NZD: NZD/USD - Moves Toward 0.6100 As Commodities Soar & The USD Struggles

The NZD/USD had a range today of 0.6044-0.6086 in the Asia-Pac session, it is currently trading arou...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

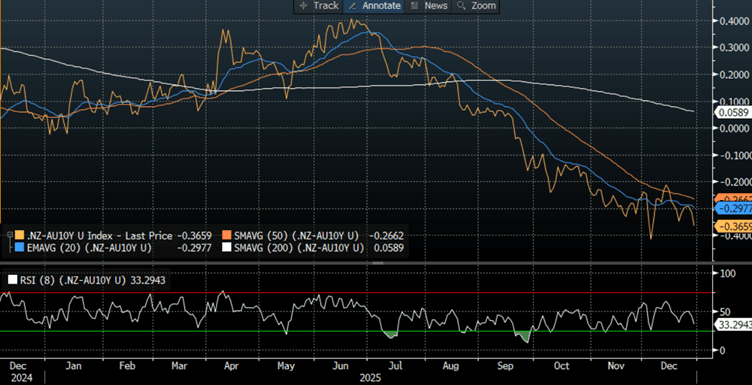

BONDS: NZGBS: Bull-Flattener With NZ-AU 10Y Diff Near Cycle Lows

NZGBs closed showing a bull-flattening of the 2/10 curve, with benchmark yields 2-6bps lower.

- The NZ 10-year outperformed ACGBs by ~6bps, with the differential returning to within striking distance of its cycle low of ~-40bps.

- Cash US tsys are slightly richer in today’s Asia-Pac session before the release of the Federal Reserve’s meeting minutes later Tuesday. The Fed will release minutes of its Dec. 9-10 meeting, where the central bank lowered the policy rate by 25bps. Fed Governor Stephen Miran voted against the decision in favour of lowering rates by twice as much.

- Swap rates closed 4-7bps lower, with tighter implied swap spreads.

- RBNZ-dated OIS pricing is slightly softer across meetings. No tightening is priced for February, while October 2026 assigns 23bps.

- The local calendar will be empty until Cotality Home Value data on January 1.

Bloomberg Finance LP

PRECIOUS METALS: Gold & Silver Bounce Back As Holidays Drive Volatility

Thin volumes related to the current holiday period are amplifying moves in precious metals, especially silver which is a significantly smaller market than gold. This and year-end positioning is likely driving current volatility. Silver rose over 10% on Friday and then fell around 9% yesterday on profit taking and is up 3.2% so far today. The BBDXY USD index has range traded and is flat as are US yields.

- Later the December FOMC minutes are published. If they show a more dovish shift, then non-yield bearing precious metals are likely to rally. The USD OIS market has 21bp of easing priced in by the April meeting and 56bp by September.

- Both gold & silver remain in overbought territory while technicals signal that corrections remain corrective.

- Gold is up 0.7% to $4362.5/oz in today’s APAC session, close to the intraday high at $4369.2. It fell to $4323.86 early in trading.

- Silver continued its sell off early in trading to a low of $71.163 but then trended higher and is now up 3.2% to $74.45 just off today’s peak of $74.625. It breached $70 last week and has remained above it since finding support at this level on Monday.

- The CME decision to increase the cash held to back precious metals futures positions was a “normal review of market volatility”, according to DJ. Positions were liquidated on Monday where the cash wasn’t available to meet the new requirements.

- In terms of data, US 13 December ADP employment, December MNI Chicago PMI, December Dallas Fed services and October house price data print. Also preliminary December Spanish CPI data are released.

JGBS: Modest Twist-Flattener At Lunch

At the Tokyo lunch break, JGB futures are little changed, +2 compared to settlement levels.

- Bloomberg – “JGB investors are in the final session of 2025 and they’re holding onto the negative stance which has prevailed through most of this year, looking for further losses in January. Despite the large price decline since the BOJ rate hike 11 months earlier, there is little sign of traders trimming exposure with open interest levels for JGB futures still near the high end of this year’s range.”

- Cash US tsys are slightly richer in today’s Asia-Pac session before the release of the Federal Reserve’s meeting minutes later Tuesday. The Fed will release minutes of its Dec. 9-10 meeting, where the central bank lowered the policy rate by 25bps. Fed Governor Stephen Miran voted against the decision in favour of lowering rates by twice as much.

- Cash JGBs have twist-flattened across benchmarks, with yields 1.5bps higher to 1.5bps lower. The benchmark 10-year yield is 0.2bps higher at 2.055% versus the cycle high of 2.104%.

- Swap rates are flat to 2bps higher, with the 5-year leading.