US: OMB Targets Federal Funding In Democrat-Led States

Jan-22 16:55

CNN reports: https://edition.cnn.com/2026/01/22/politics/trump-federal-funding-democratic-st ates th...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

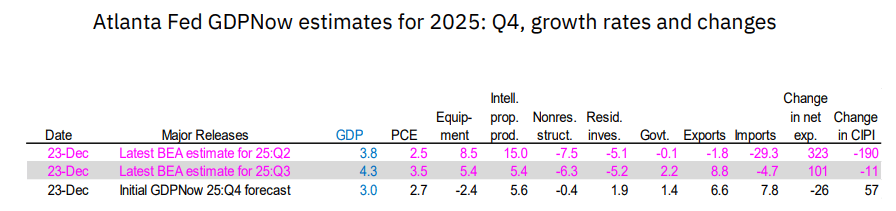

US DATA: Initial Atlanta Fed GDP Nowcast Points To Only Slight Slowdown In Q4

Dec-23 16:55

The Atlanta Fed's initial GDPNow estimate for Q4 GDP growth is 3.0% Q/Q SAAR. That comes after the surprisingly strong 4.3% in Q3 but would also represent a slowdown from the 3.8% in Q2, albeit solid by almost any reasonable measure.

- The initial breakdown includes a slowdown in PCE to a still-robust 2.7% (after 3.5% in Q3), which is the main driver of growth.

- The 2nd biggest contributor is set to be intellectual property investment (5.6% growth after 5.4%), with a modest rebound in residential investment (+1.9% after -5.2%) and continued solidity in government spending (1.4% after 2.2%).

- On the downside, equipment investment is seen contracting by a fairly sharp 2.4% (after 5.4% prior), which would be the worst quarter in a year in this category.

- In non-final domestic demand categories: net exports are also seen as a drag with inventories contributing after a Q3 GDP subtraction.

- GDP growth of 3.0% would be in line with the Dallas Fed's weekly index that points to a reading in the 2.5-3.0% region through mid-December; the Dallas Fed's index accurately estimated a reading above 4.0% whereas the Atlanta GDPNow undershot (at 3.5%).

FOREX: US GDP Prompts Limited Dollar Rebound

Dec-23 16:50

- After steadily weakening from the open this week, a much firmer-than-expected US GDP print has stalled the greenback’s downside momentum. Following the USD index printing a fresh pullback low at 97.85 in early trade, the data has sparked only a moderate rebound (owing to some question marks over the release), with the DXY operating around 98.05 as we approach the APAC crossover. Dollar dynamics did produce a notable pullback for spot gold, which had a near $70 pullback to $4,430/oz.

- Across the G10, it was JPY volatility that stole the show once again. Both the finance minister comments on potential intervention and a responsible tone from PM Takaichi provided a supportive backdrop early Tuesday. USDJPY extended its pull lower this week to erase the entirety of the post BOJ rally from Friday. This resulted in session lows of 155.65, before recovering around 85 pips following the US growth figures. Short-term technical parameters are well defined at 154.40 (50-day EMA) and 157.89 (key resistance and bull trigger).

- Continued positive sentiment for equity markets has underpinned solid gains for both AUD and NZD, which top the G10 leaderboard. AUDUSD has traded to within 7 pips of the key 0.6707 level, the Sep 17 high.

- Elsewhere, USDCAD also gathered downside momentum this morning. A break of multiple daily lows at 1.3727 is noteworthy, placing USDCAD at the lowest level since late July with prints below 1.3700. Overall, USDCAD has now extended its one-month selloff to around 3%, with the breach of the bull channel in early December exacerbating declines.

- Both EURUSD and GBPUSD had attempts at breaking the 1.18 and 1.35 levels respectively, although topside momentum certainly dissipated across the US session.

- US jobless claims are scheduled tomorrow, although market liquidity is likely to be heavily impacted by the upcoming holiday period.

US STOCKS: Extending Higher While Strong Data Tempers Rate Hike Expectations

Dec-23 16:50

- Major US equity indexes are extending higher Tuesday, looking past this morning's stronger economic data (Q3 GDP +4.3%) that tempered rate hike expectations through mid-2026 (June '26 the first FOMC date to price in a 25bp cut).

- Currently, the DJIA trades up 68.89 points (0.14%) at 48430.42, S&P E-Mini Future up 18.25 points (0.26%) at 6949, Nasdaq up 78.4 points (0.3%) at 23507.84.

- Information Technology and Communication Services sector shares led advances in the first half, chip makers buoyed after the Trump administration announced a tariff delay on China until 2027.

- "A filing from the trade office said the government would impose an initial tariff of zero percent on Chinese semiconductors exports before increasing it in June 2027 by an undetermined amount," the NY Times reported.

- NVIDIA +1.93%, Jabil +1.73%, Broadcom +0.99%, Dell Technologies +0.84% and Teradyne +0.57%.

- Meanwhile, Warner Bros Discovery +1.25%, Alphabet +1.21%, Live Nation Ent +1.16%, AT&T +0.72% and Verizon Communications +0.35% buoyed the Communications sector.

- Conversely, Health Care, Consumer Staples and Industrials sector shares underperformed in the first half:

- Moderna -5.64%, IDEXX Laboratories -2.10%, Insulet -1.91% and Align Technology -1.71%

- Brown-Forman -4.27%, Lamb Weston Holdings -2.66%, Campbell's Company -2.17%, Hershey -1.87% and PepsiCo -1.60%

- Delta Air Lines -1.46%, Southwest Airlines -1.42%, Builders FirstSource -1.37% and Stanley Black & Decker -1.13%.