OIL: Oil Consolidates Gains Following US Sanctions News.

- As President Biden approaches the end of his term, it appears that one of his last actions may be targeted at Russian oil.

- It is believed that Biden’s team are looking at further restrictions to impact the flow of Russian oil, a move that the President has avoided in the past for fear of a spike in energy costs.

- However, with the current OPEC+ oversupply issues, the market seems able to withstand possible sanctions should they come to pass.

- Prices did rise on the news with WTI steadily rising throughout the US trading day to break through the US$70/bl mark, closing at $70.29 where it has stayed at all day in Asian trading.

- Brent maintained a positive bias throughout the US trading day also reaching a high just prior to US close of US$73.75, before closing at $73.52. It rose marginally through the Asian trading day to $73.59.

- OPEC+ released its forecasts for the full year 2024 and projections for next year for oil demand, with both seeing major downward revisions.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

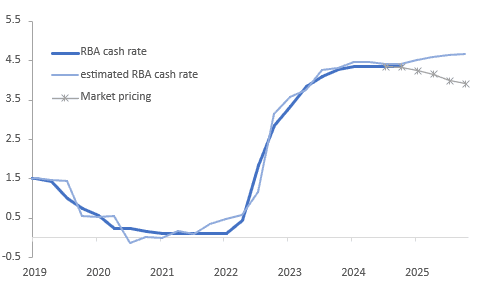

AUSTRALIA: Positive Core Inflation Gap Implies Too Early For Rate Cuts

With temporary state and federal government electricity rebates for households impacting headline inflation, the RBA has said that “underlying inflation is more indicative of inflation momentum”, even though officially its focus is headline as Governor Bullock reiterated before the Senate economics committee last week. Thus we have re-estimated our Australian OCR policy reaction function using quarterly trimmed mean CPI.

- We have also updated it for the revised RBA staff forecasts published in the November Statement of Monetary Policy. There were slight downward revisions to the trimmed mean CPI profile, while GDP growth was revised down.

- Our equation uses the trimmed mean inflation gap with the target band mid-point of 2.5% and the GDP output gap with a current trend growth estimate at around 2.25%. It is worth noting that econometric calculations are only estimates and not predictions.

- The equation with core inflation points to rates needing to stay roughly where they are to be consistent with economic fundamentals and their outlook. If anything it is implying another 25bp of tightening by end-2025 with around a 25% chance of a hike each quarter. In contrast market pricing has around 50bp of easing priced in by Q4 2025.

- The model is also “cautious” not signalling the need for any easing as there is a positive inflation gap until end-2026, when it closes but is still yet to turn negative. The equation is forward looking using the one quarter lead of the core inflation gap.

