OIL: Oil End of Day Summary: Crude Rises

Crude prices edge higher after the pull back from a high on Jan. 14. The market is weighing geopolit...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

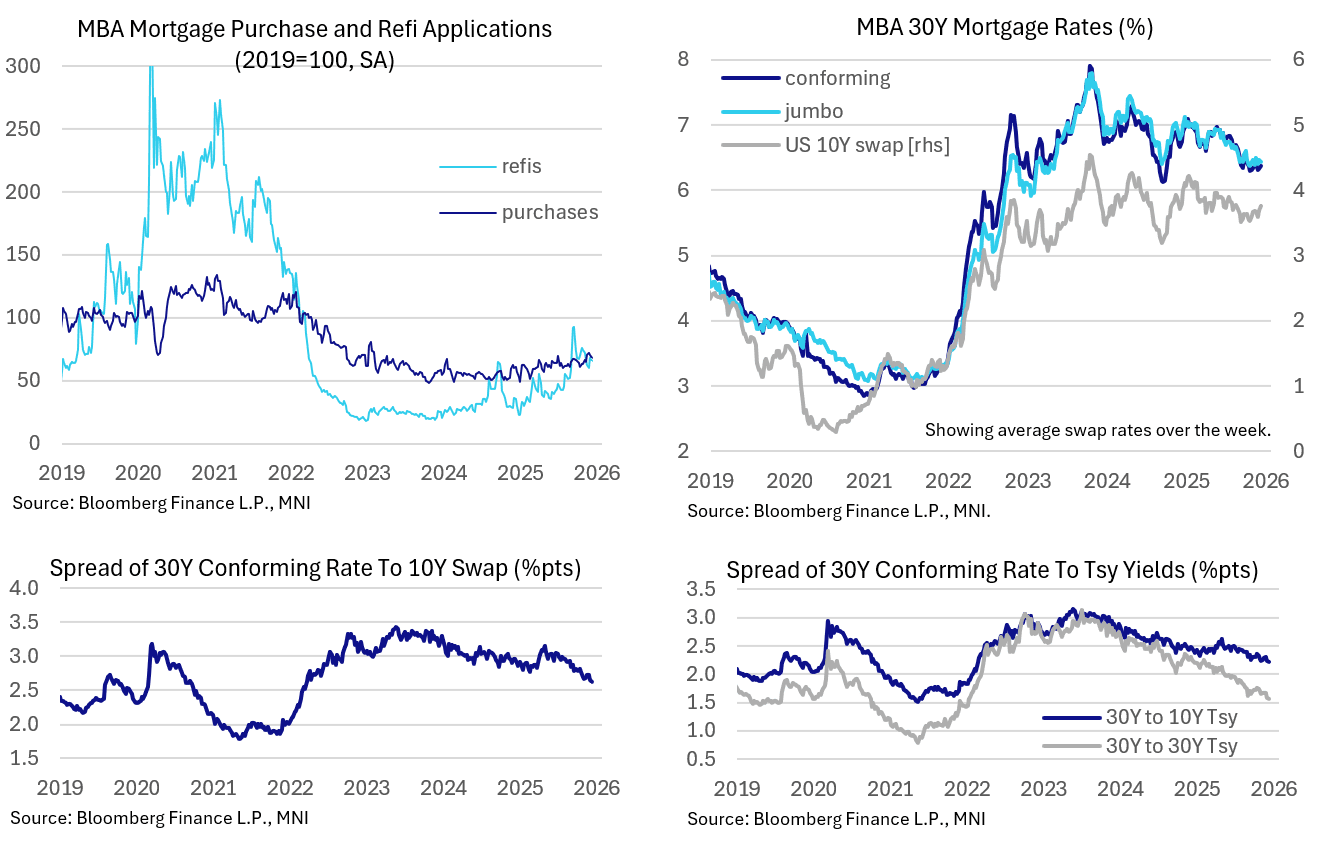

US DATA: Mortgage Spreads Continue To Narrow, But MBA Activity Stays Weak

MBA mortgage application activity softened slightly in the latest week, but the more notable trend in recent weeks has been a continued narrowing of mortgage rate spreads.

- The MBA composite fell 3.8% W/W in the week of Dec 12, partially reversing the 4.8% rise the previous week but keeping activity at the overall subdued levels seen since late 2023 (at 1/3 below pre-pandemic levels). Purchase applications fell 2.8% for a 2nd consecutive fall, while refinancing apps pulled back 3.6% after soaring 14.3% the prior week.

- This pullback came as 30Y conforming mortgage rates ticked up, by 5bp to 6.38% for a 3-week high; Jumbo rates dipped 2bp after a 6bp rise the prior week.

- But this was due to a rise in underlying rates. 10Y Treasury yields averaged 7bp higher than the prior week (4.17% after 4.09%) with 30Y up 6bp (4.81% after 4.75%), with 10Y swaps up 8bp (3.76% after 3.68%).

