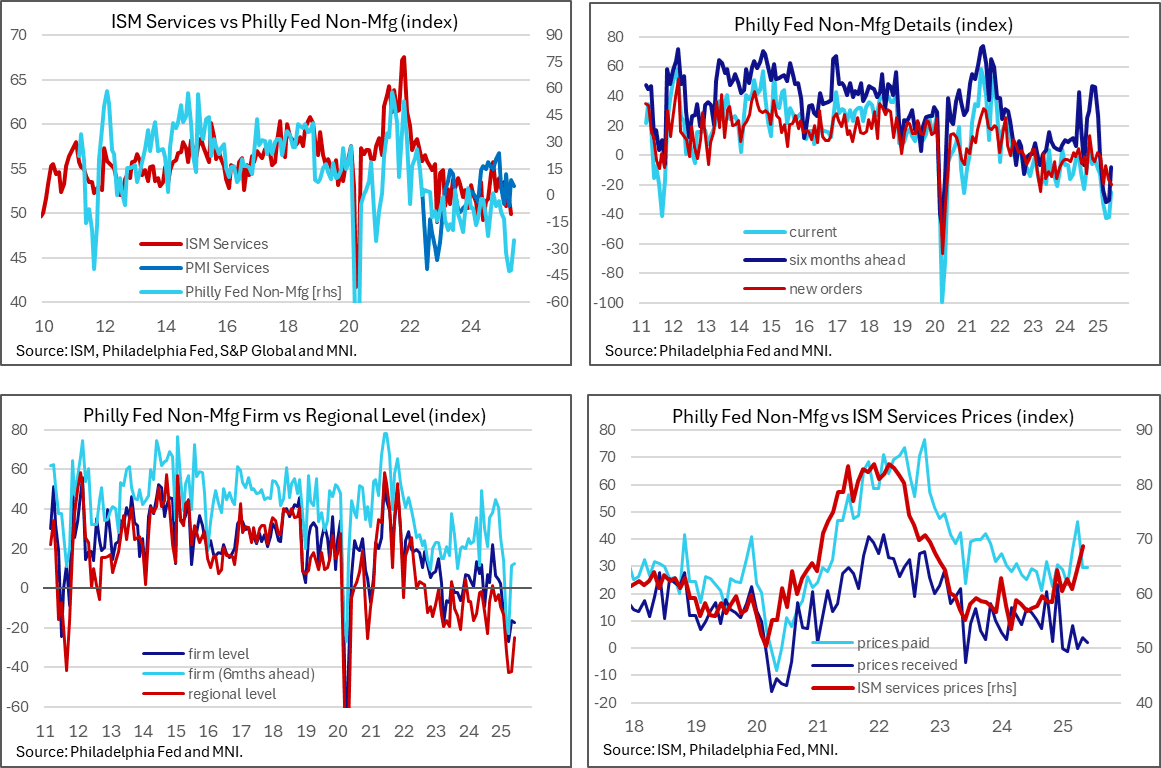

US DATA: Philly Fed Non-Mfg Improves As Regional Weakness Dialled Back

The Philly Fed non-manufacturing survey saw firms dial back particularly negative views on the regional economy to one closer to their own experiences. Some details were weak however, such as new recent lows for new orders along with the prices received index almost in balance.

- The Philly Fed non-manufacturing index improved to -25.0 in June after two particularly weak readings of -41.9 in May and -42.7 in April (both the weakest since the series started in 2011 aside from two months at the depths of the pandemic).

- For context though, this is the highest since February and compares poorly with an average -8.0 in 2024, -10.4 in 2023 and +3.7 in 2022.

- Recent swings in sentiment have been more pronounced for this measure of regional perceptions, whilst the firm-own activity index has been steadier. This own look at activity was little changed at -17.3 after -16.3 in May having recovered from lows of -26.7 in April after tariff announcements (also the lowest in the series aside from Apr/May 2020).

- The details behind these headline figures were mixed, but new orders weakness was notable, falling from -16.3 to -20.1 for its lowest since Apr 2023 and before that the pandemic.

- This new orders weakness contrasts with yesterday’s flash PMIs, which indicated a softening but one that remains in positive territory: “The ongoing expansion reflected a further rise in new orders, which have now risen continually for 14 months, though the rise in orders dipped slightly in June to remain well below the strong gains seen at the turn of the year. Similar gains in inflows of new work were recorded in the manufacturing and service sectors and, in both cases, growth was driven by rising domestic demand.”

- As for price components, prices paid held steady at 29.7 in June after 29.6 in May, off April’s 46.5 for levels close to last year’s 28.3 average. However, there’s still sign of feed through to prices received with the index at 2.2 after 4.0 in May, down from the 11.4 averaged last year.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGB TECHS: (M5) Rallies off Lows

- RES 3: 147.74 - High Jan 15 and bull trigger (cont)

- RES 2: 146.53 - High Aug 6

- RES 1: 141.48/142.95 - High May 2 / High Apr 7

- PRICE: 139.40 @ 15:42 GMT May 23

- SUP 1: 138.54 - Low May 22

- SUP 2: 136.57 - 1.382 proj of the Jan 28 - Feb 20 - Feb 26 bear leg

- SUP 3: 134.89 - 2.000 proj of the Jan 28 - Feb 20 - Feb 26 bear leg

JGBs have rallied off recent lows and for now, however a bearish theme remains intact following the reversal that started Apr 7. A continuation lower would signal scope for an extension towards 136.57, a Fibonacci projection. On the upside, a reversal higher would instead refocus attention on 142.95, the Apr 7 high. The first important resistance to watch is 141.48, the May 2 high. A break of this level would be viewed as an early bullish signal.

US FISCAL: Total Tariff Income Jumping In May As New Rates Hit

Treasury reported a record $16.5B in customs/excise taxes on May 22, reflecting the large increase in tariff rates that went into effect in April.

- Today's report is important because it represents the largest tariff collections of the month which are typically on a due date around the 22nd, when most corporate importers make their payments.

- Thursday's one-day collection is a record, and the month has already set a new record. Tariff revenues have totaled $22.3B so far in May, and are came in at $17.4B in April (after averaging $8.1B/month in 2024).

- For the fiscal year as a whole so far, customs duties have totaled just under $93B, per the Treasury Daily Statement.

US FISCAL: Extraordinary Measures Continue To Dissipate Alongside Treasury Cash

Treasury's latest estimate of the size of "extraordinary measures" available to use "in order to prevent the United States from defaulting on its obligations as Congress deliberate[s] on increasing the debt limit" is down to $67B on May 21 (of an available $299B), vs $82B a week earlier.

- The amount hit the 2nd lowest level since the debt limit impasse started, at $46B, on May 20 (the low was $34B on Feb 24).

- With $476B in cash in the Treasury General Account on May 21, that left the total resources available to Treasury at $543B, the least since April 14 - the day before the annual April 15 tax deadline.

- Treasury Sec Bessent warned Congress earlier this month that "there is a reasonable probability that the federal government's cash and extraordinary measures will be exhausted in August while Congress is scheduled to be in recess. Therefore, I respectfully urge Congress to increase or suspend the debt limit by mid-July".