OIL PRODUCTS: Oil Products End of Day Summary: Cracks Weaken

Cracks have faced pressure today, with wider economic concerns causing product prices to slide. Diesel cracks have dropped to their lowest level since late-June.

- US gasoline crack down 0.2$/bbl at 21.73$/bbl

- US ULSD crack down 1.9$/bbl at 29.35$/bbl

- US refining crack spreads are supported by global diesel tightness in H2 as fuel demand outpaces capacity additions and exports strengthen, Bloomberg said.

- Valero’s 205k b/d Houston Texas refinery reports maintenance activities may require the use of safety flare system per a community alert.

- US gasoline, diesel and jet fuel demand in May were all markedly higher in the EIA's monthly report compared to estimates published in the weekly data. Diesel demand climbed to 3.8mb/d in May, about 6.5% higher than the weekly averages, while jet fuel demand was 5% higher and gasoline 3% higher.

- The 105kb/d Paulsboro refinery in New Jersey has no plans to restart idled units despite a drop in European refined products imports to the East Coast, according to PBF Energy CEO Matt Lucey cited by Dow Jones.

- Valero’s Corpus Christi west refinery halted the naphtha hydrotreater at complex 1 on Thursday according to a regulatory filing.

- India’s diesel and gasoline sales in July fell from the previous month but were higher on the year, data from state-run Indian Oil and Bharat Petroleum and Hindustan Petroleum showed cited by Bloomberg.

- Japan’s ENEOS plans to conduct regular maintenance on two CDUs at its Kawasaki refinery during August to November, a company spokesperson told Bloomberg.

- The Litvinov refinery has lifted force majeure as it resumes normal activities, according to Bloomberg on Thursday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

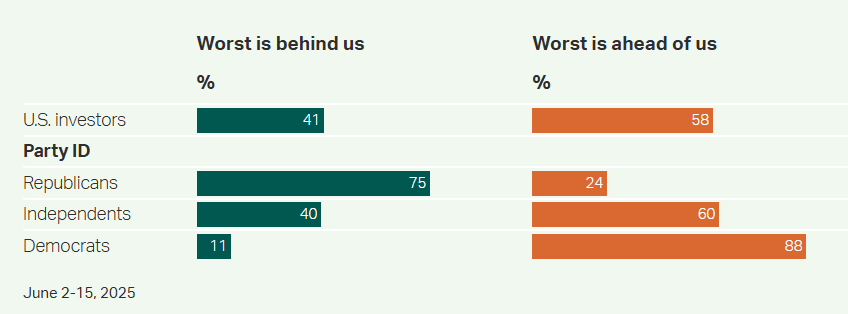

US: Partisan Split Widens On Market Volitility Expectations In 2025 - Gallup

A new survey from Gallup has found that, “Most investors foresee volatility persisting through 2025 and believe the worst is still to come, rather than “behind us.” Despite this, investor confidence in the stock market as a means of building retirement wealth remains high.”

- Gallup notes: “Democratic investors (48%) are far more likely than Republican investors (9%) to say they are very concerned about recent stock market volatility and are twice as likely to be very or somewhat concerned overall (82% vs. 41%). Concern among independents falls between the two partisan groups, similar to the national average.”

Figure 1: "In terms of market volatility this year, do you think the worst is behind us or the worst is ahead of us?"

Source: Gallup

US OUTLOOK/OPINION: Specific Private Industries Worth Watching In NFP Report

- Within industries of nonfarm payrolls, expect a continued focus on those more cyclically sensitive sectors, such as food & drinking places, for discretionary spending indicators.

- This category saw notable strength in May at +30k after +23k in April (average +11k in 2024) but maybe scope for a downward revision.

- Friday saw real consumer spending disappoint in May at -0.3% M/M (cons 0.0) with particular weakness admittedly in goods (-0.8%) but services also languished with -0.03% M/M for technically a third monthly contraction in the five months of the year to date.

- There could also be a calendar effect at play, with BofA warning that the earlier Memorial Day could weigh on leisure & hospitality more broadly.

- Transportation & warehousing should also be watched for a look at more direct impacts from US tariff policy. Recall that this category saw large downward revisions last month, leaving payrolls growth of +6k in May after -8k in April (initially +29k) and -21k in March (+3k) and changing a narrative around implications of inventory accumulation on warehousing roles in particular.

- The latest vintage points to a recent net negative impact from tariffs now having peaked with 28k and 34k monthly increases back in Nov and Dec.

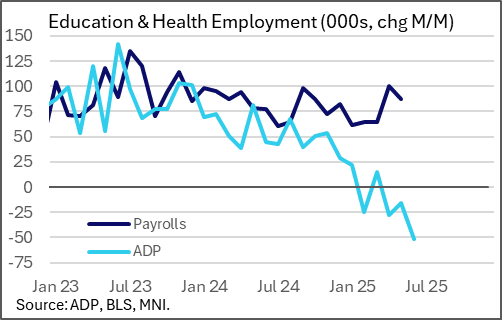

- Education & health services will also be watched closely after today's ADP employment report showed a yet further widening in what has been a puzzling disconnect with BLS payrolls.

US OUTLOOK/OPINION: Specific Factors Likely At Play In June Payrolls Report

Nonfarm payrolls growth is expected at 110k in June per the broad Bloomberg consensus after a slightly stronger than expected 139k in May but one that was offset by a large two-month downward revision of -95k.

Specific factors at play this month:

- Returning strikers to add 5.6k to payrolls, with 1.4k on strike in the June reference period vs 7k in May (SAG-AFTRA and IAM strikes concluded).

- Supreme Court allows White House to revoke Temporary Protected Status (TPS) of ~350k Venezuelans. GS see this dragging 25k whilst UBS estimate 5k with a range of 0-10k. JPM on the matter note continued uncertainty: “However, a lawsuit related to this is still ongoing, and the TPS page for Venezuela says that TPS documentation granted before February 5, 2025 will remain valid until October 2, 2026 pending resolution of the case.”

- JPM also on the Supreme Court on May 30 allowing “the government to move forward with terminating parole granted to ~530k people under the CHNV program. That does not mean every parolee, though, will be deported, as some may have other status or a pending asylum case.”