OIL PRODUCTS: Oil Products End of Day Summary: Cracks Rise on Week

Cracks have reversed earlier gains to be down on the day. However, they remain set for significant weekly gains amid disruption at several refineries, squeezing already tight product markets.

- US gasoline crack down 1.1$/bbl at 21.73$/bbl

- US ULSD crack down 0.8$/bbl at 44.51$/bbl

- There is very limited evidence that current refining tightness can be sustainably alleviated, Sparta Commodities said this week.

- Gunvor has withdrawn its offer for Lukoil’s international assets after the US Treasury Department said the oil and gas trader would never get a license.

- CDU capacity utilisation rates at China’s state-owned refineries fell by 1.86%pts in the week to Nov. 7 to average at 78.64%, OilChem said.

- The Naftan oil refinery is operating as normal after a fire earlier this week, a senior manager said cited by Reuters.

- Lukoil’s Volgograd refinery halted one of its crude-processing units until at least Nov. 30 following a Ukrainian drone strike on Thursday, according to Bloomberg citing a source.

- Bulgaria took a step toward taking full control of Lukoil’s Neftochim refinery to ensure it remains in operation after US sanctions come into force, according to Bloomberg.

- Hungary’s sole refiner MOL said it can procure most of its oil from non-Russian oil the company has said via its Q3 results call.

- Indian fuel demand fell 0.4% y/y in October to 20.17m metric tons, according to PPAC data cited by Reuters.

- Ukrainian military intelligence, known as HUR, said its drones hit the Sterlitamak Petrochemical Plant in Russia’s Bashkortostan region, according to a Telegram statement cited by Bloomberg.

- MNI: U.S. Refinery Highlights Q3, 2025: Download Full Report Here

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUDUSD TECHS: Monitoring Support

- RES 4: 0.6763 1.382 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 3: 0.6726 1.236 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 2: 0.6660/6707 High Sep 18 / 17 and key resistance

- RES 1: 0.6629 High Sep 30 & Oct 01

- PRICE: 0.6586 @ 16.30 BST Oct 8

- SUP 1: 0.6527/21 61.8% of the Aug 21 - Sep 17 bull leg / Low Sep 26

- SUP 2: 0.6484 76.4% retracement of the Aug 21 - Sep 17 bull leg

- SUP 3: 0.6463/6415 Low Aug 27 / Low Aug 21 / 22 and a bear trigger

- SUP 4: 0.6373 Low Jun 23

The AUDUSD uptrend remains intact and the latest pullback is considered corrective. The pair has again pierced support at the 50-day EMA, at 0.6563. A clear break of this average would signal scope for a deeper retracement and expose 0.6527 once again, a Fibonacci retracement. For bulls, a reversal higher would refocus attention on 0.6707, the Sep 17 high. Initial resistance to watch is 0.6629, the Sep 30 and Oct 1 high.

US TSYS: Tsys Hold Near Post-Sep FOMC Lows, Projected Cuts Cool Slightly

- US Treasuries see-sawed off early session highs, looking to finish near lows after the September FOMC minutes release, curves twist flatter with the short end underperforming. TYZ5 currently -2 at 112-19.5 vs. 112-17 low.

- Standout headline out of the September FOMC minutes release is that "most" participants "judged that it likely would be appropriate to ease policy further over the remainder of this year". But this isn't a surprise when looking at the Dot Plot that emerged from the meeting that showed 12 of 19 members eyeing at least one further cut.

- Projected rate cut pricing has cooled vs. early morning levels (*): Oct'25 at -23.1bp (-23.7bp), Dec'25 at -44.6bp (-45.1bp), Jan'26 at -54.6bp (-55.2bp), Mar'26 at -64.5bp (-66.5bp).

- Treasury futures gradually retreated after the $39B 10Y note auction re-open (91282CNT4) tailed earlier: drawing 4.117% high yield vs. 4.112% WI; 2.45x bid-to-cover vs. 2.65x prior.

- There was no breakthrough in the gov't shutdown today - both of the Senate votes have now failed. Either bill needed 60 votes: the Republican funding bill vote was 54 yes/45 no, while the Democratic package was defeated 47-52. This means that no members changed their votes vs prior. There's a chance we get another set of votes Thursday.

- The dollar index added to recent gains, putting the greenback to its highest levels since early August - contrasting with more fragile, political risk-tripped, trade in the EUR and JPY.

- Thursday's weekly Jobless Claims and Wholesale Trade Sales/Inventories suspended due to the Gov shutdown.

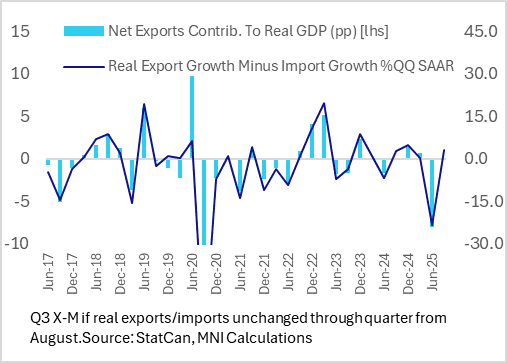

CANADA DATA: Trade Continues To Looks Marginally Positive For Q3 GDP

The sharp (~3% M/M) drop in export volumes in August reported Wednesday saw the 3M/3M annualized rate of growth remain very negative, at -9.3%. While that's an improvement from the -31% in June - driven by the US-Canada trade war - it's still a sharper contraction seen than the 5.2% 3M/3M drop in import volumes in August.

- As long as import volume growth exceeds that of export growth in September by at most 3pp, however, we estimate net exports will contribute positively to growth in the 3rd quarter. That would be the case with a flat increase in both import and export volumes in September, which would translate into around a 1.5pp contribution to Q3 GDP (SAAR), vs -8.0pp in Q2.

- Finding cues for domestic demand are trickier, but the slowdown in consumer goods imports volumes (running at its slowest pace in 17 months) is perhaps notable from that perspective; real capital goods imports growth have held up a little better.

- The BOC's July MPR estimate for Q3 GDP was 1.0% Q/Q SAAR; that included a continued dropoff in non-commodity exports in the quarter alongside weaker imports in H2.