OIL: Oil End of Day Summary: WTI Below $60/b

WTI has dropped below $60/b, coming under renewed pressure after Trump threatens more extensive tariffs against China. This compounds an easing geopolitical risk premium and oversupply concerns.

- WTI NOV 25 down 4.4% at 58.83$/bbl

- Baker Hughes Rig Count: Oil: 418 (-4) - down 63 rigs, or 13.1% on the year.

- President Trump threatened to raise tariffs on China, citing a letter from Beijing which he claims lays out new rare earth export control measures.

- The Gaza agreement reduces geopolitical risk in the key oil-exporting Middle East after prices had risen earlier in the week following a more cautious OPEC November output increase.

- The NYT reported that Venezuela offered the US various concessions including stakes in its oil resources to avoid military conflict, before diplomatic efforts broke down earlier this week.

- Saudi Aramco is set to sell ~39-40mbbl of contractual supplies of November loading crude to China, compared to 50-51mbbl a month ago, Bloomberg said.

- Shipments of Urals, Siberian Light and KEBCO grades from Primorsk, Ust-Luga and Novorossiysk may drop 200k b/d on the month to 2.3m b/d: Reuters.

- Oil could recover to $70/bbl by the end of 2026, underpinned by rising demand or OPEC supporting the market with production cuts, ANZ said.

- Global crude and condensate exports reached near-peak levels of over 45mb/d in September, Vortexa said.

- Analysts warn that the global oil market is becoming complacent about price risks, as limited spare production capacity leaves it vulnerable to geopolitical disruptions, Platts reported.

- Concerns of a looming supply glut are set to exert additional pressure on crude prices, according to DNB Carnegie

- Canadian PM Mark Carney has suggested that reviving the long-stalled Keystone XL oil pipeline from Alberta to the United States could strengthen US-Canadian energy cooperation: Reuters

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

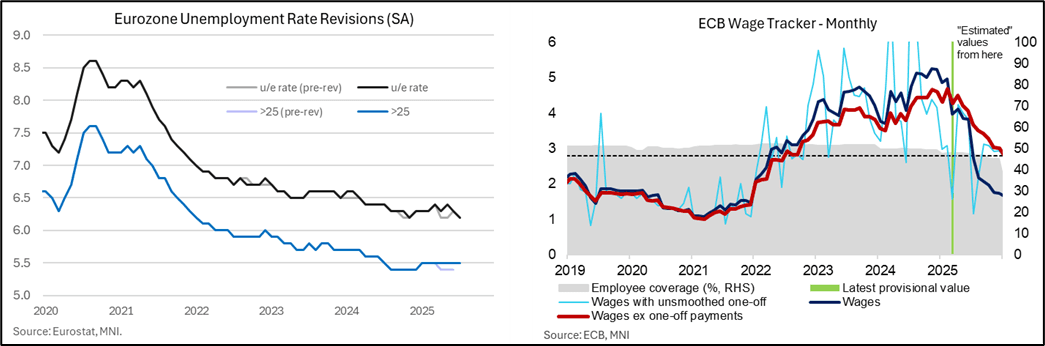

ECB: Macro Since Last ECB: Labour - U/E Rate At Series Lows After More Revisions

- The Eurozone unemployment rate printed at 6.2% in July as expected, a joint series low, but revisions have again altered recent trends. The data have quite often been revised and June saw a fairly typical 0.1pp upward revision to 6.3%, although the +0.2pp to 6.4% in May was more surprising.

- It leaves a trend of recent improvement but with question marks over the data. What had been seen as three months at joint cycle lows of 6.2% through Apr-Jun, tying with 6.2% in Oct-Nov 2024, Eurostat now estimate a latest pattern of 6.3% in Apr, 6.4% in May, 6.3% in Jun and 6.2% in July, tying with 6.2% only in Nov 2024.

- ECB’s Lagarde has pointed to these at-the-time historically low unemployment rates when citing the health of the labour market in recent meetings. Outright employment growth remains subdued however, with just 0.1% Q/Q and 0.6% Y/Y in Q2.

