POWER: Poland October Power Rises Again

Sep-17 13:58

Poland’s October power base-load contract rose again with gains in the energy complex.

- The Polish October power base-load OTC contract rose to PLN431.9/MWh in Wednesday’s session, from PLN425.25/MWh the previous day, according to data on Polish power exchange TGE.

- Liquidity for the contract declined to 15 lots in 15 transactions, down from 23 lots in 21 transactions on Tuesday.

- TTF front month is extending gains from yesterday amid concern for future Russian supplies, set against an expected ramp up in Norwegian supplies later this week. EC President von der Leyen said that the EU is looking into fast tracking the end of energy imports from Russia after the US said it needs to stop.

- EUAs Dec25 are edging higher, hitting a fresh high since mid-February on sustained confidence and support from EU gas gains.

- The latest ECMWF two-week weather forecast for Warsaw suggests mean temperatures will remain well above normal until mid-next week after which temperatures will drop below normal.

- Wind output in Poland is forecast at 571MW to 3.46GW during base-load hours over 18-26 September according to SpotRenewables.

- Planned maintenance at the 430MW Lagisza B10 coal plant is scheduled to end on 18 September.

- The 474MW Patnow B9 power plant is scheduled to be offline in an unplanned outage until 21 September.

- The 630MW Plock power plant will also be fully disconnected over 19-27 September.

- In the day-ahead market, the Polish sport power index increased sharply to PLN548.06/MWh for Thursday’s delivery, from PLN396.94/MWh in the previous session.

- Wind output in Poland is forecast at 3.46GW during base load on Thursday, down from 4.25GW on Wednesday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURIBOR OPTIONS: ERZ5 98.50 Calls Lifted Again

Aug-18 13:56

ERZ5 98.50 calls paper paid 0.75 on another 10K.

US TSY OPTIONS: Sep'25 5Y Ratio Put Fly

Aug-18 13:50

- 4,000 FVU5 107.75/108/108.5 2x3x1 put flys, ref 108-22.5

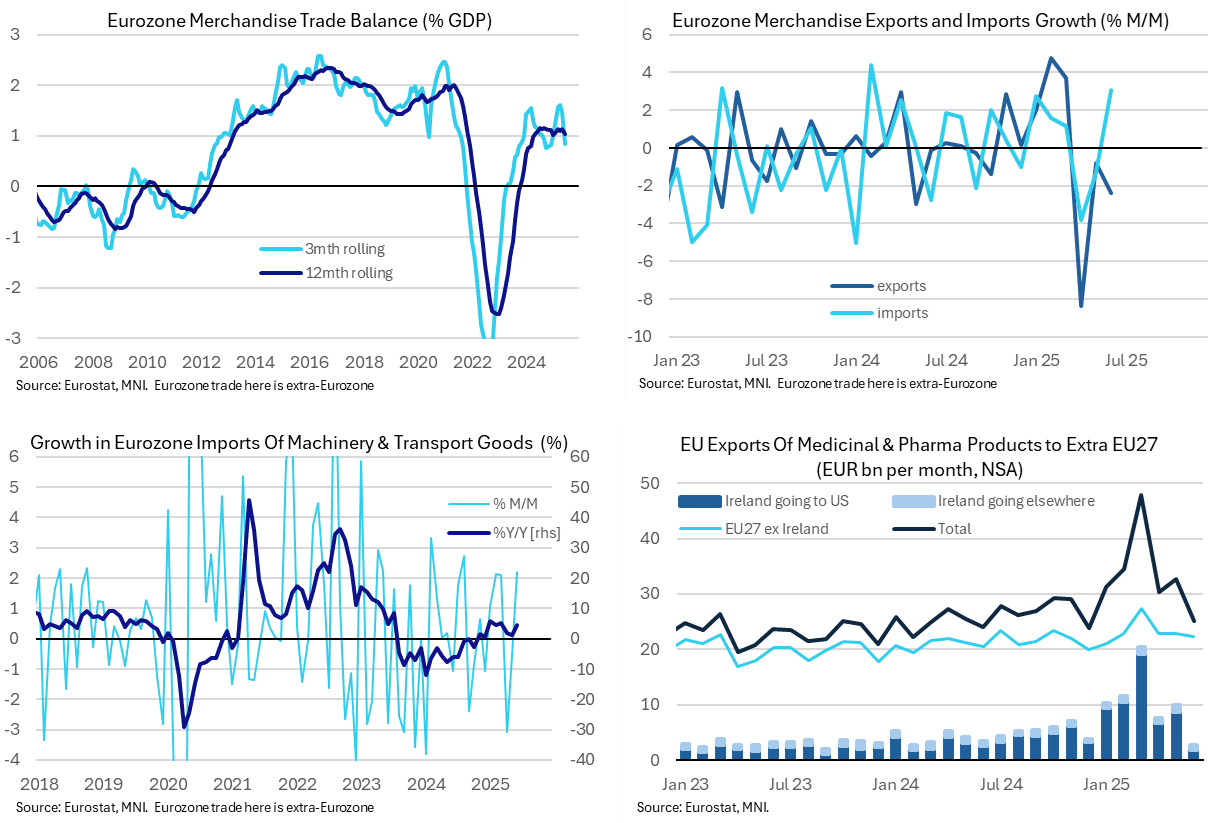

EUROZONE DATA: Trade Surplus Slips Further As Irish Pharma Surge Dries Up

Aug-18 13:45

- The Euro area goods trade surplus was smaller than expected in June at E7.0bln (cons E14.5bln).

- It saw the seasonally adjusted equivalent fall to just E2.8bln after E15.6bln in May for the lowest monthly surplus since May 2023.

- It’s an abrupt further narrowing in surpluses from the E15.0bln averaged in Apr-May and E20.5bln in Q1 (including E27.7bln in March) compared to a more typical E11.6bln in Q4.

- Alternatively, it left a goods trade surplus at ~0.8% GDP in Q2 after 1.6% GDP in Q1 and 0.8% GDP in Q4, with that 2Q25 estimate biased higher by figures earlier in the quarter.

- The narrowing came from a combination of a third consecutive monthly decline for exports (-2.4% M/M) whilst imports firmed (3.1% M/M).

- Export weakness was driven by manufactured goods shipments fell by -4.2% on a -13.2% decline in chemicals & related products likely owing to Irish pharmaceutical exports to the US.

- The more detailed NSA data show that Irish pharmaceutical exports to the US registered an unusually small E1.8bln in June (smallest since Sep 2023) after E8.7bn in May. It’s continued payback from a surge in Q1 when exports summed to E39bln vs the E44bln through 2024 as a whole. As such, it may not necessarily be surprising but it’s still notable and could see similarly small readings ahead.

- Back to the swda data, imports strength looks particularly concentrated meanwhile, with the commodities & other unclassified category surging 148% (from E2.8bln to E7.1bln) and a 7% rise in chemicals & related products (from E30.2bln to E32.3bn).

- As for somewhat more forward-looking indicators of domestic demand, imports of machinery & transport equipment increased a modest 2.2% M/M considering it followed a cumulative -3.6% decline in April and May. It left them up 4.6% Y/Y on this calendar adjusted basis for one of the faster readings in recent years but still relatively tepid for a nominal measure.