SECURITY: Pentagon Suspends Particpation In Think Tank And Research Events

Jul-24 15:53

Politico reports that the Pentagon "has suspended participation in all think tank and research events until further notice... A major shift in engagement from the country’s largest federal agency."

- Politico notes: "The move would sideline the Pentagon from national security dialogues that it has used for decades to advance its policy and explain the department’s rationale. Former Defense Secretaries Jim Mattis, Mark Esper and Lloyd Austin have also used think tank events, such as the International Institute of Strategic Studies’ Shangri-La Dialogue and the Reagan National Defense Forum, to give major policy speeches and hold sideline meetings with both allies and adversaries."

- The move could have implications for relations with China and Russia and geopolitical security more broadly, with senior officials regularly holding sideline meetings on the margins of international conferences like Shangri-La, even during periods of elevated tensions.

- The Pentagon's decision may have been influenced by China's defence minister's decision to skip June's Shangri-La Dialogue for the first time in five years. CNN reported at the time that "China’s downgrading of its Shangri-La delegation showed Beijing was not happy with Washington", per a US defense official.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Larger FX Option Pipeline

Jun-24 15:52

- EUR/USD: Jun26 $1.1600(E4.2bln), $1.1625(E1.1bln), $1.1700(E3.6bln); Jun27 $1.1400(E1.2bln), $1.1415-25(E1.1bln); Jun30 $1.1650(E2.0bln), $1.1700(E1.1bln)

- USD/JPY: Jun26 Y143.00($1.4bln); Jun30 Y143.65-85($1.2bln), Y145.35-50($1.2bln)

- AUD/USD: Jun26 $0.6500(A$2.0bln)

- USD/CAD: Jun26 C$1.3715-35($1.2bln), C$1.3800($1.6bln); Jun27 C$1.3630-45($1.2bln)

US STOCKS: Midday Equities Roundup: IT, Financials & Communications Lead Gainers

Jun-24 15:44

- Stocks are holding moderate gains Tuesday as geopolitical headlines and Fed speakers offered alternating distraction and modest support in late morning trade.

- Currently, the DJIA trades up 419.72 points (0.99%) at 43005.98, S&P E-Minis up 59.5 points (0.98%) at 6136.5, Nasdaq up 268.3 points (1.4%) at 19899.68.

- Information Technology, Financials and Communication Services sectors led gainers in the first half: IT leaders included Intel +5.69%, Advanced Micro Devices +5.56%, Super Micro Computer +4.65% and Enphase Energy +4.54%

- Services stocks led the Financials sector: Coinbase Global +9.38%, Apollo Global Management +3.78% and KKR & Co +3.32%, while media and entertainment shares supported the Communication Services sector: Warner Bros Discovery +2.95%, Charter Communications +2.27%, Netflix +1.96% and Match Group +1.78%

- On the flipside, weaker crude prices (WTI -3.2 at 65.31) weighed on oil and gas stocks: Occidental Petroleum -2.37%, Exxon Mobil -2.06%, Chevron -1.71%, Hess -1.70% and ConocoPhillips -1.20%.

- Broadline retailers and personal products maker underperformed: Dollar General -1.82%, Estee Lauder -1.50%, Dollar Tree -1.49% and Colgate-Palmolive -1.30%.

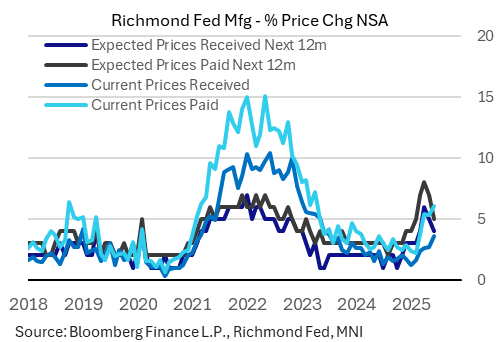

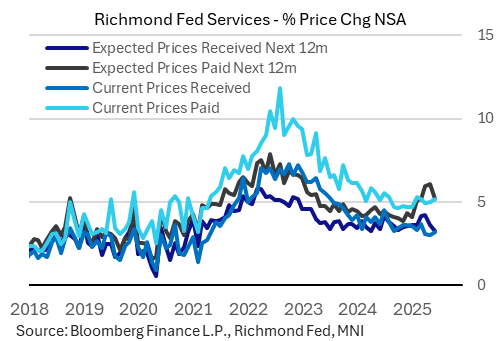

US DATA: Richmond Fed Survey Suggests Tariff Inflation Still Emerging (2/2)

Jun-24 15:36

The Richmond Fed's manufacturing and services surveys showed a divergence in inflation dynamics in June, with current prices reportedly higher but expected future inflation pulling back after recent peaks.

- Manufacturing firms saw current prices received and paid rise, but expected prices continue to pull back, while services firms saw expected future prrices increase even as current inflation pulled back.

- Starting with manufacturing, current prices paid hit a fresh 26-month high 6.1% (based on reported inflation over the last 12 months) , up from 2.2% as recently as February, while prices received rose to a 23-month high 3.6% (up from 1.2% recent low in Jan). But expected prices pulled back for a second consecutive month: paid to 5.0% (4-month low, vs 8.0% peak in April) and received 4.0% (3-month low, ve 6.0% April peak).

- For services firms, current prices ticked up, both received (3.2%, a 3-month high) and paid (5.2%, joint-highest in 4-months). Expected prices however pulled back sharply: paid to 5.2% (3-month low, down from May's recent peak of 6.0%) with received down to 3.2% (14-month low, down from 4.2% recent peak in Mar-Apr).

- We wouldn't read too much into these month-to-month dynamics but they possibly indicate that pipeline price pressures from tariffs are feeding through to regional firms, though the future inflation isn't quite as bad as had been feared immediately after April's Liberation Day announcement.

- In general, services inflation looks better-contained than that for manufactured goods.