BONDS: NZGBS: Yields Steady, NZ-US 10yr Spread Slightly Higher, Bond Sales Today

NZGB bond yields are flat to slightly higher in the first part of Thursday trade, outperforming a soft back drop from US Tsy yield on Wednesday (equity losses helped drive some US Tsy demand). NZGB yields are less than 0.5bps higher at this stage though, the 2yr around 2.52%, the 10yr 3.95%. Broader downtrends in NZ yields still look to be in play, although with have seen flatter trends in the aftermath of Monday's Q3 CPI report (which likely ruled out more aggressive RBNZ action at the Nov policy meeting). Market pricing remains for a 25bps cut at this meeting.

- Moves back up to 4.00% might draw buying interest in the NZ 10yr, while for the 2yr downside focus is likely to remain on a test of 2.50%. For 2yr swap rates, we have also stabilized and sit slightly above recent lows (near 2.25%), last around 2.30%.

- The NZ-US 10yr spread sits up slightly back around +1bps. We noted yesterday this spread was under fair value estimates. A simple regression of the 1Y3M forward swap spread against the 10-year yield differential over the past 18 months suggests the current differential is 6bps below its estimated fair value of +6bp.

- The local data calendar is empty until Sep filled jobs data prints next Tuesday.

- Note today we have 2030, 2036 and 2054 bond sales on tap.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

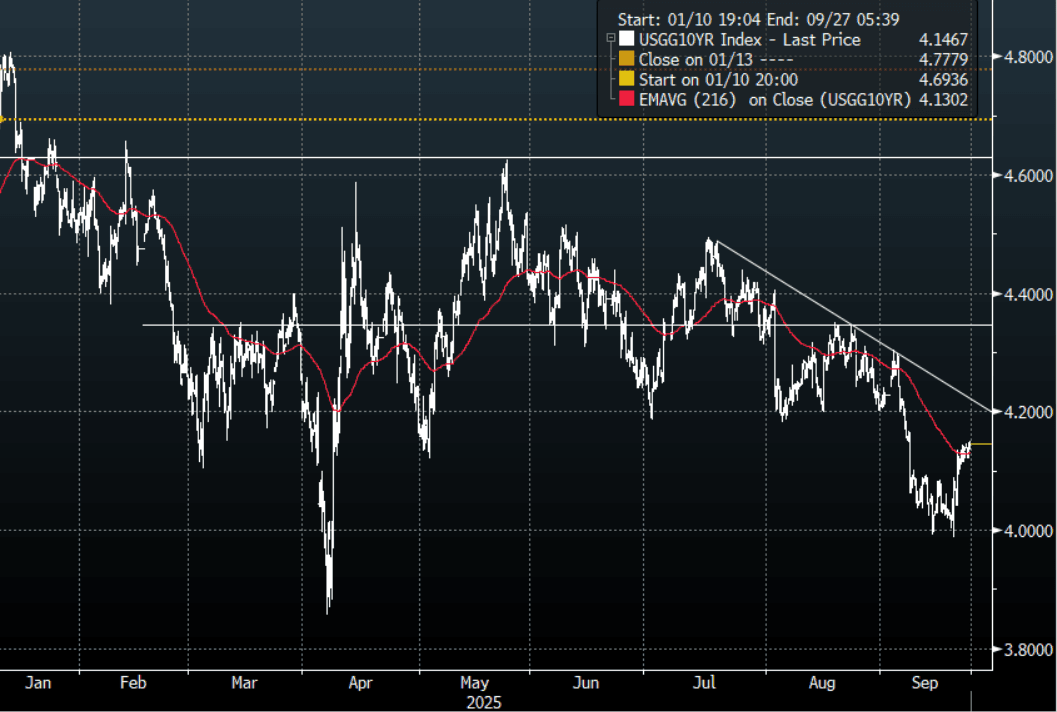

US TSYS: Yields Extend Retracement Higher

TYZ5 reopens at 112-23+, up 0-00+ from closing levels in today’s Asia-Pac session.

- Overnight the US 10-year yield had a range of 4.1196% - 4.1505%, closing around 4.147%.

- Treasury yields extended their retracement higher overnight; (2s10s -1.22 at 54.158, 5s30s -0.40 at 105.935).

- 10-Year Yields could not extend below 4.00% and have bounced as the Fed could not meet the markets very dovish expectations. The first buy-zone is now back towards the 4.20% area where I suspect demand should return initially. A sustained break through 4.00% is needed for the focus to then turn towards the 3.80% area.

- MNI FED: Atlanta's Bostic Pencils In No More Cuts this Year, But Watching Data. Atlanta Fed President Bostic (non-2025/2026 FOMC voter) appears to have stuck to his pre-September Fed meeting outlook for just 1 cut this year, telling the WSJ in an interview that "I had one cut for this year. I didn't say the timing for that. So this could easily be the one cut. And so for that, I'm fine with it. I think moving forward, the data is going to be really important.”

- MNI FED: Gov Miran: Appropriate Rates In 2.00-2.50% "Ballpark". New Fed Governor Miran unsurprisingly argues for significantly lower policy interest rates in his first prepared remarks since being appointed to the Board, calling current rates "very restrictive". The central basis of his argument is that the neutral rate has shifted lower, making immediate easing appropriate.

