US PREVIEW: October CPI Data Could Include Key Core Items... Or Not (2/2)

The October data could include several of the major categories that we include in our Core CPI consensus tables: used cars and trucks and new vehicles; airfares; lodging away from home; and various communications and medical prices (for headline CPI, gasoline data could be published).

- At least one analyst (Nomura) speculates that the BLS could estimate rents and OER as well as rent data are collected through the Housing Survey and not the Commodities and Services Price survey.

- Below is MNI's collation of sell-side consensus on individual categories. It expresses the average M/M inflation rate over October / November, either from specific month-by-month estimates, or by halving the 2-month change.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

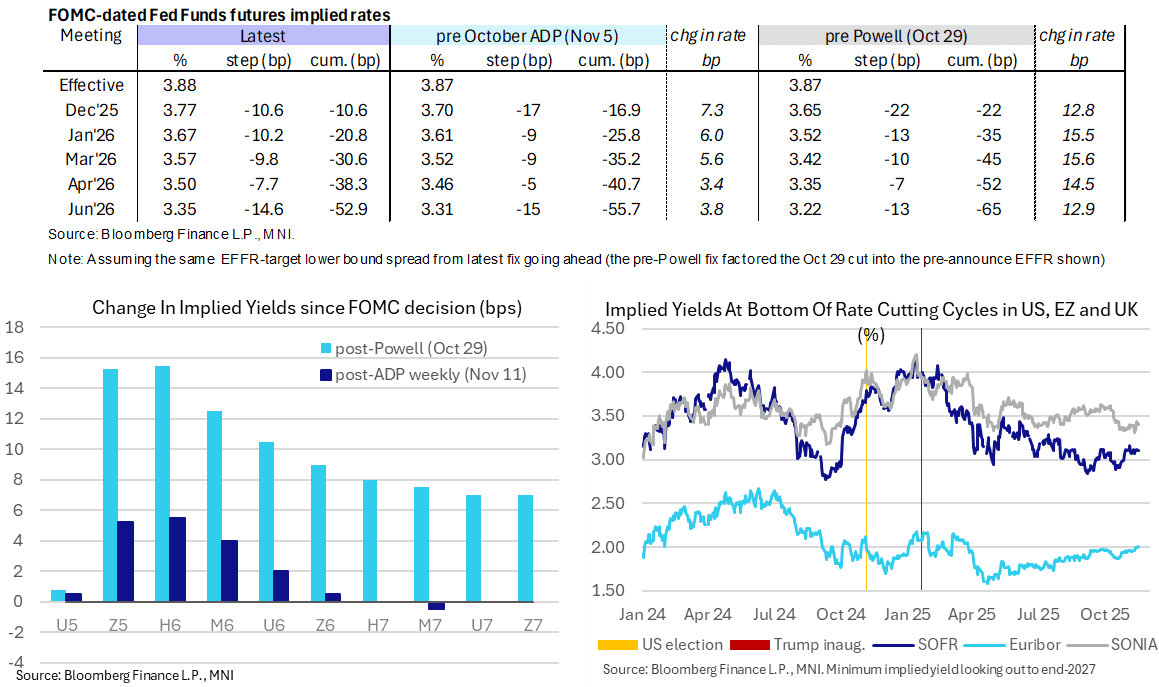

STIR: Fed December Pause Seen As Slightly More Likely, A Dovish Waller Ahead

- US rates at the very front end of the curve have given back some of today's further losses, with SFRZ5 back at 96.175 (-0.01) and the Fed Funds implied rate for the Dec FOMC limited to a 0.5bp increase from Friday’s close.

- The move has come within the past hour with little clear driver, but equally it pares what had been further momentum from last week’s hawkish Fedspeak rather than stronger data earlier.

- It maintains the recent development of a December pause being seen as slightly more likely.