- As such, mortgage spreads continued to fall. Conforming 30Y mortgage spreads to 10Y fell to 221bp and to 30Y to 157bp with spreads to 10Y swaps at 261bp, all the lowest since early 2022.

EURGBP TECHS: Remains Above Support

- RES 4: 0.8865 High Nov 14 and a bull trigger

- RES 3: 0.8840 High Nov 20

- RES 2: 0.8818 High Nov 26

- RES 1: 0.8802 High Dec 2 and a key near-term resistance

- PRICE: 0.8775 @ 16:31 GMT Dec 17

- SUP 1: 0.8721 Low Dec 9

- SUP 2: 0.8706 76.4% retracement of the Oct 8 - Nov 14 bull leg

- SUP 3: 0.8670 Low Oct 21

- SUP 4: 0.8656 Low Oct 8 and a key support

The bull cycle in EURGBP that started on Dec 9 highlights a possible reversal of the corrective phase between Nov 14 - Dec 9. Key short-term support has been defined at 0.8721, the Dec 9 low. A break of this level would signal scope for a deeper retracement, towards 0.8706, a Fibonacci retracement. Initial firm resistance to watch is unchanged at 0.8802, the Dec 2 high. Clearance of this hurdle would be a bullish development.

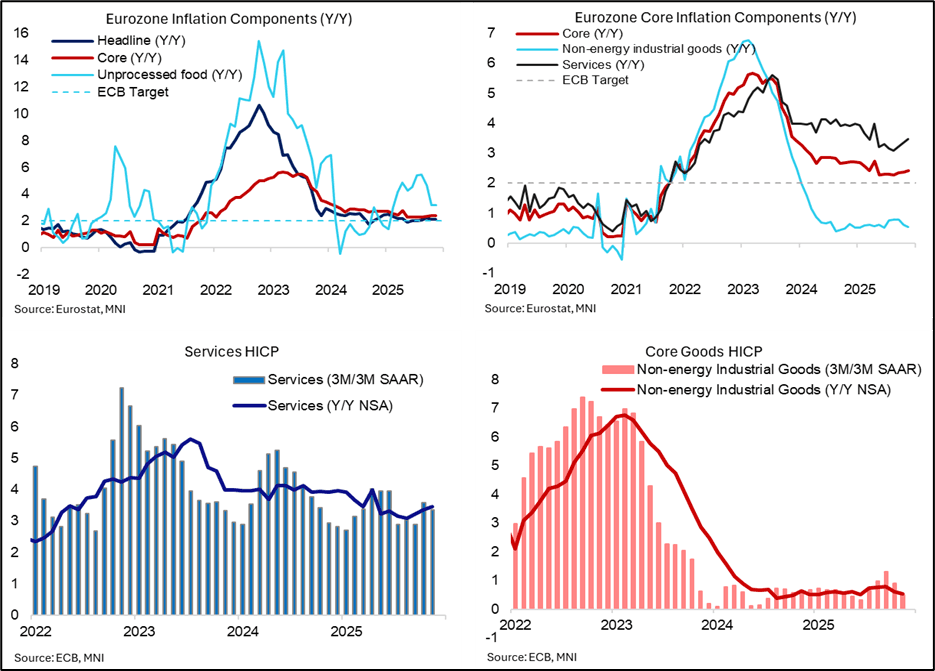

ECB: Macro Since Last ECB - Inflation: Firmer Services Helped By Package Hols

- The ECB has received a reasonable amount of new information on HICP inflation since its last meeting although it’s unlikely to have materially altered its outlook.

- Headline HICP inflation has modestly cooled since September (from 2.24% Y/Y to 2.10% in Oct and 2.14% in today’s final November data) whilst core has firmed slightly (from 2.35% to 2.37% in Oct and 2.41% in Nov). Headline was trimmed very slightly from 2.16% in the flash release whilst core was completely unchanged at 2.41%.

- Further within the details, services inflation accelerated to 3.47% Y/Y in November from 3.24% in September for its fastest since April, a little higher than consensus but mostly outweighed by core goods inflation undershooting at 0.55% Y/Y.

- The final November report confirmed as generally expected that package holidays had played a role in the further services acceleration, jumping from 0.91% to 4.42% Y/Y in November. Other travel-related categories were more mixed, with accommodation firming from 3.14% to 3.41% but airfares swinging from 1.66% in Oct to -2.74% in Nov (national level data were unclear on the extent to which this reversed).

- As for more recent 3M/3M trend rates, core inflation momentum was 2.35% annualised in November, a pullback from 2.62% in October to leave it unchanged from the 2.35% the ECB had seen for September ahead of the last meeting (a figure that currently shows as 2.31% in the latest vintage). Services momentum has firmed on net though, at 3.36% in Nov after 3.59% in Oct and 2.89% in Sept.