POWER: Poland's 3Q25 Edges Up on Coal, Emissions

Poland’s 3Q25 rebounded slightly from the previous session amid gains in European coal and EU ETS. However, gains were limited amid the return of power plants heading into July and limited planned works over the quarter.

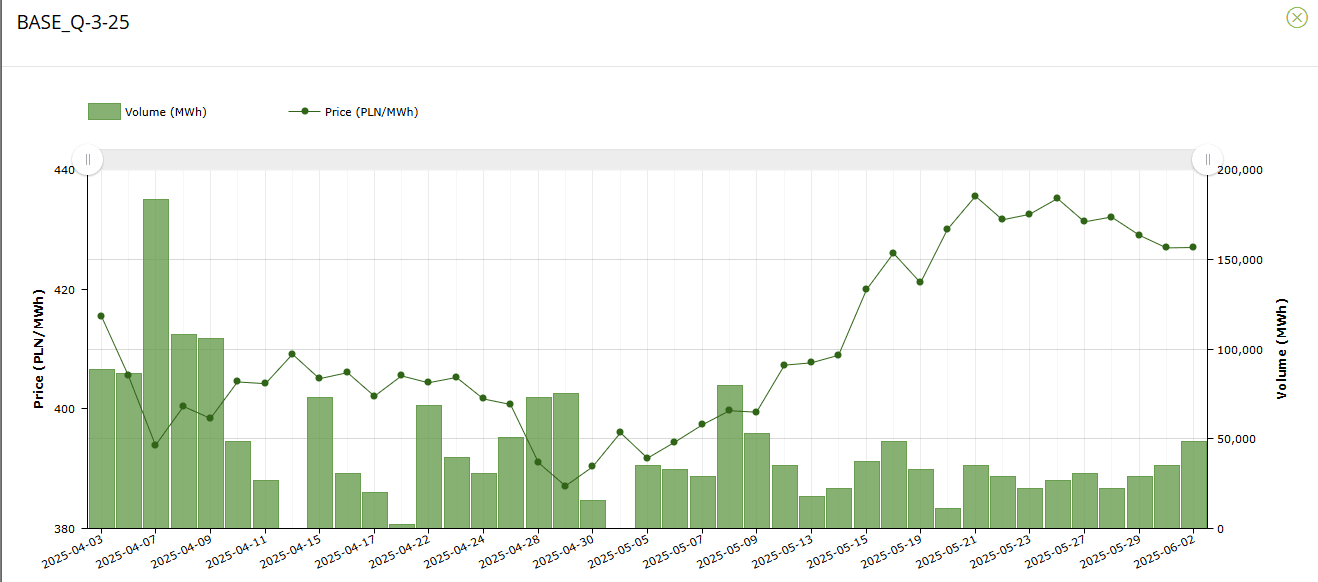

- Poland’s 3Q25 baseload power settled at PLN426.96/MWh compared to its settled price of PLN426.90/MWh on 30 May, according to data on Polish power exchange TGE.

- EUA DEC 25 up 1.6% at 71.54 EUR/MT

- Rotterdam Coal JUL 25 up 2.3% at 97 USD/MT

- The contract rebounded to end its two-session downward trend, however, it is still lower on the week to be below its settlement last Monday (26 May) at PLN435.15/MWh.

- Liquidity for the contract increased to its highest since 16 May, with 22 lots done in 19 transactions from 16 lots in the previous sessions.

- The 465MW EC Wloclawek B1 power plant is anticipated to return to the grid on 20 June from works that began on 13 February.

- Additionally, the 450MW EC Stalowa Wola power plant will return on the same day. Planned works at the plant started on 5 May.

- Mean temperatures in Warsaw have been mostly revised over July-September by as much as 1.2C in July and are seen averaging between 15.1-19.8C over 3Q25.

- Closer in, Mean temperatures in Warsaw have been mostly revised higher over 3-7 June and will be mostly above the seasonal norm until 15 June- climbing to as high as 22.2C on that day.