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

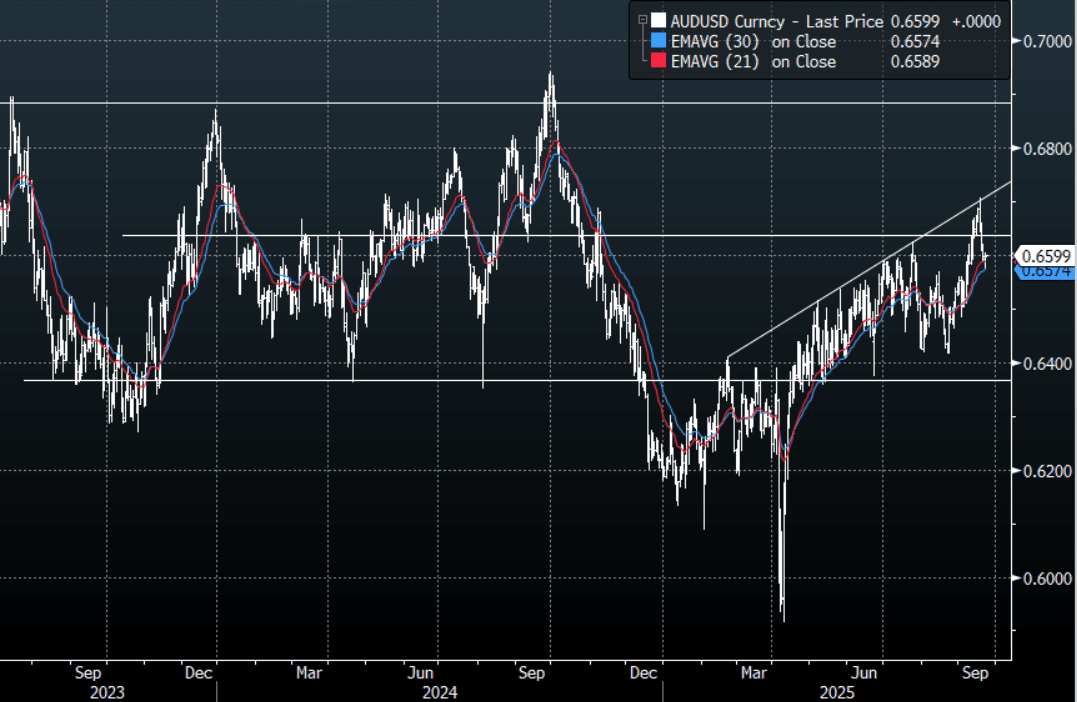

AUD: AUD/USD - Doing Work Around 0.6600

The AUD/USD had a range overnight of 0.6575-0.6603, Asia is trading around 0.6600. US stocks, just another day and another all-time high, nothing stops this train. The USD retracement stalled though as sellers reemerged even with some clearly hawkish rhetoric from Fed speakers overnight. The AUD/USD continues to do some work around 0.6600 and should still see dips supported for now with the first buy-zone back towards the 0.6550 area.

- Bloomberg - “Morgan Stanley Says Sell Dollar Versus Aussie and Loonie. The Federal Reserve’s perceived emphasis on the job market at the expense of inflation will see the US dollar’s decline widening, according to Morgan Stanley strategists who now recommend selling the greenback versus the Canadian and Australian dollars.”

- MNI FED: Cleveland's Hammack: Policy Very Mildly Restrictive, Concerns On More Cuts. Cleveland Fed President Hammack (hawk, 2026 FOMC voter) sounds extremely cautious about making further cuts: "I am laser focused on inflation. And that's why to me, I think that we should be very cautious in removing monetary policy restriction, because I think it's important that we stay restrictive to bring inflation back down to target.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6530(AUD415m), 0.6650(AUD908m), 0.6680(AUD486m). Upcoming Close Strikes : 0.6450(AUD529m Sept 24), 0.6600(AUD703m Sept 24), 0.6720(AUD791m Sept 24) - BBG

- CFTC Data last week shows Asset managers started to significantly reduce their shorts, -41095(Last -68333). The Leveraged community has pulled back their shorts to be almost flat, -1519(Last -5081).

- Data/Event: S&P Global Australia PMI’s

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

CNH: CNH Lags USD Softness, PBoC To Be Data Dependent

USD/CNH tracks near 7.1160 in early Tuesday dealings, after posting little net change for Monday's session. This lagged broader USD softness, with the BBDXY index down 0.20%, while the DXY index fell by 0.30%. USD sentiment moved off earlier Monday highs, with a subdued tone amid a lighter economic calendar to start the week, with central bank speakers providing little to boost volatility. Spot USD/CNY finished up at 7.1145, while the CNY CFETS basket tracker rose 0.20% to 96.55 (per BBG).

- For USD/CNH technicals, little has changed. The 20-day EMA is around 7.1265, while the 50-day is close to 7.1500. All key EMAs are drifting lower. On the downside, we are comfortably above recent lows of 7.0851.

- From late yesterday, the PBoC remains committed to a moderately accommodative stance, and any policy adjustment will be data-based, Governor Pan Gongsheng told reporters on Monday, in comments which provided few clues as to any future easing.

- US lawmakers, visiting China in recent days, called for fair and reasonable access to China's market, per BBG. They met with China's Vice Premier He Lifeng.

- In the cross asset space, US Tsy yields continued to tick higher, aiding US-CH yield differentials, but this didn't support broader USD sentiment.

- In Monday US trade, the Golden Dragon Index lost 0.96%, down for the 3rd straight session. Onshore equities did better yesterday, but remain off recent highs. The China to global equity ratio is lower over the past week, providing less downside impetus to USD/CNH.