Australia OCR policy reaction function with trimmed mean CPI %

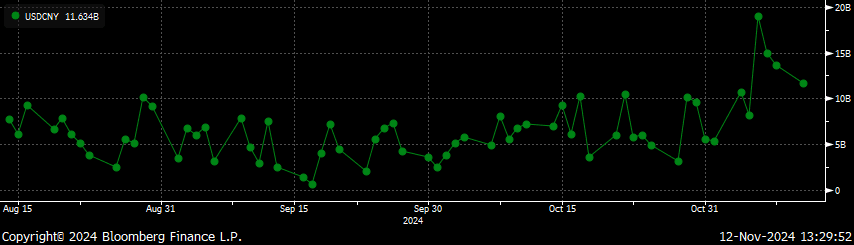

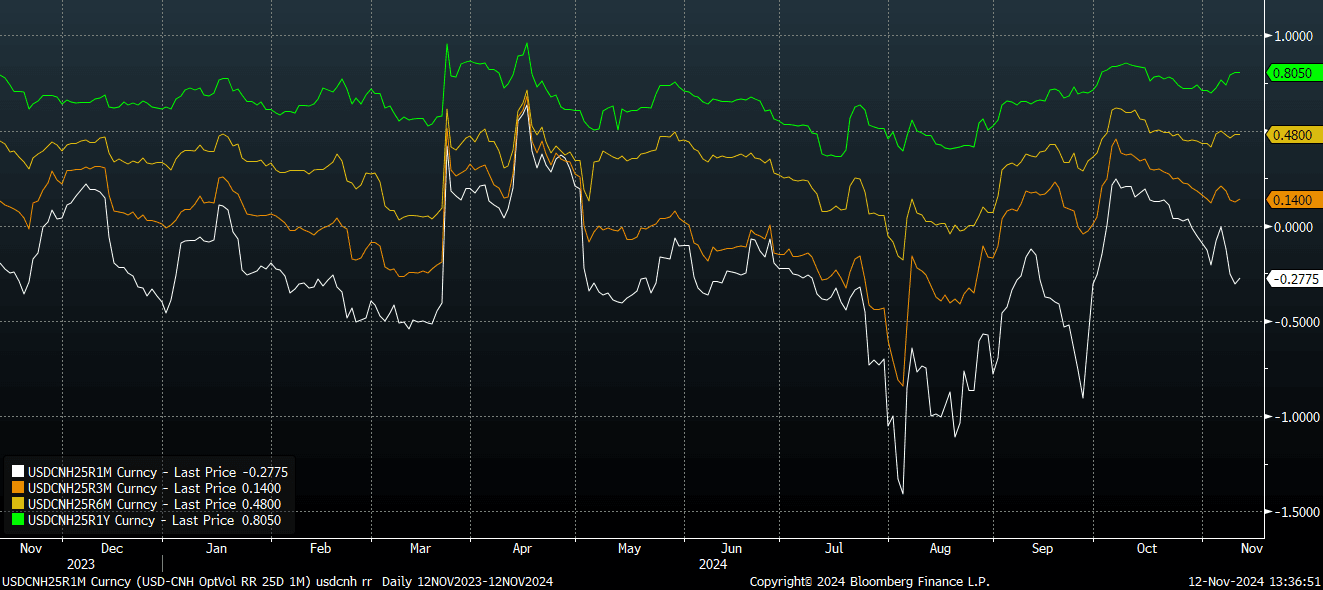

CNH: CNY FX Option Volumes Elevated, USD/CNH 12mth RR Close To Cycle Highs

USD/CNH is steady around the 7.2400 level in latest dealings. Earlier highs were at 7.2454, levels last seen in early August. Spot USD/CNY has gravitated higher as well, but found some selling resistance above 7.2300. The earlier BBG report on potential lower taxes to aid property sentiment hasn't had a lasting positive impact on equity sentiment, with headline indices back to around flat or slightly weaker. Hong Kong's HSI is down over 1%.

- In the FX option space, CNY volumes are dominating Tuesday trade so far. The chart below shows the trend shift higher in USD/CNY volumes since the US election, per DTCC (BBG). Today CNY has accounted for around 31% of total volumes, followed by JPY with 17%.

- For USD/CNH risk reversals, we have a positive skew the longer the tenor. The second chart shows USD/CNH risks reversals for the 1 month, 3 month, 6 month and 12 month tenors. This is typically always the case, although trends have diverged somewhat in the past week, with the 1 month RR tracking lower, while the 12 month is close to cycle highs.

Fig 1: USDCNY Options Volumes, Firmer Since Early Nov

Source: MNI - Market News/Bloomberg

Fig 2: USD/CNH Risk Reversals

Source: MNI - Market News/Bloomberg

BONDS: NZGBS: Closed Cheaper, H/H Spending Up Again

NZGBs closed 1-3bps cheaper across benchmarks, aligning with cash US tsys, which are also flat to 3bps cheaper in the Asia-Pac session today with a flattening bias. US tsys reopened today after being closed for the Veterans Day holiday yesterday.

- NZ retail card spending posted a third consecutive monthly rise in October up 0.6% m/m after 0.1%. Total spending rose 0.4% m/m after 0.3% and is now slightly positive on a year ago. The start of easing in August appears to have allowed households to begin to spend again.

- Westpac sees the October data as “encouraging” and that there should be further rises once past and future rate cuts are fully felt. Westpac observes that “most mortgages have not come up for refixing yet. In addition, further cuts from the RBNZ are expected over the coming months (we’re forecasting another 50bp cut at the upcoming November meeting).”

- Swap rates closed 1-3bps higher, with a flattening bias.

- RBNZ dated OIS pricing closed 3-8bps firmer across 2025 meetings. A cumulative 89bps of easing is priced by February, with 52bps by year-end.

- Tomorrow, the local calendar will see Net Migration data, ahead of REINZ House Sales and Food Prices on Thursday.