US PREVIEW: Payrolls Seen Steadying Out In December After Noisy Oct/Nov (2/2)

Next Friday's release of the December employment report is the highlight of the week's macro calendar. Our usual preview will be out early next week but early consensus expectations are for relatively steady readings vs November, with 55k nonfarm payroll gains (64k in Nov) and an unemployment rate of 4.5% (4.6% in Nov), with a slight moderation in participation and an uptick in hourly earnings growth.

- This is the last payrolls report before the FOMC's end-January meeting, at which participants would probably require substantially weaker-than-expected NFPs to spur even consideration of a another 25bp cut.

- That said the December data will carry more signal to the market and Fed than the highly unusual November report, which was both delayed and abbreviated (no October Household Report/unemployment rate) due to the federal government shutdown. Additionally, there were apparent distortions blurring the signal from the data, from the shutdown-driven jump in unemployment, to the new historical low for the household survey response rate and higher standard errors.

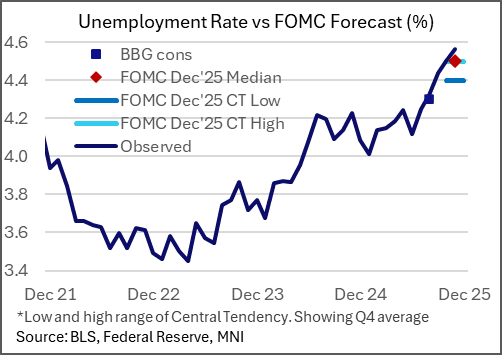

- Note that the FOMC's December 2025 median for the Q4 unemployment rate was 4.5% so a steady rate from November would imply a dovish "miss" to the upside though the significance will be muted by the noise in the household data. That said with Fed Chair Powell stating last month that nonfarm payroll gains are overstated by 60k/month, the consensus expectation will - to the leadership of the FOMC - imply only continued softness in the labor market, keeping further rate cuts in play this year.

- So far, indicators point to a relatively steady labor market overall in December vs November. The Chicago Fed's advance estimate of December's unemployment rate is 4.56% - which would be unchanged from November's unrounded BLS reading.

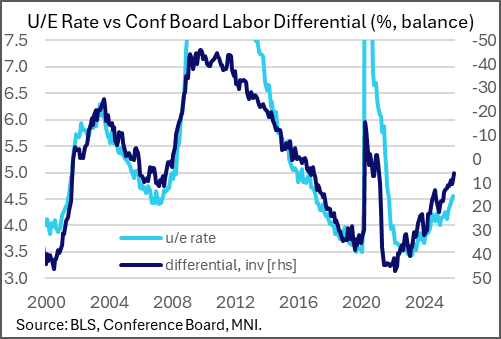

- The "labor differential" in the December Conference Board consumer survey its lowest since February 2021 at 5.9, pointing to a continued pickup in the unemployment rate, while the UMIchigan survey's expected job changes expected during the next year remains at levels consistent with meaningful monthly nonfarm payrolls contractions.

- However, jobless claims data for the reference week were on the lower side of the range seen in recent months' reference periods (initial 224k, continuing 1,913k in Dec 13 week).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Has Cleared Short-Term Trendline Resistance

- RES 4: 0.6660 High Sep 18

- RES 3: 0.6640 76.4% retracement of the Sep 17 - Nov 21 bear leg

- RES 2: 0.6618 High Oct 29 and a key near-term resistance

- RES 1: 0.6600/6598 High Dec 03 / 61.8% retracement of the Sep 17 - Nov 21 bear leg

- PRICE: 0.6596 @ 16:44 GMT Dec 3

- SUP 1: 0.6517 20-day EMA

- SUP 2: 0.6466/21 Low Nov 26 / 21

- SUP 3: 0.6415 Low Aug 21 / 22 and a bear trigger

- SUP 4: 0.6404 38.2% retracement of the Apr 9 - Sep 17 bull cycle

AUDUSD continues to appreciate and price action remains above the 20- and 50-day EMAs. This week’s gains have resulted in a breach of a short-term trendline resistance at 0.6544, drawn from the Sep 17 high. The break strengthens a bull theme and highlights a stronger reversal, testing 0.6598 next, a Fibonacci retracement. First support is at 0.6512, the 20-day EMA. A move below this average would signal a possible reversal.

US TSYS: Tsys Grind Off Midmorning Lows, Mixed Data Ahead Thursday Weekly Claims

- Treasuries look to finish moderately firmer Wednesday - off early morning highs following a flurry of economic data.

- TYH6 currently +7.5 at 113-04 vs. 113-07 high, initial technical resistance at 113-11/22+ High Dec 1 / High Nov 25.

