COMMODITIES: Oil Down on Supply Concerns; Gold Rises on Rate Hopes

- WTI fell below $58 bbl overnight as supply concerns continue to challenge forecasts for next year. WTI declined -1.79% to US$57.90bbl and is on track for one of the biggest weekly falls in over a month.

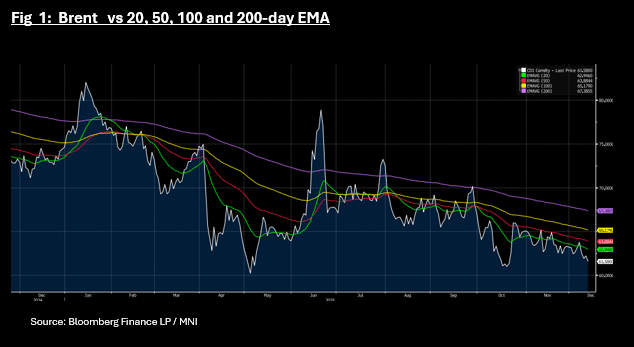

- Brent is down -1.4% to US$61.62, its lowest since October. At current levels, Brent is below all major moving averages. Topside resistance is the 20-day EMA at US$62.94

- OPEC+ forecasts are now at odds with industry forecasts following the release of their latest projections. OPEC+ points to a balanced supply demand outlook whereas industry forecasts suggest a supply excess next year with one of the leading oil trading houses describing it as a 'super glut'. OPEC+ is known to be too optimistic in its forecasts missing year end estimates over the last two years. OPEC+ has agreed to pause further output increases during Q1 next year following increases in 2025.

- Brazilian oil output is coming back on line from issues that took out over 300,000 barrels a day last month, increasing the probability of an oversupply in 2026.

- Recent attacks by Ukraine on one of the primary export terminals for Kazakh oil has limited output by an estimated 250k barrels per day

- Ukraine attacked Lukoil's Caspian seal oil field with long range drones halting output for more than 20 wells at the offshore field.

- The seizure of the Venezuelan oil tanker by US military could be the start of a meaningful drop in oil exports from the sanctioned country with independent research firm Rapidan Energy Group suggesting up to 30% of Venezuela's oil exports are now at risk. (per BBG)

- Gold continues to perform following the less than hawkish FED outcome with bullion up for a third day and on track for a weekly gain.

- Gold is up +1.2% in US trading, touching US$4,280.15

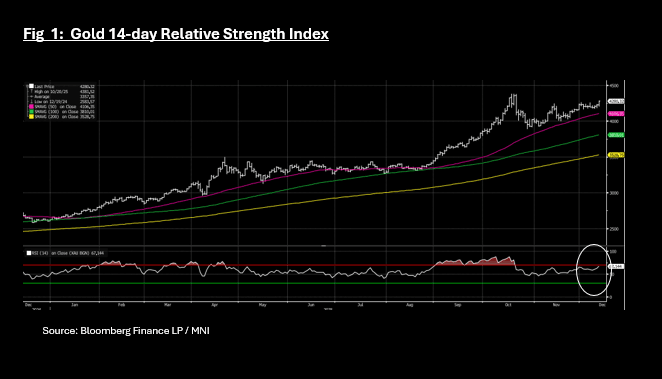

- The rally in recent days sees XAU nearing overbought on the 14-day relative strength index for the first time since mid-October. Gold spent much of September and October overbought as new highs of US$4,356.30 were hit.

- Following those highs gold corrected almost 10% by October end on hopes that the trade war was ending. Gold now sits just 1.7% below the October high as ongoing signs of Central Bank buying supports prices.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CNH: Lags Softer Dollar Backdrop, USD/CNH Risks Still Biased Lower

USD/CNH once again couldn't sustain sub 7.1200 levels, despite a softer USD backdrop as Tuesday trade unfolded (we were last 7.1220/25). The BBDXY index and DXY indices lost around 0.10%, as softer jobs data from the new weekly ADP release weighed. CNH was close to unchanged for Tuesday's session, while the broader technical backdrop remains the same. Expect moves up into the 7.1300/1400 region to draw selling interest, while downside targets are likely to focus on 7.1000 from a medium term standpoint.

