EM LATAM CREDIT: Panama: USD1.5bn Spending Reallocation – Negative

(PANAMA; Baa3neg/BBB-/BB+)

• The National Assembly budget committee recommended a reallocation for the 2026 budget that would add to spending for education, science and health of USD1.5bn. We didn’t see what cuts would be made to allow for that. President Mulino called for an extraordinary cabinet meeting on October 13th to discuss the recommendations. It’s important to see how the govt will contain spending.

• Panama 35s were last quoted T+178bp, 75bp tighter since June 30th and 136bp tighter YTD. The trigger for the strong performance was an improving fiscal situation that materialized in 2Q. We are concerned about Moody’s downgrade to junk in the next couple of months that is not factored into current spreads.

• A Moody’s downgrade would result in the bonds having high yield ratings from two of the three major rating agencies which could lead to some forced selling. Moody’s negative outlook was initiated in November 2024 last year and twelve months is the typical time frame that is given to evaluate whether a change is needed.

• Public spending rigidities in the budget may not have been dealt with sufficiently according to Moody’s analyst Renzo Marino who warned last month at a Latam Panama conference that the country was on the verge of losing its investment grade rating, as reported by Newsroom Panama. The govt update February 2025 to the social and fiscal responsibility law targets a fiscal deficit of 4% for 2025 and gradually decline to 1.5% in five years. That followed a fiscal deficit in 2024 north of 7% which triggered an S&P downgrade to BBB- and the negative outlook from Moody’s.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Eyes on PPI, Cash 2s10s Remains Dis-Inverted, 3Y Stops Through

- Treasuries look to finish weaker, off late morning lows with rates paring losses after a decent $58B 3Y Note auction broke a four consecutive auction run of tails w/ 3.485% high yield vs. 3.492% WI; 2.73x bid-to-cover vs. 2.53x prior.

- After some sharp two-way action - Tsys retreated after BLS Prelim Benchmark Revision to Establishment Survey Data comes out much lower than anticipated: -911k vs. -682k est from -818k prior.

- Meanwhile, Johnson Redbook Retail Sales Index rose 6.6% Y/Y in the first week of September (ending Sep 6), running a little above retailers' targeted 6.3% gain for the month.

- Currently, the Dec'25 10Y trades -6.5 at 113-11 (yld 4.0722 +.0324) vs. 113-07 low -- Initial firm support to watch is 112-11+, the 20-day EMA. Yield curves flatter: 2s10s -2.311 at 52.831, 5s30s -1.536 at 114.416. Cash 2s10s adjusted for carry/rolldown remains dis-inverted 58.9.

- US$ off lows, BBG index BBDXY currently +2.6 at 1201.15 vs. 1196.68 post data low.

- Focus turns to US price data, as PPI and CPI releases are expected across Wednesday and Thursday respectively. China CPI and PPI figures will be released during APAC hours tomorrow.

AUDUSD TECHS: Approaching The Bull Trigger

- RES 4: 0.6688 High Nov 7 ‘24

- RES 3: 0.6677 0.764 proj of the Jun 23 - Jul 11 - 17 price swing

- RES 2: 0.6625 High Jul 24 and the bull trigger

- RES 1: 0.6620 High Sep 9

- PRICE: 0.6595 @ 17:42 BST Sep 9

- SUP 1: 0.6522 20-day EMA

- SUP 2: 0.6463/6415 Low Aug 27 / Low Aug 21 / 22 and a bear trigger

- SUP 3: 0.6373 Low Jun 23

- SUP 4: 0.6354 38.2% retracement of the Apr 9 - Jul 24 upleg

AUDUSD traded higher again Tuesday to build on the latest gains and remains firm. The current bull cycle confirms the end of a corrective phase that started on Jul 24. Resistance at 0.6569, the Aug 14 high, has been cleared. This exposes key resistance and the bull trigger at 0.6625, the Jul 24 high. Support to watch is 0.6415, the Aug 21 / 22 low. A clear break of it would instead resume a bear leg and highlight a stronger reversal.

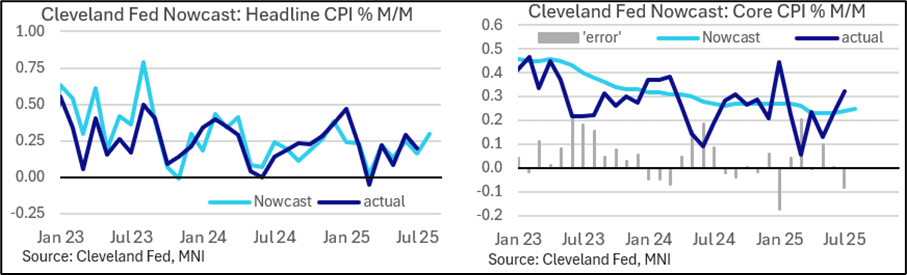

US INFLATION: Cleveland Fed Nowcast CPI Tracker Points To August Pickup

The Cleveland Fed nowcast has headline CPI at 0.30% M/M and core CPI at 0.25% M/M in August. That headline estimate is the nowcast’s highest of the year (the only one higher in the last 15 months was December 2024’s 0.38%) and comes after two consecutive 0.04pp underestimates of the actual figure (July: 0.16% vs actual 0.20%).

- The core tracker meanwhile is a the highest since March, after undershooting the actual in July (0.24% vs 0.32% actual, biggest undershoot since January) after an accurate reading in June (0.23%).

- MNI median unrounded est for core is 0.32% M/M, and for headline 0.36%