EU-BILL AUCTION PREVIEW: On offer next week

Nov-14 11:00

The EU has announced it will be looking to sell the following at its auction next Wednesday, November 19:

- Up to E1.0bln of the 3-month Feb 6, 2026 EU-bill

- Up to E1.0bln of the 6-month May 8, 2026 EU-bill

- Up to E1.0bln of the 12-month Nov 6, 2026 EU-bill

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US MBA: MARKET COMPOSITE -1.8% SA THRU OCT 10 WK

Oct-15 11:00

- MNI: US MBA: MARKET COMPOSITE -1.8% SA THRU OCT 10 WK

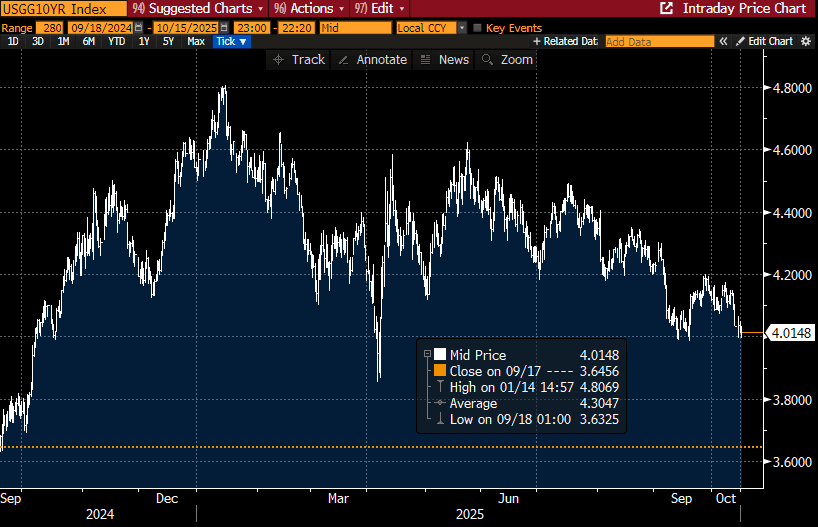

US TSYS: Another Short-Lived Probe Of Sub-4% 10Y Yields

Oct-15 10:56

- Treasuries are within overnight ranges but hold firmer on the day, underperforming EGBs which benefit from yesterday’s easing of near-term French political risks.

- Today sees calendar focus on the NY Fed Empire Survey for a latest look at regional manufacturing activity/sentiment before the Fed’s Beige Book. Earnings season also continues, with BofA results currently well-received and Morgan Stanley still to come.

- Cash yields are 0.5-2.5bp lower across the curve, bull flattening.

- 10Y yields (currently 4.0148%, -1.7bps) again tested the 4% handle earlier with a low of 3.9975% after yesterday’s 3.9976%, but are finding support at this level. Whilst there were brief clearances on Sep 17 and Sep 11, yields were last materially sub-4% in early April under reciprocal tariff deliberations.

- TYZ5 trades at 113-13+ (+00+) on modest cumulative volumes of 270k.

- An earlier high of 113-17+ matched that from yesterday, in signs of some resistance ahead of a bull trigger at 113-29 (Sep 11 high). The recent uplift has dragged support up to 112-26 (20-day EMA).

- Data: MBA mortgage applications (0700ET), Empire mfg Oct (0830ET), Beige Book (1400ET). Today’s CPI report has been rescheduled to Oct 24.

- Fedspeak: Miran (0930ET), Miran (1230ET), Waller (1300ET) and Schmid (1430ET) – see FED bullet.

- Bill issuance: US Tsy $69B 17W bill auction (1130ET)

- Politics: Trump participates in press conference with FBI Director (1500ET), Trump hosts Ballroom Dinner (1930ET)

- Earnings: Morgan Stanley still to report along with Abbot Labs and Prologis pre-market. BofA has already reported, beating trading revenue estimates. MNI Earning Calendar found here.

OUTLOOK: Price Signal Summary - Another Cycle High In Gold

Oct-15 10:54

- On the commodity front, a bull cycle in Gold remains intact and this week’s extension reinforces current conditions. The move higher maintains the price sequence of higher highs and higher lows. Sights are on $4239.7, the 3.000 projection of the May 15 - Jun 16 - 30 price swing. Note that the trend is in overbought territory. A move down would be considered corrective and would allow the overbought set-up to unwind. Support lies at $3889.3, 20-day EMA.

- A bearish theme in WTI futures remains intact and Tuesday’s fresh cycle low reinforces current conditions. The move down last week resulted in a break of support at $60.40, the Oct 2 low. This highlights an extension of the bearish price sequence of lower lows and lower highs and the move down opens $57.50 next, the May 30 low. On the upside, key resistance is at $66.42, the Sep 29 high. First resistance is at $62.47, the 50-day EMA.