BONDS: NZGBS: Bull-Flattener Moves Curve Away From Cycle High

NZGBs closed showing a bull-flattener, with benchmark yields 3-7bps lower. * Cash US tsys are ~1bp ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RBA: More Concerned About Inflation & Its Drivers, Waiting For Q4 CPI

In a unanimous decision, the RBA’s Board decided to leave rates at 3.6% where they have been since August, which was expected. While it remains “cautious”, the statement shifted slightly hawkish with more concern regarding rising inflation but it needs “longer to assess the persistency of inflationary pressures”. It noted that there was “uncertainty” around monthly CPI data given it is new signaling that the Board was content this month to wait for Q4 CPI on 28 January ahead of the next decision on 4 February. Governor Bullock speaks to the press at 1530 AEDT.

- In terms of inflation, the RBA noted that the October CPI suggested “some signs of a more broadly based” increase in inflation and it could be “persistent” and needs “close monitoring". It also added to the guidance paragraphs that risks have now “tilted to the upside”.

- There was also concern around inflationary drivers. It pointed out that it is the WPI that has peaked while “broader measures” were strong and that unit labour cost growth remains “high”.

- Capacity utilisation was also said to be above its “long-run average” and reiterated that firms are finding it difficult to source labour. Consistent with this, Bullock said to the senate last week that while it is difficult to estimate, she believes that the output gap has closed.

- The Board no longer sees policy as “a little restrictive” but added the degree of restrictiveness to the list of uncertainties.

- It is also waiting for the full effect of 2025’s 75bp of easing to “flow through fully to demand, prices and wages”. But the recovery continues and private demand growth remains stronger than the RBA expected.

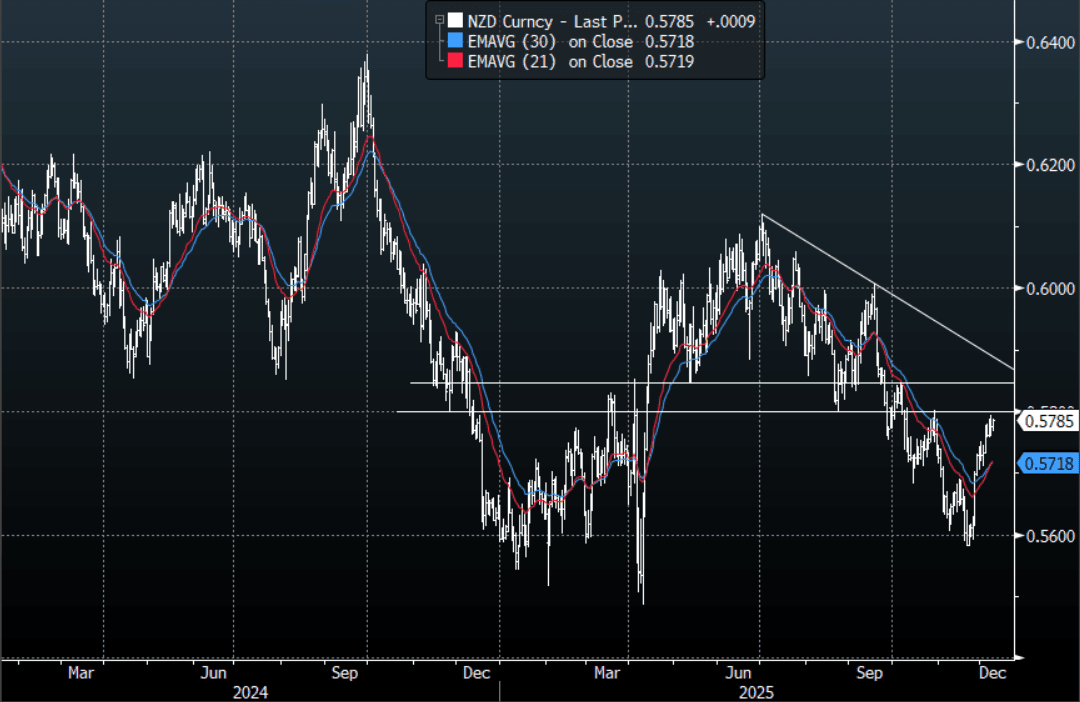

NZD: NZD/USD - A Little Higher Looking To Test 0.5800 Again

The NZD/USD had a range today of 0.5767-0.5788 in the Asia-Pac session, going into the London open trading around 0.5785, +0.15%. The NZD/USD has drifted a little higher having a look back toward the 0.5800 area once again in our session. On the day, watch the price action back toward 0.5780-0.5800 if price cannot retake the highs we could see a potential reversion back to the mean. Support is around 0.5735-0.5755 area first up and then the more important 0.5670/0.5700 area. Some tough resistance approaching in the 0.5800-0.5850 area, I suspect sellers could fade a move here initially.

