ISRAEL: PM Office-Israel Will Respond Accordingly After IDF Off. Injured By IED

Following an injury to an IDF officer caused by an IED in the southern Gaza city of Rafah, a statement from the office of Prime Minister Benjamin Netanyahu claims "Hamas continues to violate the ceasefire and Trump's 20-point plan. Their violent intentions and violations were once again confirmed by the explosion of an IED that injured an IDF officer. Hamas must be held to the agreement they signed, which includes removal from power, demobilization, and deradicalization. Israel will respond accordingly."

- Earlier in the day, Turkish Foreign Minister Hakan Fidan met with Hamas political bureau officials in Ankara. Reuters reports "the Hamas officials told Fidan that they had fulfilled their requirements as part of the ceasefire deal, but that Israel's continued targeting of Gaza aimed to prevent the agreement from moving to the next phase."

- Both sides have accused the other of ceasefire violations, something that will be discussed on 29 December when Netanyahu meets with US President Donald Trump at his Mar-a-Lago club in Florida. There have been reports of increasing frustration in the US administration at the slow progress towards the second phase of the ceasefire agreement, which is due to see an international stabilisation force deployed to Gaza. Despite Turkey saying this could come in the early part of 2026, there is not agreement yet on what countries will contribute to this force, or how it will operate.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - Gains In Gilts Appear Corrective

- In the FI space, a rally in Bund futures on Friday appears to be a correction - for now. Price remains below an important resistance around the 50-day EMA, at 129.04. A clear break of the EMA is required to signal a potential reversal. Recent weakness has resulted in a print below support at 128.52, 76.4% of the Sep 25 - Oct 17 bull leg. A resumption of the bear leg would open 128.25, the Oct 7 low.

- A sharp sell-off in Gilt futures last Wednesday strengthens a bear threat and cancels a recent bullish condition. The contract has traded through 91.82, the Sep 11 high, and the move down signals scope for a deeper retracement that opens 91.12, 61.8% of the Sep 3 - Nov 4 bull leg. On the upside, initial key resistance is seen at 92.70, the 20-day EMA. A clear break of the average is required to signal a reversal. For now, gains are considered corrective.

EQUITY OPTIONS: Latest Estoxx Option

- SX5E (20th Mar) 6000/6300cs 1x2, bought for 24 in 5k (5kx10k).

- SX5E (16th jan) 5000p, (20th feb) 5000p, (20th mar) 5000p, trades as a Put Fly for -7 in 3k.

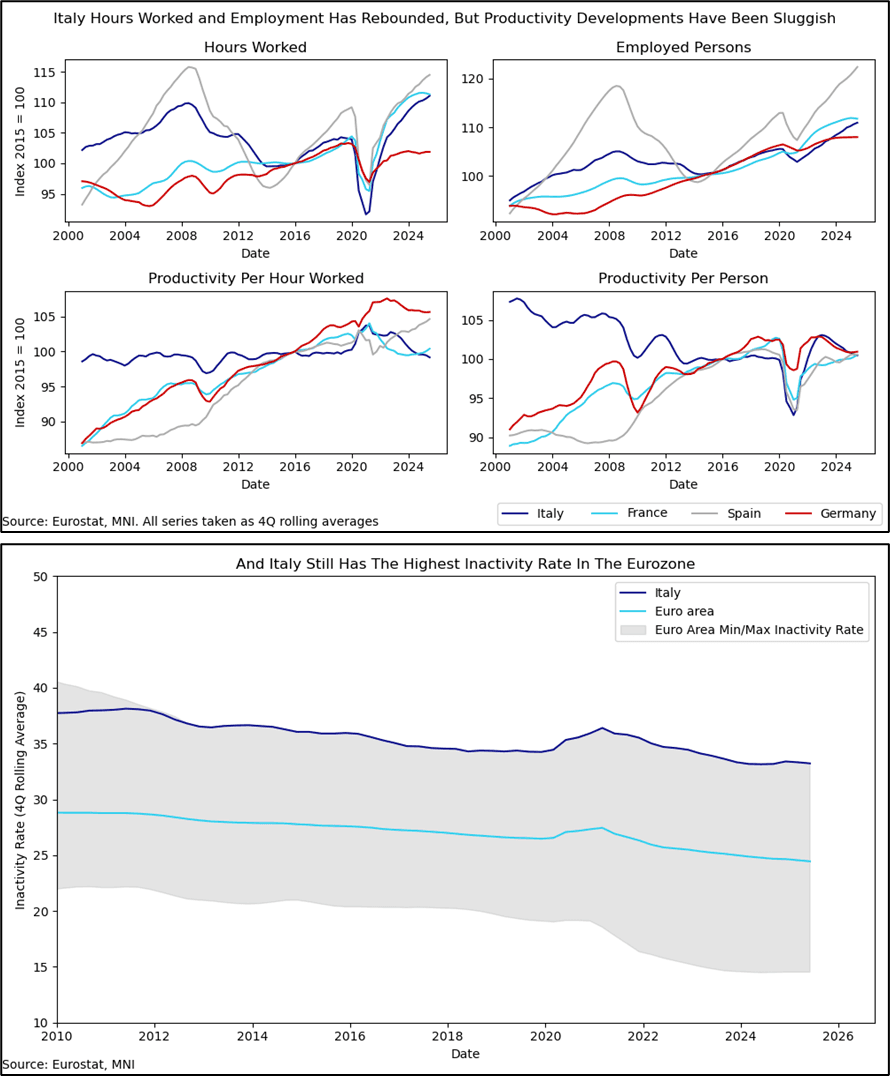

ITALY: Moody's Upgrade Expected, Growth Outlook Key For Further Positive Action

Moody’s upgraded Italy’s credit rating to Baa2 (Outlook Stable) on Friday, in line with our expectations. Further positive ratings action is possible next year, contingent on “continued fiscal consolidation resulting from further improvements in the quality of revenue and spending” and “faster progress in addressing structural challenges related to the labour market and innovation capacity, together with stronger private investment than we currently assume”

- We’ve previously argued that growth dynamics, rather than primary balance consolidation, presents the main risk to the Italian fiscal/ratings outlook. Worse-than-expected growth outturns may limit narrowing momentum in BTP/XXX spreads in the coming years.

- Analysts expect a cyclical rebound in Italian growth, from 0.5% Y/Y in 2025 to 0.7% in 2026 and 0.9% in 2027. These are broadly in line with the EC’s latest projections (0.8% in both 2026 and 2027).

- Private consumption is expected to be supported by low unemployment rates and positive real wage growth. Meanwhile, non-residential investment growth should continue to be aided by EU RRP disbursements.

- The key cyclical questions ahead will be if middle-class tax cuts announced in the 2026 budget spur additional consumption, and whether private investment can fill the gap left by RRP funds once that programme ends.

- Meanwhile, the outlook for potential output remains bleak. Although employment and hours worked have rebounded solidly post covid, sluggish growth metrics have implied poor productivity outturns. Meanwhile, Italy still has the highest inactivity rate across the Eurozone. Coupled with an ageing population, this presents a key structural headwind that government policy will need to address.