- Spot USD/CNY finished up at 7.1173, while the CNY CFETS basket tracker edged down a little further to 97.87, consistent with softer USD index levels.

- The CNH/JPY cross was relatively steady, we track near 21.6470 in early Wednesday trade, with USD/JPY unable to test above 154.50 as softer US data weighed. This leaves recent highs in CNH/JPY intact, just above 21.70.

- For USD/CNH, downside risks will still likely emerge as the bias around US-CH 2yr yield differentials is still skewed lower over the medium term.

- The PBoC did state late yesterday, it will implement a moderately loose monetary policy, utilise various tools to maintain relatively loose social financing conditions, according to the Q3 monetary report released Tuesday. On FX, the report said it will maintain exchange rate flexibility, strengthen expectation guidance, prevent the risk of overshooting, and keep the yuan basically stable at a reasonable and balanced level. This is no change in the FX stance.

- On the data front, we still await Oct new loans and aggregate financing data. The PBoC also stated that slowing loan growth is not cause for concern as the economy shifts from high speed to high quality growth.

BONDS: Slightly Richer With US Tsy Futures

NZGBs are flat to 2bps richer, with the 5-year benchmark leading.

- US tsy futures holding firmer. Currently, the Dec'25 10Y contract finished trading +10 at 113-00 vs. 113-01.5 high - just below resistance at 113-02, the Nov 5 and 7 high. Clearance of this level would highlight a potential bullish reversal – MNI Tech

- Otherwise, a short-term bear theme in US tsy futures remains in place. Attention is on a reversal trigger at 112-06, the Sep 25 low, and the 100-DMA, at 112-08. A clear break of these price points would expose a trendline support at 112-02.

- Bloomberg reports that, "First-Time Buyers Snap Up New Zealand Property After Price Slide. People signing up to buy their first property in New Zealand made up a record 27.7% of all transactions in the third quarter, according to the Cotality-Westpac NZ First Home Buyer Report."

- Swap rates are 2bps lower.

- RBNZ dated OIS pricing is little changed across meetings. 28bps of easing is priced for November, with a cumulative 38bps by February 2026.

- Today, the local calendar will be empty ahead of Card Spending data tomorrow.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 4.50% May-30 bond, NZ$150mn of the 4.25% May-34 bond and NZ$50mn of the 5.00% May-54 bond.

OIL: Crude Rallies As Market Watches Rise In Product Prices

Oil rallied on Tuesday as the impact on global supplies from sanctions on Russia came to the fore again after US President Trump said that a US-India trade deal was close. Also, demand for products remains robust, as seen in US inventory data, and the announcement of restrictions on Russia’s Rosneft and Lukoil drove prices sharply higher. Short-covering also supported oil benchmarks on Tuesday.

- WTI rose 1.5% to $61.04/bbl after reaching $61.28, below initial resistance at $62.59, 24 October high. It fell to $59.66 but has struggled to hold moves below $60, which provided support to the benchmark from a technical perspective. Support lies at $58.83, 6 November low.

- Brent was up 1.7% to $65.13/bbl after a peak of $65.31 to be slightly higher in November. It approached resistance at $65.98, 9 October high. Initial support is a $62.84, 6 November low.

- With product prices surging, attention will be on Wednesday’s US industry inventory data. The official EIA release will be Thursday.

- India is the second largest importer of Russian oil and if it looks to other sources there could be a large quantity of Russian crude unconsumed.

- The excess oil supply driven by increased OPEC and non-OPEC output remains in focus with the spread between the WTI December-January contracts only 6c. The EIA short-term outlook, IEA annual report and OPEC monthly report are published Wednesday.