US CREDIT SUPPLY: Pershing Square Hldgs (PSHNA) $Bnchmrk 7Y T+200 A - Fair Value

Oct-23 2025 13:44

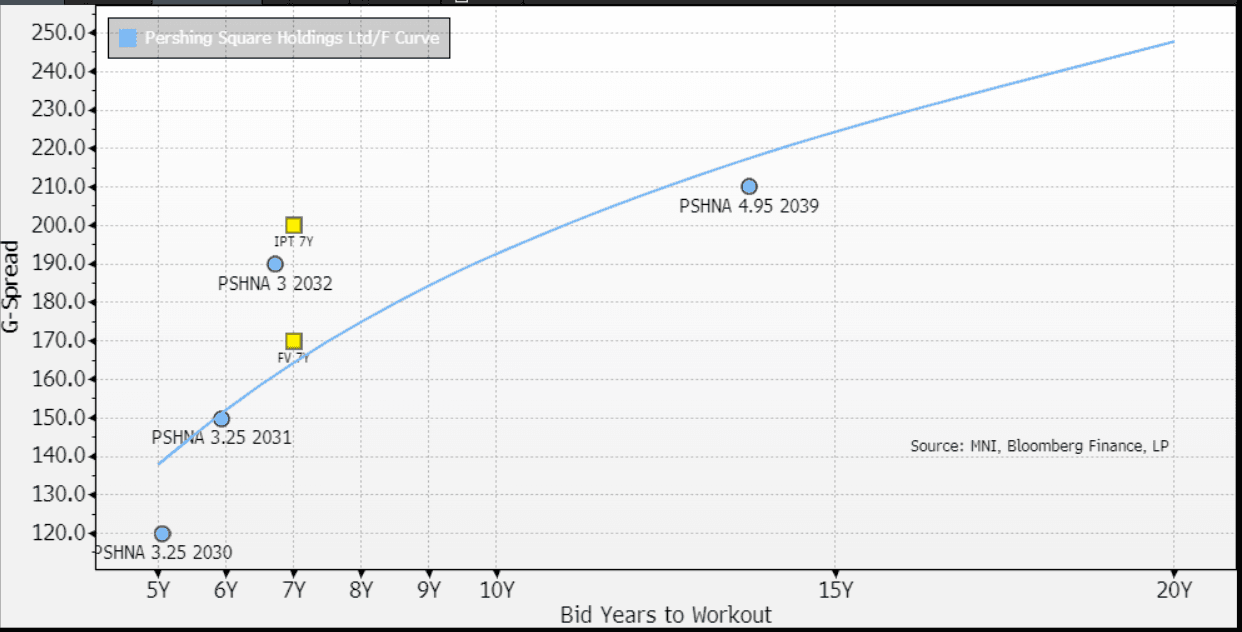

New Issue: Pershing Square Holdings $Benchmark 7Y T+200 Area - Fair Value

(PSHNA;NR/A-/BBB)

• $Benchmark 7Y Fixed (Oct. 28, 2032) +200 Area. FV +170 area

- Using existing levels of 6y and 14yr PSHNA notes (bnchmrk size) we arrive at our FV. PSHNA '32s are a small tranche and illiquid so hard to get good read on levels there. Note all bonds have low $$ price and are not rated by Moody's.

• Issuer: Pershing Square Holdings Ltd/Fund (PSHNA)

• Format: 144A/Reg S without reg rights

• Settlement: Oct. 28, 2025

• Bookrunners: Citi (B&D), BofA, Jefferies, UBS

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: Settled In Ranges Ahead Of Powell & U.S. PMIs

Sep-23 2025 13:41

Activity has been subdued over the past few hours, with little in the way of meaningful macro catalysts noted since the PMI data and soft 30-Year gilt auction during the London morning.

- First resistance holds in gilt futures, as detailed in a recent bullet, while Bund & TY futures have stuck to narrow ranges, despite an uptick in oil and benchmark European equity indices.

- Fedspeak from Governor Bowman & Chicago Fed President Goolsbee has generally leaned a little dovish on net (vs. pre-existing views, see recent bullets for greater detail).

- Activity in Tsy futures remains particularly depleted, even when accounting for the cash market closure in Asia-Pac hours, which was a function of a Japanese holiday.

- Core global FI curves are generally biased flatter on the day.

- U.S. PMI data and comments from Fed Chair Powell highlight the macro calendar during the remainder of the day.

- Note that U.S. President Trump is set to speak at the UNGA, with the White House noting that he will deliver a “major speech touting the renewal of American strength around the world, his historic accomplishments in just eight months, including the ending of seven global wars and conflicts.” See more on that in our political risk team’s daily U.S. briefing: https://media.marketnews.com/MNIPOLRISKUS_Daily230925_080167f664.pdf

AUD: AUDNZD makes an attempt at the 2025 high

Sep-23 2025 13:40

- AUDNZD is on course to test the 2025 high printed last Week at 1.1279.

- Medium Term risk remains to the upside for the AUDNZD following the poor Growth report from New Zealand last Week.

- Some Market participants will look for the next resistance at the 1.1300 figure, but better is seen at 1.1348 next.

US TSY FUTURES: BLOCK: Large 2Y Sale

Sep-23 2025 13:37

- -23,681 TUZ5 104-08.125, sell through 104-08.38 post time bid at 0920:00ET, DV01 $950,000.

- The 2Y contract trades 104-08.12 last (-.25)