BRAZIL: Persistent Core CPI Inflation A Concern

Sep-10 17:59

- Although headline IPCA inflation moderated further in August, the details revealed an acceleration in services inflation, with the 3mma sa rate rising by 50bp to 6.7%. Underlying industrial inflation also surprised to the upside, and the average of the core inflation measures rose by 30bp to 4.5% on a 3mma (sa) annualised basis.

- Given the persistence of core inflation, the BCB is widely expected to maintain its high for longer messaging when it decides on interest rates next week (Sep 17), keeping the Selic rate at 15.00%. Indeed, despite the recent moderation in economic activity, credit growth and inflation expectations, JP Morgan says that these are not yet good enough to warrant a change in the central bank’s stance.

- Nonetheless, they expect a decline in the BCB’s inflation projections to underscore that the monetary tightening implemented since H2 2024 is yielding the intended results. So long as economic growth remains subdued this trend should be reinforced in Q4 of this year, in their view. They continue to believe that this would enable the Copom to begin easing as early as December (-25bp), followed by consecutive 50bp cuts to 10.75% next year.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Limited Trade To Open Week, With Sonia Upside Faded Pre-Labour Data

Aug-11 17:52

Monday's Europe bond/rate options flow included:

- SFIH6 96.70 calls 3.5K given at 5

US OUTLOOK/OPINION: Analyst Expectations For Sequential Drivers In July CPI

Aug-11 17:41

Core CPI sequential drivers in July are expected to come from used cars increasing modestly after a weak run plus travel-related services with lodging away from home pausing after declining and airfares increasing after broadly pausing.

- Lodging away from home (+ve): Seen broadly unchanged on the month after a heavy -2.9% M/M in June that subtracted -0.05pps from core CPI.

- Used cars (+ve): There’s a reasonable range of estimates for used car prices in July, from -0.5% to +0.7% but they all are stronger than the -0.7 M/M seen in June. The average estimate is 0.24% M/M after four months averaging -0.6% M/M.

- Airfares* (+ve): Seen rising 1.5% M/M after -0.1% in June following a period of prolonged, large declines with an average -3.7% M/M through Feb-May. The range of views of -0.4% to 2.5% is one of the narrower in recent months.

- Apparel (neutral to small +ve): Median of 0.5%/average 0.44% having accelerated to 0.43% M/M in June from a surprisingly soft -0.4% M/M in May.

- Vehicle insurance* (neutral to small +ve): Once again only three estimates this month with a decent range of -0.1% to 0.6% M/M. The average of 0.2% M/M would be a slight acceleration from the 0.1% in June but it’s a category that can swing from month to month with a sizeable 3.5% weight in core CPI.

- Rents (neutral): Owners’ equivalent rent (OER) seen dipping to an average 0.28% (range 0.25-0.30) after 0.30% in June, but with primary rents firming to an average 0.26% (range 0.22-0.34) after 0.23%.

- Non-core: Food (small -ve): Food price inflation is seen easing to 0.25% M/M in July after 0.33% M/M. Food away from home has continued a robust run recently, with 0.40% M/M in June and a 1H25 average of 0.36% (feeding into core PCE but not CPI). Food at home meanwhile has seen two months averaging 0.27%.

- Energy (-ve): Energy prices are seen falling circa -0.6% M/M after a 0.95% increase in May, driven by a more than 2% M/M decline in seasonally adjusted gasoline prices.

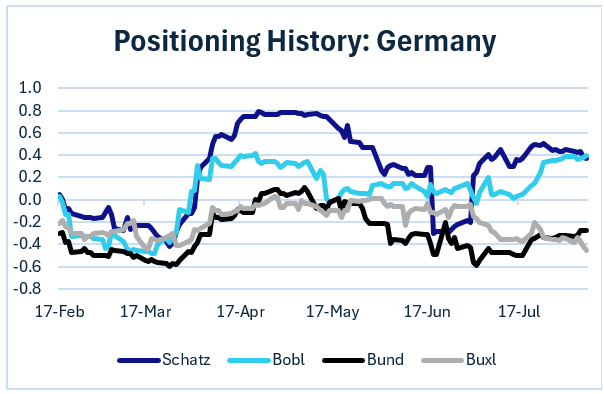

BONDS: Europe Pi: German Positioning Mixed (1/2)

Aug-11 17:37

From our latest Europe Pi futures positioning update (PDF):

- German contracts' structural positioning has been relatively steady since late July, with some subtle shifts. Schatz remains in "long", though has failed to pierce "very long" territory. Bobl has shifted into long territory alongside.

- Bund and Buxl remail short as with the last update.

- Shorts were set across 3 of 4 contracts last week, with the exception being Buxl (longs reduced).