BELGIUM T-BILL AUCTION PREVIEW: On offer next week

Dec-05 13:18

Belgium has announced it will be looking to sell a combined E2.8-3.2bln of the following at its auction next Tuesday, December 9:

- An indicative E1.2bln of the Mar 12, 2026 TC

- An indicative E1.8bln of the new Dec 10, 2026 TC

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Post-ADP React

Nov-05 13:18

- Treasuries declining after larger than expected Oct ADP jobs gain. Currently, the Dec'25 10Y contract trades 0.0 at 112-25, 10Y yield 4.0929% (+.0077), curves mildly steeper (2s10s +.136 at 50.865; 5s30s +.312 at 97.021).

- A short-term bearish threat in Treasuries remains present. Recent weakness has resulted in a breach of the 50-day EMA, currently at 112-26+. This highlights potential for a deeper retracement near-term. A continuation lower would open 112-06, the Sep 25 low and the next key support. The contract needs to trade above 113-18+, the Oct 28 high to signal a possible bullish reversal. Key resistance and the bull trigger is at 114-02, the Oct 17 high.

- USD only marginally gains on the back of the stronger-than-expected headline - helping both EURUSD and GBPUSD edge away from any test on earlier highs. All-in-all the reaction is largely contained, however USDJPY is pressuring 153.84 and the best levels of the day.

- Next up: US Tsy Quarterly Refunding annc at 0830ET followed by S&P Global US Services/Composite PMI at 0945ET.

US TSYS/SUPPLY: No Change To Coupon Size Guidance, But Bills Eyed in Refunding

Nov-05 13:11

A few areas to watch in today's 0830 Refunding announcement - MNI's full preview is here

- Guidance: We do not expect Treasury’s guidance on coupon issuance to change in this Refunding round ("Treasury anticipates maintaining nominal coupon and FRN auction sizes for at least the next several quarters.")

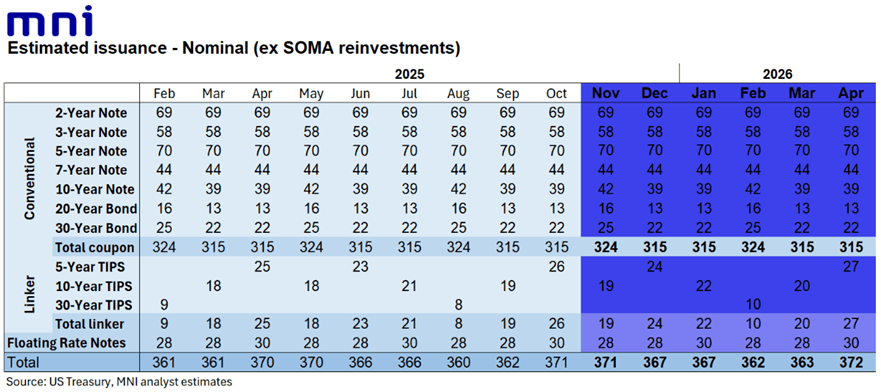

- Coupon sizes for upcoming quarter (Nov-Jan): As seen in table below. The Refunding itself will be $58B in new 3Ys, $42B in new 10Y, and $25B in new 30Y for next week.

- Buybacks: After being in some focus in August's Refunding, we don’t expect any changes to buyback program parameters this time, following the last round’s amendments that included higher-frequency operations/increasing the size of long-end buybacks. There are some risks that buyback sizes could be slightly increased, or that Treasury announces that the list of eligible counterparties will be expanded.

- Bill guidance: This will be of some interest given that borrowing expectations for the coming quarter were at the lower end of the expected range - one thing to watch will be if Treasury guides to reducing bill auction sizes soon having increased them significantly in late September/early October, helping push the TGA cash pile to the $1T mark. Last time that guidance read: "Treasury anticipates further marginal increases in short-dated Treasury bill auction sizes in the coming days and then maintaining sizes at or near those levels through the end of September. Additional increases to Treasury bill auction sizes are anticipated in October. Treasury will carefully monitor market conditions and adjust its bill issuance plans as appropriate. "

STIR: Repo Reference Rates

Nov-05 13:05

- Secured Overnight Financing Rate (SOFR): 4.00% (-0.13), volume: $3.147T

- Broad General Collateral Rate (BGCR): 3.98% (-0.11), volume: $1.183T

- Tri-Party General Collateral Rate (TCR): 3.98% (-0.11), volume: $1.156T

- (rate, volume levels reflect prior session)