SWITZERLAND DATA: October KOF Stronger But Should Keep SNB Expectations Intact

Oct-30 08:03

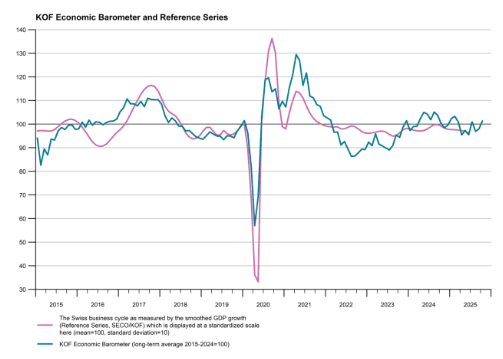

The Swiss KOF indicator outperformed against expectations in October, coming in at 101.3 (98.4 cons; 98.0 September). "The outlook for the Swiss

economy is improving", KOF institute comments.

- On drivers: "Most of the indicator bundles included in the KOF Economic Barometer evince these positive developments. In particular, the indicator bundles for manufacturing, for financial and insurance services, and for other services show a more favourable outlook. The indicators for private consumption, however, experience a setback."

- Despite the upward surprise, the print should not challenge current SNB market pricing, sitting around 9bps of easing priced through the September 2026 meeting.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: BAVARIA SEP CPI +0.4% M/M, +2.4% Y/Y

Sep-30 08:00

- MNI: BAVARIA SEP CPI +0.4% M/M, +2.4% Y/Y

MNI: GERMANY SEP UE RATE (SA) 6.3% (FCST 6.3%); AUG 6.3 %

Sep-30 07:55

- MNI: GERMANY SEP UE RATE (SA) 6.3% (FCST 6.3%); AUG 6.3 %

- GERMANY SEP UE NET CHANGE (SA) +14K; AUG -7K

- GERMANY SEP UE TOTAL (SA) 2.976 MN; AUG 2.962 MN

GILTS: Off Highs, Consolidating Yesterday's Rally

Sep-30 07:53

Gilts look to global peers for cues, with U.S. government shutdown risk and softer-than-expected French CPI providing an early bid, before a pullback from highs as some resistance levels in wider core global FI markets hold.

- Gilts futures flat at ~90.90 with bulls unable to force a test of first resistance at the Sep 24 high (91.28). That leaves bears in technical control, with first support located at the Sep 26 low (90.26).

- Yields essentially unchanged across the curve, with 2s10s and 5s30s remaining in their steepening trend despite the recent flattening moves.

- Local fiscal risks remain evident, with focus on the November Budget.

- We have outlined Chancellor Reeves’ fiscal options if she chooses to break the government’s election pledges.

- GBP STIRs also little changed on the day, showing less than 5bp of easing through year end.

- We continue to suggest that the market is underpricing the odds of a cut in Q4, but note that such a move would likely require support from Governor Bailey, as well as Deputy Governor’s Ramsden & Breeden (in addition to dovish dissenters Dhingra & Taylor).

- Ramsden maintained his position as the most dovish MPC member that did not vote for a cut in September via his speech yesterday, with Breeden set to speak today. We will also hear from BoE’s Lombardelli & Mann today.

- No reaction to modest revisions in the final update to UK Q2 GDP data.