- The ISM services index was stronger than expected in November as it inched higher to 52.6 (cons 52.0) after 52.4 in October, marking its highest since February. The S&P Global US services PMI continues to offer a more optimistic assessment of current activity despite being revised down in its final November release to 54.1.

- ADP employment growth “surprised” lower at -32k (Bloomberg cons 10k) in November whilst the October increase was revised up from 42k to 47k.

- The S&P Global US services PMI was revised lower in the final November release 54.1 (flash & cons 55.0) in Nov final after 54.8 in Oct, dipping to its lowest since June rather than confirming what had been its highest since July.

- Stocks continue to plow higher Wednesday, recovering from early session lows after Microsoft denied a write-up from "The Information" they had lowered "AI software sales quotas". Pretty specific, nevertheless, while market concerns over stretched AI-tied valuations are on full display.

- Charles Gasparino at Fox Business reports on X that there is a 'last-ditch' effort by Wall Street and corporate America insiders to caution President Donald Trump against nominating National Economic Council Director Kevin Hassett as Federal Reserve Chair.

- Look Ahead Thursday Data Calendar: Challenger Job Cuts, Weekly Claims, Revelio & Regional Fed Data.

US TSYS: Late SOFR/Treasury Option Roundup: Large Low Delta Trades

SOFR & Treasury options remained mixed after better downside put interest early overnight. Underlying futures well off midmorning lows - still off early morning highs. Projected rate cut pricing mixed vs. early morning levels (*): Dec'25 at -23.6bp (-24.6bp), Jan'26 at -31.4bp (-31.8bp), Mar'26 at -40.4bp (-39.8bp), Apr'26 at -47.9bp (-46.3bp).

- SOFR Options:

- +6,000 SFRZ5 96.12 puts, .25 vs. 96.2825

- +15,000 SFRF6 96.50/96.75 call spds 2.0-2.75 over 96.37 puts ref 96.465

- +4,000 SFRH6 96.75 calls, 4.0 vs. 96.475/0.20%

- 2,089 SFRZ5 96.12/96.18/96.25 call flys

- 2,000 0QZ5 96.81/96.87/97.00/97.06 call condors ref 96.95

- 3,500 SFRZ5 96.31/96.37 call spds ref 96.275

- 5,000 SFRZ5 96.25/96.31 call spds ref 96.2725

- over 9,600 SFRZ5 96.31 calls ref 96.2725

- 3,000 SFRH6 96.00 puts ref 96.445

- +6,000 SFRZ5 96.25/96.37 put spds, 9.0

- +5,000 SFRZ5 96.18/96.25 put spds, 0.75

- +7,500 SFRH6 96.18/96.25/96.31 put trees, 0.0 vs. 96.405/0.02%

- +6,000 SFRH6 96.18/96.31/96.37 broken put flys, 2.0

- over -4,100 SFRM6 98.00 calls, 2.0 ref 96.715/0.04%

- +1,850 SFRF6 96.56/96.75 call spds, 2.75 vs 96.46/0.18%

- Treasury Options:

- -5,000 TYF6 112.5/113.5 strangles, 39

- +84,361 wk2 Fri 30Y 106 puts, cab-7**

- 3,000 Wed wkly 113.5 calls ref 113-03.5 (exp today)

- 2,000 USG6 108 puts ref 116-21

- -2,500 TYF6 114/114.75 call spds, 9 vs. 113-08/0.12%

- +2,000 USG6 108/112 3x1 put spds, 6 ref 116-14

- 2,000 USF6 125.5 calls ref 116-16

- +1,750 FVF6 111 calls, 3 vs. 109-20.5/0.08%

- +7,600 Wed wkly 113 calls ref 112-28 to 30 (exp today)

- tyf6 114/114.75 cs vs 113-08 12% seller 9s 2500x 648am

- **File under patently absurd low-delta 30Y put trade:

84,361 wk2 30Y 106 puts trade on screen at cab-7

The 10 handle out-of-the-money option expires next week Friday - after the final FOMC of 2025. while markets are widely anticipating a 25bp rate cut on December 10.

Most likely a hedge vs some short term balance sheet risk that corresponds to a rise in 30Y yield to (rough) appr 5.48% from current yield of 4.73%. (Two caveats: bond cheapest to deliver will change to a higher duration bond most likely; the duration on US 30y cash and USH prob ably won't shift in parallel.)

There has been a rise in low delta option trades - Treasury & SOFR - on both sides of the curve over the last few sessions. SOFR has seen rise of par (100 strike) and above call options in midcurves targeting early 2026.