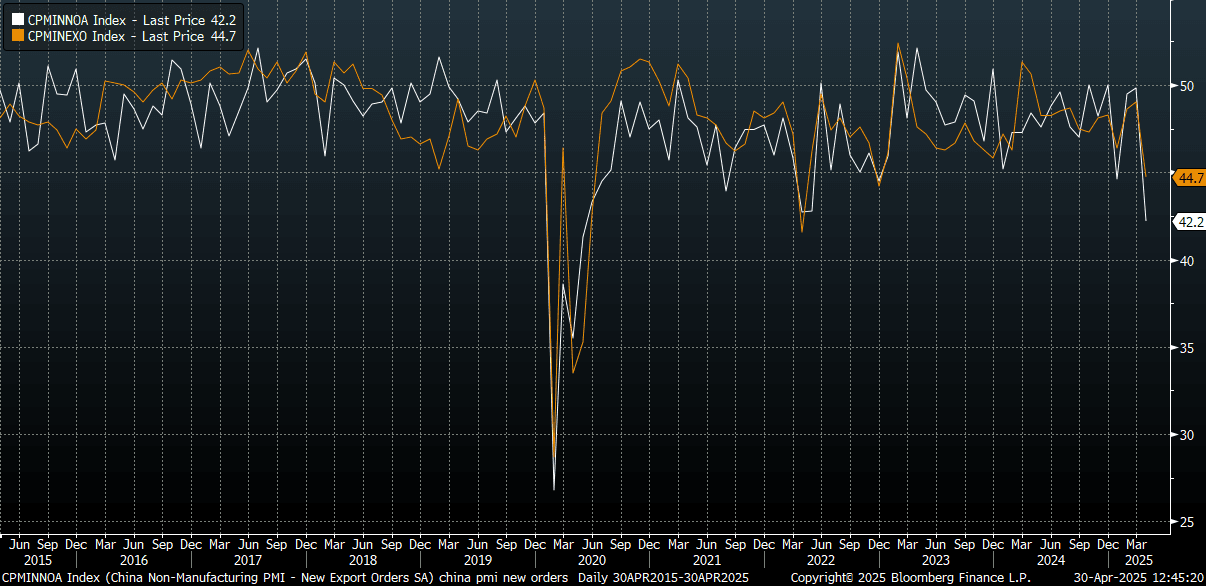

CHINA DATA: PMI Details: New Export Orders Slump, Price Indices Lower

The detail of the official PMI print showed new orders were down to 49.2, back to lows from Jan of this year. New export orders slumped to 44.7, which is fresh lows back to end 2022. April 2022 lows for this index were sub 42.0, while we got to below 30 during the Covid pandemic in 2020. The tariff impact is clearly in play here, with anecdotes of sharp declines in China to US shipping highlighted in recent weeks. For the services PMI, new export orders also fell sharply to 42.2, which is fresh lows back to 2020, see the chart below (which is the white line on the chart, manufacturing is the orange line).

- The aggregate new orders to inventory ratio eased to 1.04 for the manufacturing index, so softer but not implying a collapse in the headline PMI going forward.

- Inputs prices for the manufacturing PMI eased to 47.0 from 49.8 prior. Output prices fell to 44.8 from 47.9 prior.

- For the services side, input prices and selling prices also eased further and remain comfortably sub the 50.0 level.

- Overall, this still points to the need for further policy support, with external risks growing at a time when price pressures remain benign.

Fig 1: China PMIs - New Export Orders Slump

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JPY: USD/JPY Tracking US Yields Lower** (correction)

** corrected CFTC update in the final paragraph.

After moving lower on Friday night to close around 4.25% 10 Yr US yields have moved again gapping lower this morning as risk starts the week squarely on the backfoot. We were last near 4.21% (down around 4bps). USD/JPY has followed suit, after touching 149.84 early doors it has quickly come back under selling pressure printing under 149.00 in latest dealings.

