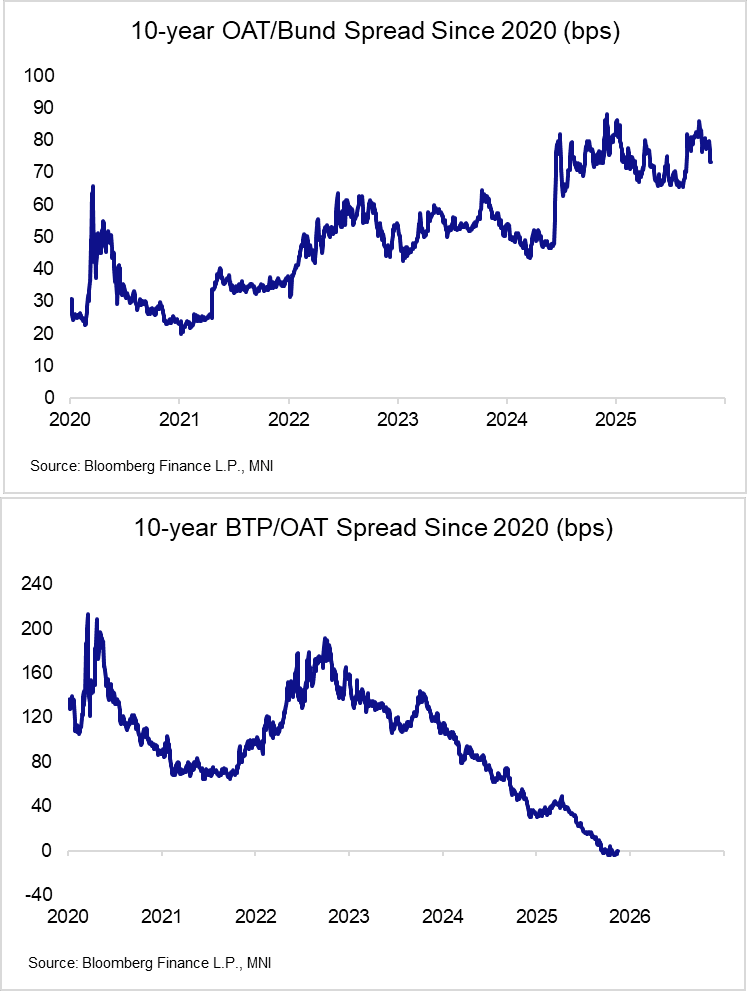

FRANCE: OAT Outperformance Could Stall On Budget Revenue Section Negotiations

The 10-year OAT/Bund spread has narrowed ~7bp since Friday’s close, but a meaningful push through support at 70bp may not be forthcoming unless a clearer path to passing the 2026 budget becomes evident.

- The National Assembly approved the temporary suspension of the 2023 pension reform yesterday, but this was largely as expected. More importantly, lawmakers were unable to vote on the full Social Security bill, and their focus has now turned back to the Revenue section of the budget.

- The majority of yesterday’s OAT/Bund narrowing and BTP/OAT widening came in the morning, seemingly in response to buoyant European equities and improved growth expectations from the Banque de France.

- Increased hopes around France being able to pass a budget will have also factored into OAT outperformance since last Friday (e.g. on the back of optimistic comments from Economy Minister Lescure in recent days). However, this appears more a “no news is good news” dynamic, with the National Assembly still clearly fragmented on many elements of the budget proposals.

- The Social Security bill has now been passed to the Senate and will be reviewed on November 19th.

- A reminder that the National Assembly was unable to vote on the Revenue section of the budget in early November. The Socialist’s Zucman and ‘Zucman light’ proposals were rejected on October 31. Disagreements around how– and whether – to raise revenue from the wealthy are a key risk in the next stage of negotiations. The deadline for passing the revenue section to the Senate is November 23.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILT SYNDICATION: 5.25% Jan-41 gilt: Spread set

- Spread set at 4.375% Jan-40 Gilt + 8.0bps (Guidance was +8/8.5bps)

- Size: GBP Benchmark (MNI expects GBP4.0-8.5bln (probably around the middle to top half of that range).

- Orderbook in excess of GBP125bln (including JLM interest of GBP7bln)

- Maturity: 31 Jan 2041

- Settlement: 15 Oct 2025 (T+1)

- Coupon: 5.25% (short first)

