POWER: Poland's February Hits Fresh All-Time High

Jan-02 15:29

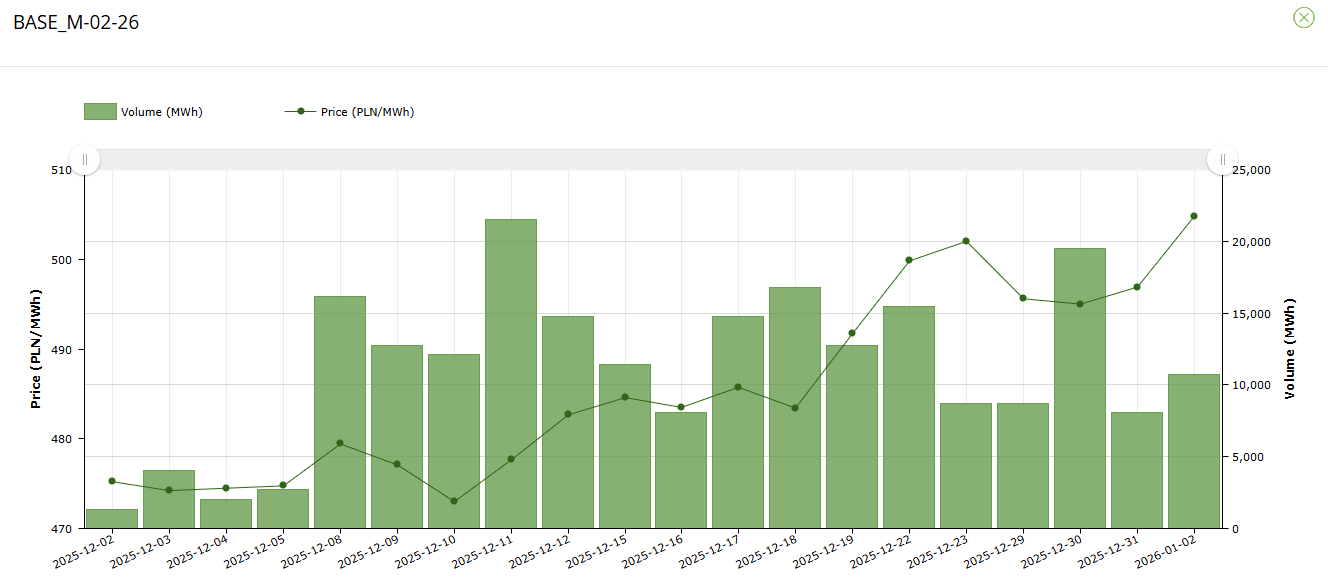

Poland’s February climbed sharply to be supported by gains in EU ETS and European coal, with average temperatures in Warsaw forecast to be mostly below the seasonal norm until the middle of February.

- Poland’s February baseload power settled at PLN504.80/MWh compared to its settled price of PLN496.90/MWh on 31 December, according to data on Polish power exchange TGE.

- EUA DEC 26 up 1.1% at 88.31 EUR/MT

- Rotterdam Coal FEB 26 up 1% at 95.25 USD/MT

- EUAs Dec26 are rising today and are on track for weekly gains of nearly 0.5%, nearing the highest level since Aug 2023, amid bullish sentiment on tightening supply in 2026. The return of market participants from the holiday period is likely to lift buying interest.

- Average temperatures in Warsaw were revised mostly higher over 1-31 January but are expected to be mostly below the seasonal norm until the middle of February.

- Closer in, average temperatures in Warsaw were mostly revised lower over 3-7 January by as much as 3C and will be below the seasonal norm until flipping above over 13-16 January. Temperatures are seen reaching as low as -12.5C on 6 January.

- The day-ahead rose to PLN370.74/MWh for Saturday delivery from PLN248.86/MWh for Friday amid wind expected at 64% load factor tomorrow, down from 77% today.

- Separately, Poland’s PGE has scrapped a PLN 1.3bn (€310mn) contract to modernise the 500MW Porabka-Zar pumped-storage hydropower plant, accusing contractors of delays and faulty execution.

Additionally, Poland’s climate ministry is renewing support for biogas and biomethane production, proposing auctions for facilities above 1MW, while streamlining rules for onshore wind farms, it said.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Market Still Prices Over 90% Odds Of Dec Cut, No Reaction To ISM

Dec-03 15:26

Little net reaction in the USD short end following the mixed ISM services report, which won’t have changed the picture for the Fed (with elevated inflation and questions surrounding the health of the labor market remaining intact).

- To recap, while the headline index and was firmer-than-expected, the prices paid component (while still elevated at 65.4) came in on the softer side of expectations. Meanwhile, the new orders subindex showed a slower rate of expansion and the employment subindex showed a slightly reduced rate of contraction.

- Fed Funds continue to indicate 23.5bp of easing for this month, 32bp through January, 40bp through March, 48bp through April and 62.5bp through June.

- SOFR futures 0.25-3.0 firmer on the day vs. 0.25-3.5 firmer heading into the ISM release.

- Implied terminal rare pricing 3.025% after threatening to break below 3.00% earlier.

US TSYS: Post ISM Services React

Dec-03 15:04

- Treasuries scale back support after ISM services data - prices paid and new orders lower than expected while the Services index and employ component rise slightly.

- Currently, TYH6 trades 113-01.5 (+5) vs. 113-07 high, initial technical resistance at 113-11/22+ High Dec 1 / High Nov 25. Support below at 112-22 Low Dec 02

- Curves mildly steeper: 2s10s +.312 at 57.753, 5s30s +1.424 at 110.291.

MNI: US ISM NOV SERVICES COMPOSITE INDEX 52.6

Dec-03 15:00

- MNI: US ISM NOV SERVICES COMPOSITE INDEX 52.6

- US ISM NOV SERVICES PRICES 65.4