OIL PRODUCTS: Oil Products End of Day Summary: Cracks Climb on Week

US gasoline and diesel cracks are both set for a net gain this week, underpinned by ongoing refinery disruptions.

- US gasoline crack up 0.1$/bbl at 17.61$/bbl

- US ULSD crack down 0.3$/bbl at 33.76$/bbl

- Pemex completed the shutdown of multiple units at its 312,500 b/d Deer Park, Texas, refinery on Thursday to begin a multi-unit overhaul, people familiar with plant operations said.

- Saudi Aramco plans maintenance at the 305kb/d Sasref, 465kb/d Satorp and 120kb/d Riyadh refineries in Q4, according to Bloomberg sources.

- Thailand’s diesel demand fell 2.2% to an average of 66m litres per day in the first eight months of the year amid weaker economic activity, slowing exports and reduced factory output, according to the Energy Ministry cited by Bloomberg.

- CDU capacity utilisation rates at China’s state-owned refineries rose by 0.98%pts in the week to Oct. 10 to average at 82.26%, OilChem said.

- Hungary's MOL is to increase deliveries to Serbia after NIS has failed to secure another waiver from US sanctions, Hungary's Foreign Minister Peter Szijjarto said.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ECB: Macro Since Last ECB: Labour - U/E Rate At Series Lows After More Revisions

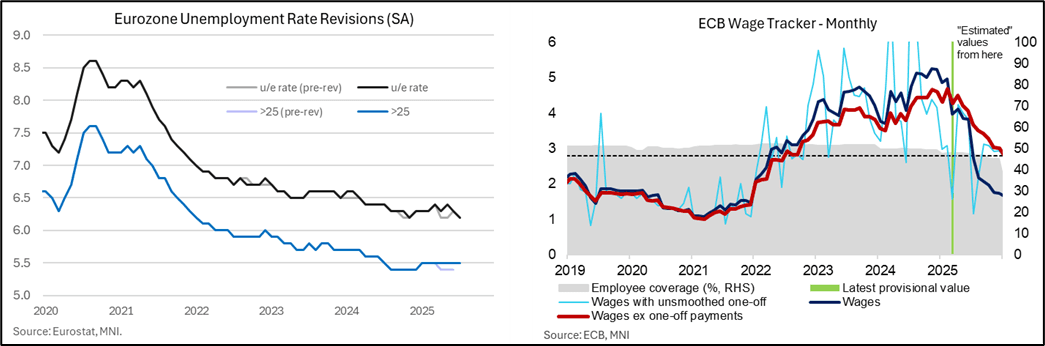

- The Eurozone unemployment rate printed at 6.2% in July as expected, a joint series low, but revisions have again altered recent trends. The data have quite often been revised and June saw a fairly typical 0.1pp upward revision to 6.3%, although the +0.2pp to 6.4% in May was more surprising.

- It leaves a trend of recent improvement but with question marks over the data. What had been seen as three months at joint cycle lows of 6.2% through Apr-Jun, tying with 6.2% in Oct-Nov 2024, Eurostat now estimate a latest pattern of 6.3% in Apr, 6.4% in May, 6.3% in Jun and 6.2% in July, tying with 6.2% only in Nov 2024.

- ECB’s Lagarde has pointed to these at-the-time historically low unemployment rates when citing the health of the labour market in recent meetings. Outright employment growth remains subdued however, with just 0.1% Q/Q and 0.6% Y/Y in Q2.

- As for inflationary pressures stemming from the labour market, Eurozone unit labour costs grew 3.1% Y/Y in Q2, down from 3.3% in Q1 for the seventh consecutive annual deceleration. This was above the ECB's 2.9% projection made in June, seemingly driven by the smaller-than-expected deceleration in total compensation per employee growth (3.9% Y/Y vs 4.0% prior, 3.4% ECB).

- While a declaration in ULC growth has allowed the ECB to deliver 200bps of easing this cycle, the data is too lagged to help determine whether further fine-tuning of the policy stance is necessary. Given the modest upward surprise to compensation per employee growth, it argues in favour of steady rates at 2.00% for now.

- ULC growth may have moderated at a steadier pace than the ECB forecast but its forward looking wage tracker released earlier in the inter-meeting process points to a continued decline in negotiated wage growth. Now with estimates out to 1Q26, it eyes wage growth excluding one-off payments at 2.6% Y/Y in 1Q26 after 3.1% in 4Q25. Overall, the results are consistent with a further softening in services inflation pressures in the coming years, in line with ECB signalling.

EURGBP TECHS: Corrective Pullback

- RES 4: 0.8769 High Jul 28 and the bull trigger

- RES 3: 0.8744 High Aug 7

- RES 2: 0.8728 76.4% retracement of the Jul 28 - Aug 14 bear leg

- RES 1: 0.8713 High Sep 2

- PRICE: 0.8653 @ 16:30 BST Sep 10

- SUP 1: 0.8636/8597 50-day EMA / Low Aug 14 and the bear trigger

- SUP 2: 0.8562 50.0% retracement May 29 - Jul 28 upleg

- SUP 3: 0.8540 Low Jun 30

- SUP 4: 0.8514 61.8% retracement May 29 - Jul 28 upleg

EURGBP traded lower Tuesday and has breached the 20-day EMA. Short-term weakness is considered corrective - for now - and support to watch lies at 0.8597, the Aug 14 low. Clearance of this level would reinstate a recent bearish threat. A resumption of gains would open 0.8744, the Aug 7 high. Key resistance and the bull trigger is at 0.8769, the Jul 28 high. Note that MA studies are in a bull-mode position highlighting a dominant uptrend.

BONDS: EGBs-GILTS CASH CLOSE: Short-End Underperformance Ahead Of ECB

EGBs and Gilts traded in mixed fashion Wednesday, with underperformance at the short end of respective curves.

- While Gilt yields remained within this week's ranges throughout the day, 10Y Bund yields touched an intraday post-Aug 7 low in early trade as markets digested overnight news of Poland downing Russian drones in its territory.

- Lower-than-expected inflationary pressures in the US producer price report saw a brief rally across global core instruments, but EGBs and Gilts were content to drift into the cash close ahead of event risk Thursday.

- The German curve twist flattened on the day, with the UK's bear flattening.

- OAT spreads were little changed albeit underperformed periphery/semi-core EGBs more widely, following overnight news that French President Macron had named centrist/ex-defence minister Lecornu as the new Prime Minister.

- While US CPI will garner significant attention, Thursday's European highlight is the ECB decision (MNI preview here in PDF).

- Along with the expected rate-hold along with communications reiterating a data dependent approach, Lagarde's characterisation of economic resilience and/or the extent to which uncertainty has been alleviated by the US-EU trade deal should help shape market reaction.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.1bps at 1.952%, 5-Yr is unchanged at 2.225%, 10-Yr is down 0.7bps at 2.652%, and 30-Yr is down 0.7bps at 3.273%.

- UK: The 2-Yr yield is up 2.6bps at 3.94%, 5-Yr is up 1.8bps at 4.055%, 10-Yr is up 1bps at 4.633%, and 30-Yr is up 0.5bps at 5.482%.

- Italian BTP spread down 0.6bps at 81.5bps / French OAT spread down 0.3bps at 80.9bps