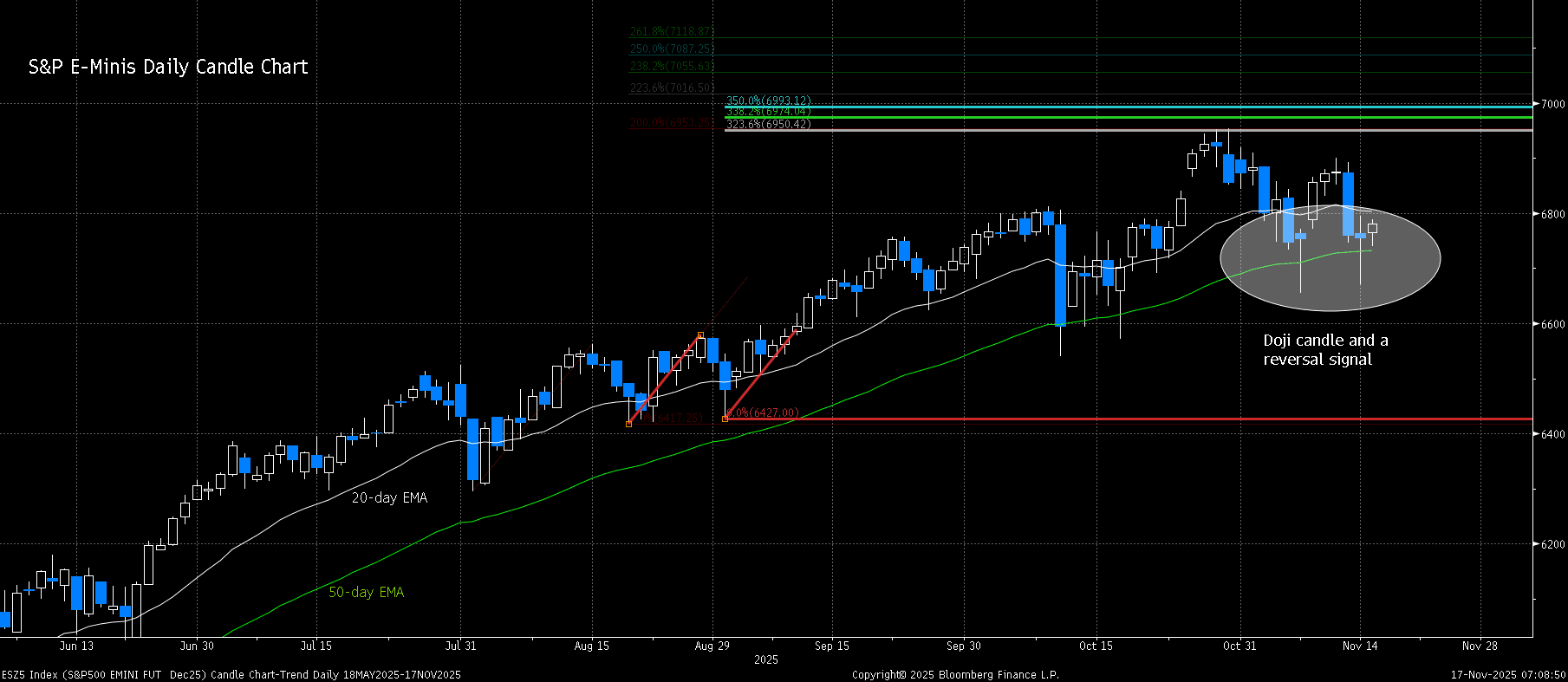

EQUITY TECHS: E-MINI S&P: (Z5) Doji Reversal Candle

- RES 4: 6993.12 3.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 3: 6953.75 High Oct 30 and bull trigger

- RES 2: 6900.50 High Nov 12

- RES 1: 6804.35 20-day EMA

- PRICE: 6750.00 @ 14:35 GMT Nov 17

- SUP 1: 6670.50 Low Nov 14

- SUP 2: 6655.50 Low Nov 7 & key short-term support

- SUP 3: 6571.25 Low Oct 17

- SUP 4: 6540.25 Low Oct 10 and a key support

The trend condition in S&P E-Minis remains bullish and the latest selloff appears corrective - for now. Support at the 50-day EMA, at 6730.32, has been pierced, however, price is once again trading above the average. The next key support to watch is 6655.50, the Nov 7 low. Friday’s price pattern is a doji candle - a reversal signal. Initial firm resistance to watch is 6900.50, the Nov 12 high. A breach of this level would be bullish.