- Bloomberg - “Westpac New Zealand is raising interest rates on fixed-term home loans of two years or longer, the lender says in an emailed statement. Effective Wednesday, a two-year special home loan will carry a 4.75% rate up from 4.45%. Five-year special rate rises to 5.29% from 4.49%. Says fixed rates are mainly driven by movements in wholesale interest rates rather than the OCR and wholesale rates have lifted materially.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5700(NZD557m Dec 10), 0.5700(NZD306m Dec 12) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 33 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Little Changed After RBA Hold, RBA Cautious About Inflation Risks

ACGBs (YM -3.5 & XM -2.5) are little changed after the RBA decision to leave the cash rate at 3.60%, as widely expected, but noted that risks to inflation are tilted to the upside. Press conference at 1530 AEDT.

- The last paragraphs of the RBA statement stated that inflation risks have shifted higher and that the RBA wanted more time to judge how persistent these pressures are. Demand is recovering and the labour market is still somewhat tight, though easing gradually. As a result, the Board is staying cautious and will update its outlook as new data come in. It will closely monitor global conditions, domestic demand, inflation and labour-market trends, and stands ready to act as needed to achieve price stability and full employment.

- Cash US tsys are slightly cheaper in today’s Asia-Pac session.

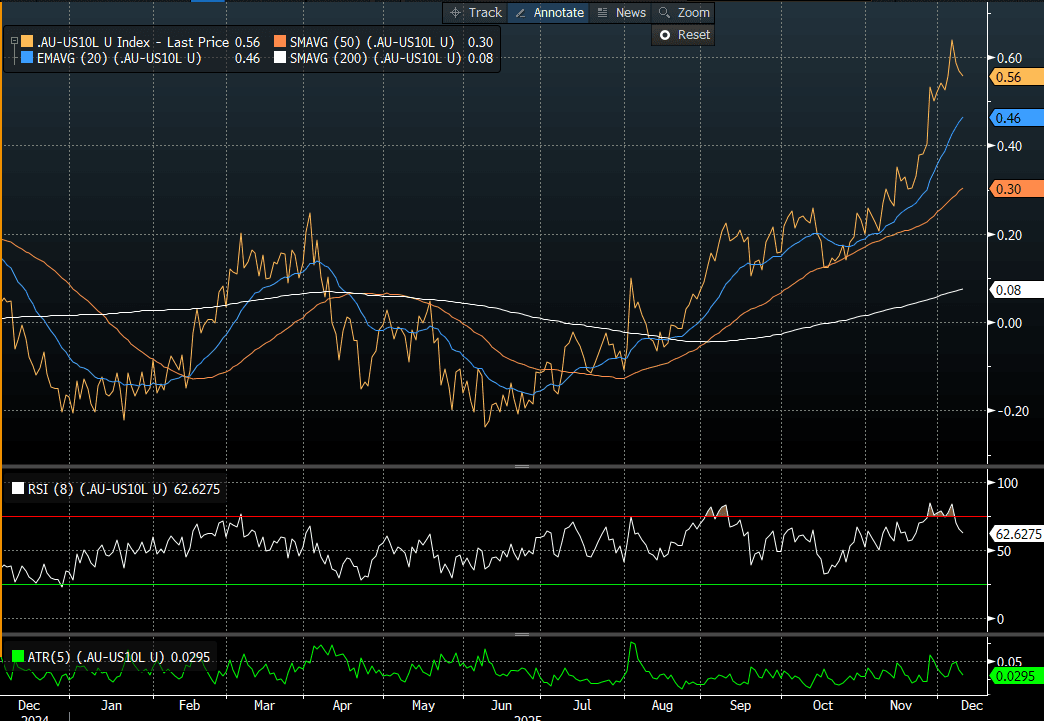

- Cash ACGBs are 2-3bps cheaper on the day, with the AU-US 10-year yield differential at +56bps. The differential broke above the ±30bps range that had persisted since November 2022 in October. It peaked around +60bps at the end of last week (see chart).

- The bills strip has bear-steepened, with pricing flat to -6.

- RBA-dated OIS pricing is little changed after the decision. Tightening expectations are seen across all meetings, with the probability of a 25bp hike rising from 15% for February to 118% by August and 154% by December 2026.

Bloomberg Finance LP