- FF cumulative cuts from an assumed 3.88% effective: 10.5bp Dec, 21bp Jan, 30.5bp Mar, 38.5bp Apr and 53bp Jun.

- SOFR futures are -0.01 (Z5 and H6) to +0.02 (most 2027 contracts), with gains seen from U6 onwards.

- The terminal implied yield at 3.10% (H7) is unchanged since the start of the US session and between the 3.06-3.16% recent range that has been defined primarily by labor data and a strong ISM services report.

- Vice Chair Jefferson earlier today reiterated his increasingly cautious stance, seeing a need to proceed slowly on rates. If forced to guess we would think he is still marginally in favor of a December cut.

- Coming up at 1535ET, Fed Gov. Waller (voter, dove) speaks on the economic outlook (text + Q&A), having driven some gyrations in rates over the past six weeks by sounding a little more patient ahead of the October meeting before reverting to a more dovish stance since then.

- He made clear on Oct 31 that he still supports a rate cut in December and we expect more of the same today. "The fog might tell you to slow down. It doesn't tell you to pull over to the side of the road. You still have to go. You may want to be careful, but it doesn't mean to stop, and … the right thing to do with policy is to continue cutting."

- Tomorrow then sees weekly ADP data at 0815ET for what will be a closely watched update after last week’s abrupt weakness.

EURJPY TECHS: Trend Needle Points North

- RES 4: 181.70 1.764 proj of the Jul 31 - Sep 29 - Oct 2 price swing

- RES 3: 181.01 1.618 proj of the Jul 31 - Sep 29 - Oct 2 price swing

- RES 2: 180.37 1.500 proj of the Jul 31 - Sep 29 - Oct 2 price swing

- RES 1: 180.02 High Nov 14

- PRICE: 179.88 @ 16:15 GMT Nov 17

- SUP 1: 177.72/175.99 20- and 50-day EMA values

- SUP 2: 174.82 Low Oct 17

- SUP 3: 174.30 Bull channel support drawn from the Feb 28 low

- SUP 4: 173.92 Low Oct 6 and a gap high on the daily chart

The trend in EURJPY remains bullish and the cross is holding on to its latest gains. Recent strength has resulted in a break of the bull trigger at 178.82, the Oct 30 high, confirming a resumption of the medium-term uptrend. Note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on 180.37, a Fibonacci projection. First support lies at 177.72, the 20-day EMA.

US STOCKS: Late Equities Roundup: Technology Shares Underperforming

- Major equity indexes are extending late session lows Monday - following a couple of large program sales, one appr 1,470 names - largest since late October. Currently, the DJIA trades down 632.13 points (-1.34%) at 46515.95, S&P E-Minis down 86.5 points (-1.28%) at 6669.5, Nasdaq down 312 points (-1.4%) at 22590.45.

- Chip makers continue to lead late session declines followed by Financial names. Note, Nvidia is expected to release Q3 earnings this Wednesday.

- Dell Technologies -9.57%, Hewlett Packard Enterprise -8.48%, Super Micro Computer -6.89%, Arista Networks -4.14% and Skyworks Solutions -3.99%.

- Coinbase Global -8.59%, Robinhood Markets -7.81%, Capital One Financial -4.61% and Apollo Global Management -4.58%.

- Meanwhile, Health Care and Communication Services sector shares continued to lead late session advances:

- Alphabet +3.01%, Omnicom Group +0.71%, Interpublic Group +0.61% and T-Mobile +0.58%.

- Centene Corp +2.47%, Johnson & Johnson +1.89%, Regeneron Pharmaceuticals +1.83% and Amgen +1.59%.

- Larger names yet to announce earnings this week include: Aramark, Home Depot, Target Corp, Valvoline Inc, Lowe's Cos, Williams-Sonoma, TJX Cos, NVIDIA, Palo Alto Networks, Jacobs Solutions, Bath & Body Works, Walmart, Copart, Gap, Intuit, Ross Stores and BJ's Wholesale Club.