US CREDIT UPDATE: OBDC/OBDC II Merger Called Off: Observations & Relative Value

OBDC/OBDC II Merger Called Off – Some observations and Relative Value

(OBDC:Baa3/BBB-/BBB)

• OBDC today announced it was calling off its proposed merger with OBDC II due to market conditions. Please see our earlier note for more details on the merger: https://www.mnimarkets.com/articles/obdcobdc-ii-blue-owl-capital-merger-terms-further-explained-1763496857057

• The press release cancelling the merger mentions plans to re-evaluate alternatives in the future. OBDC terminated the merger so as to act in the best interest of shareholders given current market conditions. OBDC II shareholders will once again be able to tender shares in Q1’26.

• OBDC shares were trading at 80% of NAV (down 20% YTD) in what is best described as a weak equity market for BDCs. While all BDCs are down YTD, very few were down by a single digit percentage, most were down by more. OBDC, OCINCC and OWL bonds also were quoted wider this week.

• Interestingly, through all the events of the past week, there was no mention of the debt either at OBDC or OBDC II or the operating performance of either. The focus was on shareholders at OBDC II and the public equity valuation of OBDC. Yet OBDC bonds have moved wider by 10-15 bps with a wide print of +240bps on the OBDC 6.2%’30s.

• Interestingly, OBDC (public) bonds continue to trade wide to OCINCC bonds. At +240, the OBDC ‘30s were trading about +20bps wide to the OCINCC $‘30s (as an aside OCINCC €’31s recently were quoted at +252(z)).

• While we would have expected some widening in Blue Owl complex bonds due to the market chatter, we highlight that the relation between the public OBDC to the private OCINCC is inverted.

• That is, when considering comps ARCC/ARESSI, BXSL/BCRED, GBDC/GSCRED and TSLX/SIXSLP, in each case, the public name trades either about flat or 30bps through the private name. We would expect the relationship between OBDC and OCINCC to begin to invert as Blue Owl moves out of the headlines.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

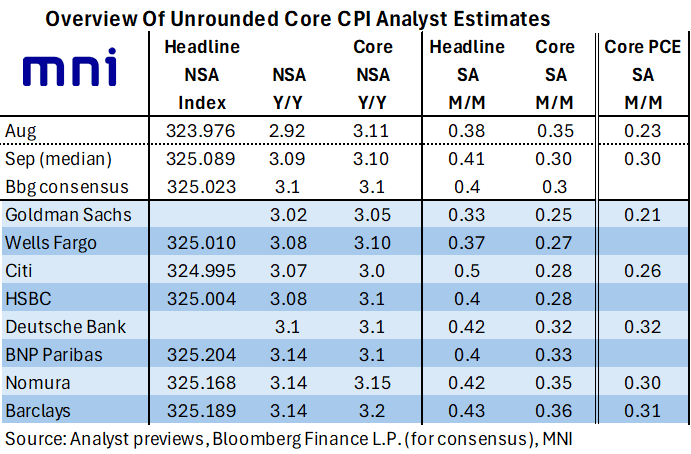

US OUTLOOK/OPINION: Core CPI and Early PCE Estimates Eye 0.30% M/M For Sept

- An early look at analyst unrounded core CPI estimates for Friday’s delayed September release sees a median estimate of 0.30% M/M, with a reasonably wide range of 0.25-0.36% M/M.

- As such, core CPI inflation is mostly expected to moderate from the 0.35% in August although it would be a third consecutive strong month after the 0.32% in July as well.

- Indeed, if accurate, it would leave there having been only two months in the past twelve with a monthly rate equivalent to less than 2% annualized (March and May). That sets it up for a more clearly cut 3.1% Y/Y after accelerating to 3.06% in August.

- Of course, the Fed targets PCE inflation, with a median of the five forecasts for core PCE also at 0.30% M/M for September. In contrast to core CPI, this would be an acceleration after 0.23% M/M in August and 0.24% in July (prior to revisions, which should be more extensive being part of the annual update).