- ISIN: GB00BVP99897

- JLMs: BofA / Barclays / DB / MS (B&D/DM) / RBC CM

- Timing: Books to close at 10:00BST

Source: Market source and MNI colour

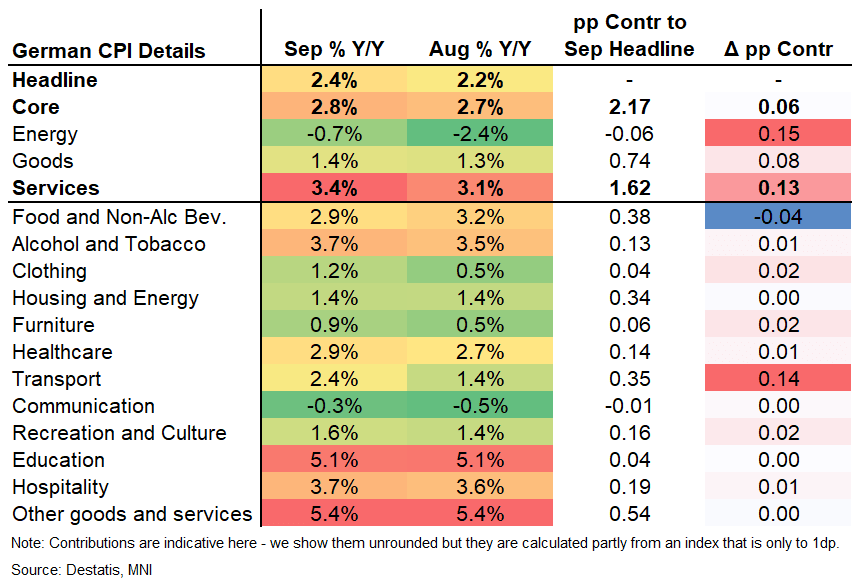

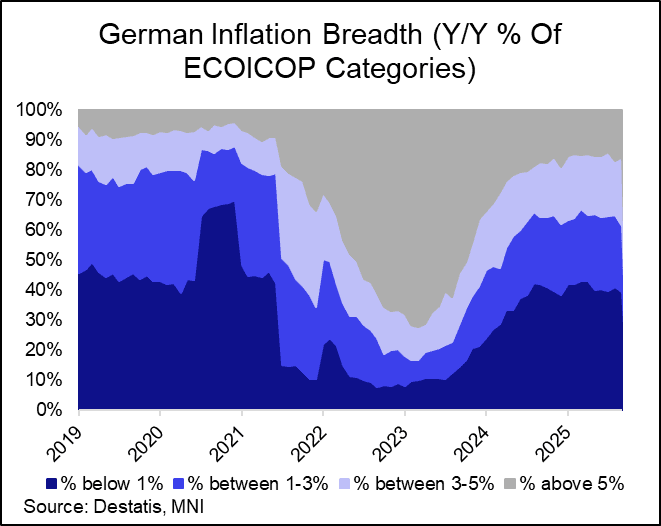

EUROPEAN INFLATION: German September Details See Higher Share At 3-5% [2/2]

MNI’s tracker shows 2-way moves in German September inflation breadth at either end of the spectrum, which broadly cancel out on balance and for the most part reverse the trends seen in August. However, the share running at a still strong 3-5% did rise to its highest in eighteen months:

- Looking at the low-inflation categories, the percentage of ECOICOP items (a standardized category split) printing at or below 1% Y/Y was a little lower at 39% (from 41%) but the percentage in high-inflation categories (above 5%) also decreased from 17% to 16%.

- This meant that the mid-range categories had to offset these moves, with the percentage of items printing between 1% and 5% increasing to 45% from 42% previously.

- However, of note within this broad mid-range category, the share growing between 3-5%, i.e. firmly above that of the 2% target, bounced from 18% to 23% for its highest since Mar 2024.

EUROPEAN INFLATION: Final German September Data Shows Move In Car Fuels [1/2]

German final September HICP was unrevised from the flash readings at 2.4 Y/Y (2.1% in Aug) and 0.2% M/M. The final reading to CPI was also unrevised at 2.4% Y/Y (2.2% in Aug) and 0.2% M/M whilst core CPI printed at 2.8% Y/Y after three consecutive months at 2.7%. The main conclusions from the flash reading were confirmed.

- Services accelerated to 3.4% Y/Y (confirming the flash reading), a 0.3pp reacceleration after two consecutive prints at 3.1%, adding 0.13pp to headline inflation in September. Goods inflation meanwhile also accelerated, with a 0.08pp higher contribution to headline, mostly on the back of higher energy amid base effects.

- As we projected after the state level data ahead of the national-level flash release, the mixed-weighting transport category saw noticeable moves, accelerating to 2.4% (2.5% MNI tracking, 1.4% prior). Out of the 0.14pp the category added to headline in September, 0.13pp came from car fuels (accelerating to 1.1% Y/Y from -2.5% in August amid base effects looking at the -0.4% M/M print), and 0.02pp each from rail and air transport services (outweighed by a negative 0.04pp impact from car prices).

- The remainder of the services acceleration was broad-based across categories: 0.03pp came from package holidays, 0.02pp from lodging away from home, and the remaining 0.04pp are difficult to attribute when rounding contributions to 2dp.

- Food (and non-alcoholic beverages) prices took away 0.04pp from headline in September amid its deceleration to 2.9% Y/Y (from 3.2% prior).

- The Bundesbank thinks German inflation "is likely to be temporarily somewhat higher in the next few months" as energy inflation will turn positive and services are also set to see temporarily higher Y/Y rates again, both amid base effects (August monthly report).

- [See the disclaimer below the table on using the changes in contributions with caution]