FOREX: Onshore & Offshore Yuan Trading Further Below 7.00

In EM Asian FX, the focus remains on the yuan. The offshore CNH against the US dollar was trending lower before today’s fixing and has continued the move falling 0.1% to 6.9835 after a low of 6.9818. Bloomberg fixing estimates were below 7.00 but it came in at 7.0288, driving the error wider. USDCNY fell to a low of 6.9880 and is currently down 0.1% to 6.9888. The BBDXY USD index is slightly higher.

- Officials warned on the weekend against making bets on yuan strengthening but it has continued this week signalling some acceptance in China of currency appreciation.

- President Xi said that the economy is on track to achieve the 5% growth target and that there will be more proactive macroeconomic policies in 2026. December PMIs printed above expectations and the breakeven 50-level.

- The Indonesia rupiah is outperforming with USDIDR down 0.4% to 16698 today after reaching 16790 on Monday. Rupiah depreciation has held Bank Indonesia’s hand in Q4 after easing 75bp in Q3. It is likely to want a stronger currency before resuming rate cuts.

- USDTWD is up 0.1% to 31.428 off the intraday low at 31.387.

- Some spot Asian currencies are not trading due to New Years’ holidays.

- Later US jobless claims print. European stock markets are either closed or have early finishes, which includes the UK.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

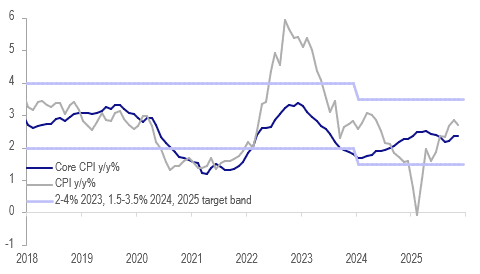

INDONESIA: BI Looking To Cut Again, Inflation Stable But Need Stronger IDR

Headline inflation moderated 0.2pp to 2.7% y/y as volatile fresh food inflation eased 1.1pp to 5.5% y/y in November. Core held steady at 2.4% y/y, which was slightly more than consensus forecast. Bank Indonesia Governor said today there is room for further easing and that it just depends on timing and the stabilisation in inflation should allow it to cut rates again when it is confident that the rupiah has stabilised.

- USDIDR is down 0.5% to 16,661 since the 19 November BI decision to keep rates unchanged but this has been helped by a weaker US dollar as Fed rate cut expectations have increased. The BIS IDR NEER was flat in November which is a step in the right direction towards FX stability.

- The S&P Global November PMI reported that cost pressures increased in Indonesia due to the weaker IDR and raw materials and were passed on resulting in highest selling inflation in more than 18 months. This is a trend that will be monitored.

- In October a large jump in personal care & others inflation to 11.9% y/y from 9.9% drove the increase in core inflation. The rise was due to higher global gold prices. They were up almost another 6% over November and so it is not surprising that personal care & others picked up further to 12.5% y/y keeping underlying inflation at 2.4%. Other components saw steady rates.

- The drop in fresh food inflation fed into lower price changes for dining out and general food & drinks components.

Indonesia CPI y/y%

Source: MNI - Market News/LSEG

ASIA STOCKS: UEDA Spooks Japanese Stocks; Korea and Taiwan Follow Suit

Global rate expectations continue to impact investor optimism with risk appetite strong in most major bourses today. Whilst US rate sensitive markets continue to position for a rate cut in the US, markets are seeing a potential BOJ rate hike in December, which has caused the yen to firm and the Nikkei to fall. Governor Kazuo Ueda has indicated the bank will consider the pros and cons of an increase. In India, stronger than expected GDP results came ahead of this week's Reserve Bank of India's decision on rates which is widely expected to see a rate cut to stem the decline in inflation. The focus on AI tech remains a key thematic with names like TSMC's fall today a key driver to the decline of the TAIEX in what local press are suggesting is profit taking. This is likely to be an ongoing theme into year end given the extraordinary run up in recent months of AI / Tech names like TSMC and key equities in Korea and Japan.

- UEDA's comments wasn't well received by the NIKKEI with it starting the month and the week off with a fall of -1.8%, dragging the KOSPI with it with falls of -0.16%.

- China's major bourses are all up with the Hang Seng leading the way with gains of +0.80%, followed by the CSI 300 up +0.75%

- The TAIEX in Taiwan is down modestly by -0.44% with risk sentiment looking less robust into year end.

- The NIFTY 50 was buoyed by the better than expected GDP and talk of a rate cut this week sees it start Monday up +0.28% to a new high of 26,278

- SE Asia' s bourses are starting the month off strongly with the FTSE Malay KLCI leading the way up +1.1% following better than expected Manufacturing PMIs.

JGBS: Futures Testing Cycle Lows Post Ueda Speech, Dec Hike Odds Near 80%

JGB futures are holding close to session lows in latest dealings, last 134.50, -.63 versus settlement levels, as BoJ Governor Ueda said a rate hike in Dec would be considered. For 10yr futures, we are challenging the Nov 19 and cycle low of 134.56. A clean break lower points to the low 134.00 region , (with 134.04 being the 1.0% 10-day DMA envelope). Market implied BoJ rates for the Dec meeting sit around 0.675%, (roughly a 79% chance of hike in Dec). We were at 0.535% this time last week.

- Bank of Japan Governor Kazuo Ueda said on Monday that the BOJ will consider the pros and cons of raising the policy interest rate and make decisions as appropriate at its Dec. 18-19 meeting. He added that that raising the policy interest rate under accommodative financial conditions should be seen as easing off the accelerator toward stable economic growth and price developments, rather than applying the brakes on economic activity.

- Ueda also expressed confidence in the wages outlook, while noting downside risks for both the US and Japan economies have lessened.

- In the cash JGB space we are around 5-6bps higher for 5-20yr tenors. The 10yr outright yield is at 1.86%, fresh cycle highs. The 2yr is around 1.00%, while the 30 is up 4bps to 3.39%. Th 2/30s curve is little changed at +237.5bps.

- Earlier data on Capex was weaker than forecast but was largely ignored by the market.

- Note tomorrow we have a 10yr JGB auction.