- As for inflationary pressures stemming from the labour market, Eurozone unit labour costs grew 3.1% Y/Y in Q2, down from 3.3% in Q1 for the seventh consecutive annual deceleration. This was above the ECB's 2.9% projection made in June, seemingly driven by the smaller-than-expected deceleration in total compensation per employee growth (3.9% Y/Y vs 4.0% prior, 3.4% ECB).

- While a declaration in ULC growth has allowed the ECB to deliver 200bps of easing this cycle, the data is too lagged to help determine whether further fine-tuning of the policy stance is necessary. Given the modest upward surprise to compensation per employee growth, it argues in favour of steady rates at 2.00% for now.

- ULC growth may have moderated at a steadier pace than the ECB forecast but its forward looking wage tracker released earlier in the inter-meeting process points to a continued decline in negotiated wage growth. Now with estimates out to 1Q26, it eyes wage growth excluding one-off payments at 2.6% Y/Y in 1Q26 after 3.1% in 4Q25. Overall, the results are consistent with a further softening in services inflation pressures in the coming years, in line with ECB signalling.

EURGBP TECHS: Corrective Pullback

- RES 4: 0.8769 High Jul 28 and the bull trigger

- RES 3: 0.8744 High Aug 7

- RES 2: 0.8728 76.4% retracement of the Jul 28 - Aug 14 bear leg

- RES 1: 0.8713 High Sep 2

- PRICE: 0.8653 @ 16:30 BST Sep 10

- SUP 1: 0.8636/8597 50-day EMA / Low Aug 14 and the bear trigger

- SUP 2: 0.8562 50.0% retracement May 29 - Jul 28 upleg

- SUP 3: 0.8540 Low Jun 30

- SUP 4: 0.8514 61.8% retracement May 29 - Jul 28 upleg

EURGBP traded lower Tuesday and has breached the 20-day EMA. Short-term weakness is considered corrective - for now - and support to watch lies at 0.8597, the Aug 14 low. Clearance of this level would reinstate a recent bearish threat. A resumption of gains would open 0.8744, the Aug 7 high. Key resistance and the bull trigger is at 0.8769, the Jul 28 high. Note that MA studies are in a bull-mode position highlighting a dominant uptrend.

BONDS: EGBs-GILTS CASH CLOSE: Short-End Underperformance Ahead Of ECB

EGBs and Gilts traded in mixed fashion Wednesday, with underperformance at the short end of respective curves.

- While Gilt yields remained within this week's ranges throughout the day, 10Y Bund yields touched an intraday post-Aug 7 low in early trade as markets digested overnight news of Poland downing Russian drones in its territory.

- Lower-than-expected inflationary pressures in the US producer price report saw a brief rally across global core instruments, but EGBs and Gilts were content to drift into the cash close ahead of event risk Thursday.

- The German curve twist flattened on the day, with the UK's bear flattening.

- OAT spreads were little changed albeit underperformed periphery/semi-core EGBs more widely, following overnight news that French President Macron had named centrist/ex-defence minister Lecornu as the new Prime Minister.

- While US CPI will garner significant attention, Thursday's European highlight is the ECB decision (MNI preview here in PDF).

- Along with the expected rate-hold along with communications reiterating a data dependent approach, Lagarde's characterisation of economic resilience and/or the extent to which uncertainty has been alleviated by the US-EU trade deal should help shape market reaction.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.1bps at 1.952%, 5-Yr is unchanged at 2.225%, 10-Yr is down 0.7bps at 2.652%, and 30-Yr is down 0.7bps at 3.273%.

- UK: The 2-Yr yield is up 2.6bps at 3.94%, 5-Yr is up 1.8bps at 4.055%, 10-Yr is up 1bps at 4.633%, and 30-Yr is up 0.5bps at 5.482%.

- Italian BTP spread down 0.6bps at 81.5bps / French OAT spread down 0.3bps at 80.9bps