- The day-ahead dropped slightly PLN488.40/MWh for Tuesday delivery from PLN511.72/MWh for Monday amid the almost full return of the 680MW Gryfino unit 9 unit.

- However, wind is only expected at a 3% load factor tomorrow from 19% today – which likely kept losses limited.

- Looking ahead, wind is expected to be at 19% load factor, or 1.79GW on 4 June (Wed) – likely to place some downward pressure on delivery costs.

Separately, Poland's new president, Karol Nawrocki, has openly rejected the wind energy bill—an amendment that would allow wind turbines to be built 500m from residential buildings—and declared the EU Green Deal "unconstitutional."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Hits Bear Trigger, New Cycle Low

- RES 4: 1.4415 High Apr 1

- RES 3: 1.4296 High Apr 7

- RES 2: 1.4087 50-day EMA

- RES 1: 1.3906/3935 High Apr 17 / 20-day EMA

- PRICE: 1.3793 @ 17:00 BST May 2

- SUP 1: 1.3760 Low Apr 21 and the bear trigger

- SUP 2: 1.3744 76.4% retracement of Sep 25 ‘24 - Feb 3 bull run

- SUP 3: 1.3696 Low Oct 10 2024

- SUP 4: 1.3643 Low Oct 9 ‘24

The trend set-up in USDCAD deteriorated further Friday, with prices slipping through the bear trigger to narrow the gap with next support. The fresh cycle low reinforces the bear cycle and signals scope for a continuation near-term. Potential is seen for a move towards 1.3744, a Fibonacci retracement. Moving average studies are in a bear mode position, highlighting a dominant downtrend. First resistance to watch is 1.3943, the 20-day EMA.

AUDUSD TECHS: Consolidation Phase

- RES 4: 0.6550 61.8% retracement of the Sep 30 ‘24 - Apr 9 bear leg

- RES 3: 0.6528 High Nov 29 ‘24

- RES 2: 0.6471 High Dec 9 ‘24

- RES 1: 0.6470 High May 2

- PRICE: 0.6445 @ 16:59 BST May 2

- SUP 1: 0.6344/6316 Low Apr 24 / 50-day EMA

- SUP 2: 0.6181 Low Apr 11

- SUP 3: 0.6116 Low Apr 10

- SUP 4: 0.5915 Low Apr 9 and key support

AUDUSD remains inside a consolidation phase, having traded either side of the 0.6400 level for 10 consecutive sessions. The underlying trend remains bullish and the pair is trading close to recent highs. Price has recently breached a key resistance at 0.6409, the Dec 9 ‘24 high. This breach reinforces bullish conditions and signals scope for a continuation higher near-term. Sights are on 0.6471 next, the Dec 9 2024 high. Initial key support to monitor is 0.6316, the 50-day EMA. A clear break of this EMA would be a concern for bulls.

US TSYS: Rates Retreat, Sentiment Improved Though Trade Risk Remains

- Treasuries look to finish near late Friday session lows after trading firmer on the open, higher than expected Nonfarm payrolls at 177k (sa, cons 138k) of which private contributed 167k (sa, cons 125k) triggered the early reversal.

- However, two-month revisions of -58k offset the 39k beat for nonfarm payrolls, with a similar story for private (a 42k surprise vs -48k two-month revision).

- Stocks are back near four week highs - pre-"Liberation Day" levels as hopes of some trade deal being made improved sentiment.

- The Wall Street Journal reports that "Beijing is considering ways to address the Trump administration’s gripes over China’s role in the fentanyl trade... potentially offering an off-ramp from hostilities to allow for trade talks to start." The Journal notes that "discussions remain fluid" and China "would like to see some softening of stance from President Trump".

- Currently, the Jun'25 10Y contract trades -20 at 111-07.5 vs 111-02 low -- initial technical support (50-dma) followed by 110-16.5/109-08 (Low Apr 22 / 11 and the bear trigger). Curves bear flattened, 2s10s -3.480 at 48.002, 5s30s -4.911 at 86.807.