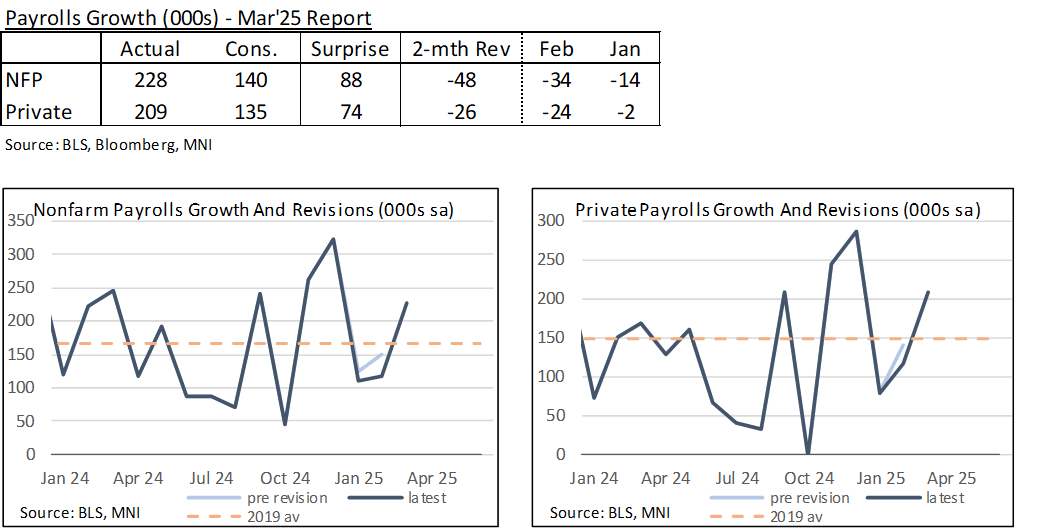

US DATA: Payrolls Beat Expectations, Downward Revision Concentrated In Feb

Apr-04 12:43

- A sizeable 88k beat for payrolls (228k vs cons 140k) in March, most of which came from the private sector.

- The government added 19k of seasonally adjusted jobs, with federal a modest -4k after the -11k in Feb.

- The beat was somewhat offset by the -48k two-month nonfarm downward revision, mostly in Feb (-34k) rather than Jan (-14k).

- Private sector two-month revision of -26k, almost entirely in Feb.

- Revision table and charts below:

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Early SOFR/Treasury Option Roundup, 10- & 30Y Call Spreads

Mar-05 12:42

Better 10- and 30Y call trade reported overnight, lighter SOFR option volume more pared with some recent midcurve put spread activity. Underlying futures mostly weaker, off lows, curves steeper with short end rates outperforming. Projected rate cuts through mid-2025 steady to mildly firmer vs. late Tuesday levels (*) as follows: Mar'25 steady at -1.8bp, May'25 steady at -12.2bp, Jun'25 at -29.2bp (-28.9bp), Jul'25 at -39.8bp (-38.8bp).

- SOFR Options:

- Block, 3,000 0QM5 95.81.96.06.96.31 put flys, 4.0 vs 96.425

- Block, 8,000 0QK5/0QQ5 95.62 put strips, 2.0

- 2,000 SFRZ5 95.43/95.62/95.81 put flys ref 96.375

- 3,000 0QH5 96.75/97.00 call spds ref 96.42

- 4,000 2QM5 96.50/97.00 call spds ref 96.39

- 2,500 SFRZ5 96.12/96.37 call spds ref 96.355

- 1,750 0QK5 96.50/97.00/97.25 broken call flys ref 96.47

- Treasury Options:

- 2,000 FVM5 109/110 call spds ref 107-28.75

- 5,000 USK5 112/125 strangles ref 117-29

- over 5,500 USJ5 119 calls, 50 last

- over 5,100 USJ5 120 calls, 31 last

- 2,000 USJ5 114.5/115.5 put spds ref 117-23

- appr +20,000 TYJ5 109.75/112.5 combos on 1:1 ratio, +c 0.0-1 in pieces followed Block

- Block, -10,000 TYJ5 109.75/112.5 3x2 combo, 11 net/put sold over vs. 110-31.5/0.57%

EUR: Differing Analyst Views as Euro Rally Develops

Mar-05 12:16

- *Deutsche Bank note the biggest and fastest fiscal policy shift in post-unification German history exceeded even their optimistic expectations. Recall that last week DB turned from bearish to neutral on EURUSD, and the latest developments prompt them to shift to an outright bullish view.

- For now, Deutsche go long EURUSD targeting 1.10, noting that that their rate differential models are already up at 1.09. They will be re-assessing their more medium-term dollar views as the newsflow progresses.

- *HSBC: German fiscal optimism will support EUR-USD in the near-term but it's worth bearing in mind that other factors will also impact EUR-USD. Recent softer US data has pushed US Treasury yields lower, weighing on dollar strength and Friday’s US jobs data will also be key. Additionally, US trade tariffs on the EU loom on the horizon while any EUR peace dividend relies upon a peace deal being successfully agreed.

- *Rabo: On the back of the news that Germany is poised to change its constitution to enable more fiscal spending, Rabo have raised their one-month forecast for EURUSD to 1.07. They will publish fresh EUR forecasts out to 12 months at the end of this week.

- *ING note the problem for the EUR/USD story here is that the fiscal news has not moved the needle on ECB policy expectations. The forward ESTR curve still prices the low point for the ECB easing cycle near 1.75%. No doubt this is a function of the global tariff threat which looks like it will be coming Europe's way next month.

- ING haven't been calling for such a decisive upside break in EUR/USD, and don't yet buy into this talk of the dollar losing its reserve currency status. This looks more of a cyclical decline on soft US data this year. For the near term, however, US activity data will probably be the determinant of whether we trade up to 1.0800. EUR/USD maybe more of a 1.03/04 story when broader US tariffs come in next month, compared to ING’s prior forecasts of 1.00/02 in coming quarters.

- *MUFG: More tariff action is very likely still coming for Europe, which in MUFG’s view will limit EUR/USD upside from these levels. Trump last night in his address to Congress was clear that the EU would be hit with tariffs. With US yields rebounding last night and Trump sounding very aggressive on future tariff action on the EU and others, MUFG are unconvinced that this move higher in EUR will extend much further. Leveraged Funds have been short EUR, but positioning has already been reduced and is not extreme by historical comparison.

US DATA: Mortgage Refis Sensitive To Limited Declines In Mortgage Rates

Mar-05 12:16

- MBA composite mortgage applications jumped 20% last week (sa) to more than reverse a 12% decline over the prior two weeks.

- Refis jumped 37% after a cumulative 11% two-week decline, whilst new purchases increased 9% after a two-week decline of -13.5% (as part of a five-week decline totalling -19%).

- Refis have proven sensitive to declines in lending rates despite the outright level still being high. The 30Y conforming rate fell 15bps to 6.73% for what’s now a 36bp drop since the recent high of 7.09% in January, although is still elevated compared to lows of 6.13% seen in September on then expectations of a more prolonged Fed cutting cycle.

- A reminder of how depressed mortgage activity remains though: new purchases are at 56% of 2019 averages whilst refis are at 45%.