- The market might have been hoping for some USD demand into the Japanese fix to sell at better levels but once yields started collapsing the sellers were forced to engage. Technically the pair has failed once more around 151.00 and the bears once more have gained the upper hand.

- On the day any bounces back towards 149.80/150.20 should see sellers reemerge, early morning Monday price gaps in Asia have an ugly habit of being unwound as the day evolves but if risk remains under pressure so too shall USD/JPY.

- While USD/JPY continues to be capped around 151.00/50 it will remain a sell on rallies, a break below the 146.50 area would see the move lower gain momentum. We were last near 148.80/85, with broader risk trends dominating sentiment.

- Also note, Japan’s Government Pension Investment Fund will announce its asset allocation for the next five years later today which could have important implications for the market (see this BBG link).

- CFTC weekly data shows leverage funds slightly reduced shorts and Asset managers continue to rebuild JPY longs.

Fig 1: USD/JPY CFTC Positioning Data

Source: MNI - Market News/Bloomberg

JPY: USD/JPY Tracking US Yields Lower

After moving lower on Friday night to close around 4.25% 10 Yr US yields have moved again gapping lower this morning as risk starts the week squarely on the backfoot. We were last near 4.21% (down around 4bps). USD/JPY has followed suit, after touching 149.84 early doors it has quickly come back under selling pressure printing under 149.00 in latest dealings.

- The market might have been hoping for some USD demand into the Japanese fix to sell at better levels but once yields started collapsing the sellers were forced to engage. Technically the pair has failed once more around 151.00 and the bears once more have gained the upper hand.

- On the day any bounces back towards 149.80/150.20 should see sellers reemerge, early morning Monday price gaps in Asia have an ugly habit of being unwound as the day evolves but if risk remains under pressure so too shall USD/JPY.

- While USD/JPY continues to be capped around 151.00/50 it will remain a sell on rallies, a break below the 146.50 area would see the move lower gain momentum. We were last near 148.80/85, with broader risk trends dominating sentiment.

- Also note, Japan’s Government Pension Investment Fund will announce its asset allocation for the next five years later today which could have important implications for the market (see this BBG link).

- CFTC weekly data shows leverage funds are starting to turn long JPY and Asset managers continue to add to their longs that had been pared back at the beginning of the year.

Fig 1: USD/JPY CFTC Positioning Data

AUD: Recent Ranges Still Holding, Positioning Biased For Lower A$ Levels

AUD/USD saw a brief dip to 0.6269 amid earlier risk off, but we are back near 0.6285/90 in latest dealings. Friday ranges (0.6312 - 0.6281) were tight considering the moves in Equities and US rates. A higher than expected print in the PCE data on Friday saw some significant moves lower in both equities and US yields. These moves have extended today, amid tariff/US growth fears, but spill over to the AUD remains fairly limited. The A$ is lagging yen gains though.

- More broadly, AUD/USD price action remains pretty directionless in the short term with the currency caught between wanting to go lower on negative risk sentiment and lower stocks, but with US yields also moving lower this has seen the USD also come under pressure.

- While stocks remain under pressure the bias may be for the AUD to continue to trade heavy, with scope for sellers to emerge towards 0.6300/10 on the day and a break of the support around 0.6250 could see momentum begin to pick up.

- Ultimately AUD/USD still seems stuck in a wider 0.6200 - 0.6400 range for now.

- This week we have the RBA but with the market not expecting any moves until we get more information from the quarterly CPI, attention will turn again this week to US data.

- Trumps tariffs will be front and centre but with lots of negative sentiment already in the price there is a high bar to exceed expectations. Hence the ISM prints this week particularly Services and then NFP will offer the most potential for movement.

- CFTC weekly data shows leveraged funds and Asset managers both continued to add to their respective AUD shorts, see the chart below.

Fig 1: AUD CFTC Positioning

Source: MNI - Market News/Bloomberg