OIL: Oil End of Day Summary: WTI Falls on Week

WTI is on higher on the day but remains on track for a net decline on the week with market focus still on downside risk from signs of a surplus.

- WTI DEC 25 up 0.6% at 59.79$/bbl

- OPEC oil output rose 50kb/d to 29.07mb/d in October, Bloomberg said.

- Russia’s crude oil production edged up in October but remained below its OPEC+ quotas, Bloomberg said.

- OPEC+’s decision to pause production hikes in Q1 26 is a precautionary move at a time when the market, according to Kpler’s Amena Bakr, cited by Dow Jones.

- Gunvor has withdrawn its offer for Lukoil’s international assets after the US Treasury Department said the oil and gas trader would never get a license.

- US President Trump signalled openness to granting Hungary an exemption from sanctions placed on Russian oil producers, though the exemption might not be needed

- China's headline Oct trade figures were weaker than forecasts, with export growth falling to -1.1%y/y, the weakest result since Feb this year.

- China total imports also moderated to 1.0%y/y from 7.4% in Sep although oil imports rose to 48.36m mt, from 47.25m mt in Sep and 8.2% higher on the year: Customs data.

- October sanctions have disrupted China’s mainstream crude flows, creating logistical challenges for Chinese NOCs, while teapots have remained resilient and benefited from wider discounts, Vortexa says.

- Oil in floating storage in Asia has surged in recent, Reuters said.

- In Q4, oil markets are expected to feel the impact of increased global production reaching the water, according to International Seaways executives.

- Mexico’s Pemex is currently in the process of assigning hydrocarbon development projects to private sector partners, Energy Minister Luz Elena Gonzalez told Congress Nov. 7.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Tsys Hold Near Post-Sep FOMC Lows, Projected Cuts Cool Slightly

- US Treasuries see-sawed off early session highs, looking to finish near lows after the September FOMC minutes release, curves twist flatter with the short end underperforming. TYZ5 currently -2 at 112-19.5 vs. 112-17 low.

- Standout headline out of the September FOMC minutes release is that "most" participants "judged that it likely would be appropriate to ease policy further over the remainder of this year". But this isn't a surprise when looking at the Dot Plot that emerged from the meeting that showed 12 of 19 members eyeing at least one further cut.

- Projected rate cut pricing has cooled vs. early morning levels (*): Oct'25 at -23.1bp (-23.7bp), Dec'25 at -44.6bp (-45.1bp), Jan'26 at -54.6bp (-55.2bp), Mar'26 at -64.5bp (-66.5bp).

- Treasury futures gradually retreated after the $39B 10Y note auction re-open (91282CNT4) tailed earlier: drawing 4.117% high yield vs. 4.112% WI; 2.45x bid-to-cover vs. 2.65x prior.

- There was no breakthrough in the gov't shutdown today - both of the Senate votes have now failed. Either bill needed 60 votes: the Republican funding bill vote was 54 yes/45 no, while the Democratic package was defeated 47-52. This means that no members changed their votes vs prior. There's a chance we get another set of votes Thursday.

- The dollar index added to recent gains, putting the greenback to its highest levels since early August - contrasting with more fragile, political risk-tripped, trade in the EUR and JPY.

- Thursday's weekly Jobless Claims and Wholesale Trade Sales/Inventories suspended due to the Gov shutdown.

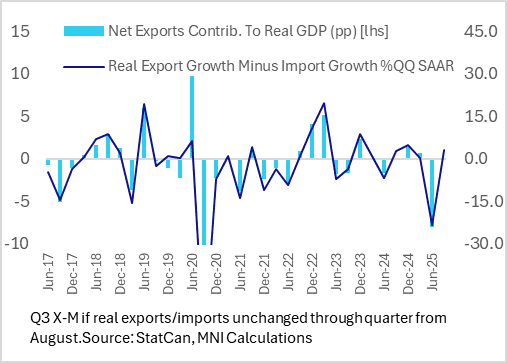

CANADA DATA: Trade Continues To Looks Marginally Positive For Q3 GDP

The sharp (~3% M/M) drop in export volumes in August reported Wednesday saw the 3M/3M annualized rate of growth remain very negative, at -9.3%. While that's an improvement from the -31% in June - driven by the US-Canada trade war - it's still a sharper contraction seen than the 5.2% 3M/3M drop in import volumes in August.

- As long as import volume growth exceeds that of export growth in September by at most 3pp, however, we estimate net exports will contribute positively to growth in the 3rd quarter. That would be the case with a flat increase in both import and export volumes in September, which would translate into around a 1.5pp contribution to Q3 GDP (SAAR), vs -8.0pp in Q2.

- Finding cues for domestic demand are trickier, but the slowdown in consumer goods imports volumes (running at its slowest pace in 17 months) is perhaps notable from that perspective; real capital goods imports growth have held up a little better.

- The BOC's July MPR estimate for Q3 GDP was 1.0% Q/Q SAAR; that included a continued dropoff in non-commodity exports in the quarter alongside weaker imports in H2.

US TSYS: Late SOFR/Treasury Option Roundup: Low Delta Call Pick-Up

Option desks reported mixed flows on net Wednesday, pick-up in call interest following better low delta put interest early in the session. Underlying Tsy futures mixed, curves twisting flatter after the Sep FOMC minutes spurred renewed selling. Projected rate cut pricing has cooled vs. early morning levels (*): Oct'25 at -23.1bp (-23.7bp), Dec'25 at -44.6bp (-45.1bp), Jan'26 at -54.6bp (-55.2bp), Mar'26 at -64.5bp (-66.5bp).

- SOFR Options:

- 2,750 SFRZ5 96.43/96.50/96.56 call flys

- 4,000 SFRZ5 96.00/96.06/96.12/96.18 put condors

- +10,000 SFRZ5 96.62/96.68 call spds, cab vs. 96.295/0.05%

- Block/pit, +50,000 SFRG6 97.25/97.50 call spds, 1.0 ref 96.52

- +2,000 SFRZ5 96.43/96.50 call spds, 0.75 vs. 96.315/0.08%

- +25,000 0QX5 97.37 calls, 1.5 vs. 96.875/0.05%

- 2,500 2QM6 97.62 calls, 4.0 vs. 96.74/0.12%

- 4,000 0QM6 96.00/96.50 put spds WITH 2QM6 95.87/96.37 put spds, 16.5 total

- +2,000 SFRZ5 96.00 puts, 0.5 ref 96.325

- 3,000 0QH6 97.06/97.18 call spds vs 3QH6 96.75/97.00 call spds on 2x1 basis

- +4,500 SFRZ6 96.12/96.50/96.75 broken put flys, 2.0 ref 96.94

- Treasury Options:

- 5,000 FVX5 108.5/109.5 strangles, 13.5

- +10,000 TYX5 113.5 calls, 9

- 2,000 TYZ5 113/114 2x3 call spds, 26 net ref 112-22.5

- +7,000 FVF5 110/111.5 call spds 18.5 vs. 109-12.25

- Block, -4,200 TUF6 104.62/105.37 call spds, 7.5 vs. 104-08.62/0.25%

- -7,000 wk2 TY 112 puts, cab-7 ref 112-25.5 (exp 10/10)

- 4,000 wk2 TY 113.25 calls, 2 ref 112-24 (exp 10/10)

- -5,000 TYZ5 111/112 put spds, 16 ref 112-24

- +2,000 USX5 114 puts, 7 ref 116-31