EGBS: OAT Futures Extending Higher Following Failed No-Confidence Votes

OAT futures have continued to extend higher, after PM Lecornu survived two censure votes this morning and moved to pass the expenditure section of the 2026 state budget using Article 49.3. Although the outcome of the votes was as expected, it confirms another reduction in near-term political uncertainty.

- OATs are now +38 ticks at 121.51, testing resistance at the 76.4% retracement of the November 26 – December 22 bear leg. Clearance of this level would expose the December 1 high at 121.82.

- OATs are dragging Bund and BTP futures higher, though French bonds unsurprisingly remain the outperformer.

- In cash. The 10-year OAT/Bund spread is now 4bps narrower on the session at 58.5bps. We noted earlier that some may look towards the 57bps level, which coincides with the 76.4% retracement of the widening move seen after President Macon called for snap Parliamentary Elections in mid-2024.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

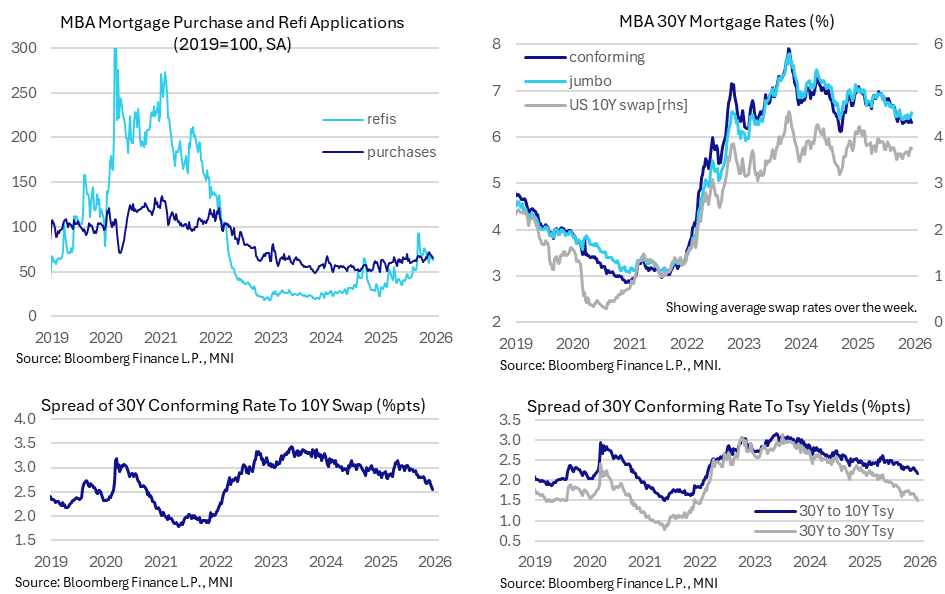

US DATA: Mortgage Applications Slip Further Despite Latest Spread Tailwind

- MBA composite mortgage applications slipped another -5.0% (sa) last week after the -3.8% in the week prior, on balance more than reversing a refi-driven increase in early December.

- Refis fell -5.6% after -3.6% and +14.3%, whilst new purchases fell -3.7% after -2.8% and -2.4%.

- Relative levels to 2019 averages: 62% for composite, 66% for new purchases (this peaked at 72% in late November) and 62% for refis (this peaked at 93% in a mid-September spike).

- There was little sign of response from a 7bp decline in the 30Y conforming rate to 6.31%, reversing the 5bp increase the week prior to come close to the 6.30% in October that was the lowest since Sep 2024.

- There could however be some distortion ahead of Christmas, with an unusually sharp divergence with jumbo rates which increased 8bp on the week to 6.52%. That 21bp spread over conforming was the widest since Oct 2024.

- There continues to be an increasingly significant tailwind from narrowing spreads over swap rates, with the 30Y conforming to the average 10Y swap rate spread narrowing 6.5bps to 255bp for a fresh low since Mar 2022.

- It compares with the peak of 315bp in May in post-tariff disruption, 285bp averaged in 1Q25 and 302bp averaged in 2024.

US TSYS: Mildly Firmer; Jobless Claims & 7Y Supply Ahead Before Early Close

Treasuries are mildly firmer overnight, sitting firmly within yesterday’s strong GDP-induced range amidst tiny futures volumes on Christmas Eve. Cash closes early at 1400ET and futures at 1315ET today.

- Reuters headlines that Japan is considering reducing super-long debt issuance and pausing an increase in 10Y issuance saw JGB futures gain on tiny volumes but with little spillover to Treasuries (after greater sensitivity to post-BoJ JGB moves).

- Cash yields are 0.5-1bp lower on the day, consolidating yesterday’s pullback after 10Y yields tested 4.20% with a high of 4.2001%, currently trading at 4.155%.

- TYH6 trades at 112-12 (+02+) in narrow ranges on tiny cumulative volumes of 120k.

- It sits comfortably within yesterday’s range of 112-17 (90mins before GDP) and 112-01+ (before a softer labor differential in the Conf Board survey and that yield test).

- Resistance remains intact at 112-21+ (50-day EMA) whilst yesterday’s low came close to the bear trigger at 111-29 (Dec 10 low). Further downside traction will again open the 4.20% yield level, which today equates to 112-02+ to continue to offer support just above that bear trigger.

- In rates space, Fed Funds futures see low chance of a Jan rate cut (3bp priced), with April less timely at a cumulative 17.5bp (22bp pre-GDP). A cut is still clearly expected in June under a new Fed chair (30.5bp vs 34.5bp pre-GDP).

- SOFR futures are unchanged to 1 tick firmer, with the terminal implied yield at the higher end of recent ranges at 3.155% (Z6).

- Today’s data focus is on weekly jobless claims at 0830ET.

- Attention should then turn to issuance, with the $44bn 7Y auction at 1130ET plus 4wk/8wk/17wk bills (1000/1000/1130ET). Yesterday’s 5Y saw little reaction to a small 0.1bp tail and the bid-to-cover slipping from 2.41 to 2.35.

US TSYS: Early SOFR/Treasury Option Roundup

Limited Treasury option volumes ahead of the Christmas holiday, SOFR options nil so far. Underlying futures steady in the short end to mildly higher. Projected rate cut pricing cools vs. early morning levels (*): Jan'26 steady at -3.3bp, Mar'26 at -12.3bp (-11.3bp), Apr'26 at -18.1bp (-17.3bp), Jun'26 at -31.1bp (-30bp).

- Treasury Options:

- over 3,000 TYF6 111.75 puts ref 112-12

- 3,053 TUF6 104.12/104.25 put spds vs. TUF6/wk1 FV 104.37 call spd

- over 12,600 TYF6 112 puts, 1 ref 112-11 to 11.5

- 1,000 TYG6 111/112 call spds ref 112-09.5

- 1,000 TYG6 112.5/113/114 broken call flys ref 112-10.5

- over 10,000 wk2 TY 112.5 calls, ref 112-11 to -11.5