- It's still only seen two months in the past twelve with monthly inflation below 2% annualized (March and November) whilst annual core PCE inflation was still elevated at 2.9% Y/Y in August. The median FOMC member sees this accelerating further to an average 3.1% Y/Y in Q4 before moderating to 2.6% Y/Y in 4Q26 and 2.1% Y/Y in 4Q27.

US TSYS: Late SOFR/Treasury Option Roundup: Mixed Flows

Rather modest SOFR/Treasury option volumes to report Monday, as the US Gov enters shutdown day 19. No data and the Fed in policy blackout. Underlying futures modestly higher (TYZ5 113-19 +4) while US$ index pares modest gains in late trade. Projected rate cut pricing cools slightly vs. late Friday levels (*): Oct'25 at -24.7bp (-25.3bp), Dec'25 at -50bp (-50.9bp), Jan'26 at -63.7bp (-64.8bp), Mar'26 at -77bp (-77.9bp).

- SOFR Options:

- 3,200 SFRM6 96.25/96.62/97.00 vall flys ref 96.87

- 2,000 SFRH6 96.37 puts, 4.0

- over +12,500 SFRZ5 96.12 puts, 0.5 ref 96.365/0.05%

- +2,500 SFRX5 96.75/96.87 call spds, cab

- -4,000 SFRZ5 96.25/96.37 call spds, 8.5

- +2,000 SFRM6 96.25/96.37 put spds, 2.0 ref 96.87

- 1,600 SFRH6 96.31/96.43 put spds

- 1,500 SFRM6 96.25/96.62/97.00 call flys

- +8,000 SFRG6 96.68/96.81/96.87/97.00 call condors, 1.75 ref 96.625 to -.63

- Treasury Options:

- 1,560 USX5 116.5/117/118 broken put flys ref 118-24

- 6,000 TUZ5 104.25 puts, ref 104-13.75

- 9,000 TYZ5 113.5/114.5 call spds, 6 ref

- 10,000 TYZ5 113.5/114.5 2x1 call spds vs. TYZ 112.5 puts

- Update, total -6,000 TYF6 113.5 straddles, 163-200 vs. 113-09 to -13.5/0.06%

- 2,000 TYX5 114/115.5 call spds, 5 ref 113-16

- 2,500 FVF6 110/111.5 call spds ref 1109-27.5

- over 5,000 TYX5 113.5/118 call spds on ratio

- over 5,000 FVX5 109.5 puts, 5.5 last

- 5,900 TYX5 113 puts, 7-8 ref 113-13.5/0.08%

- -5,000 TUZ 104.75 calls, 5 ref 104-13

- +3,000 TYH6 107.5/109 put spds, 6

- 3,000 TYF6 110/112 put spds, 23 vs. 113-11/0.20%

EURJPY TECHS: MA Studies Highlight A Dominant Uptrend

- RES 4: 180.33 Top of a bull channel drawn from the Feb 28 low

- RES 3: 180.00 Psychological round number

- RES 2: 178.94 1.236 proj of the Jul 31 - Sep 29 - Oct 2 price swing

- RES 1: 177.94 High Oct 10 and the bull trigger

- PRICE: 175.52 @ 17:15 BST Oct 20

- SUP 1: 175.19 20-day EMA

- SUP 2: 173.92 Low Oct 6 and a gap high on the daily chart

- SUP 3: 173.24 High Oct 3 and a gap low on the daily chart

- SUP 4: 172.27 Low Oct 2 and a key medium-term support

The trend structure in EURJPY is bullish - moving average studies are in a bull-mode position highlighting a dominant uptrend. Recently, the cross cleared resistance at 175.13, the Sep 29 high to confirm a resumption of the uptrend. A reversal higher would open 175.00, a Fibonacci projection. First key support to watch lies at 175.19, the 20-day EMA - a level pierced on Friday. A clear breach of it would signal scope for a deeper retracement.