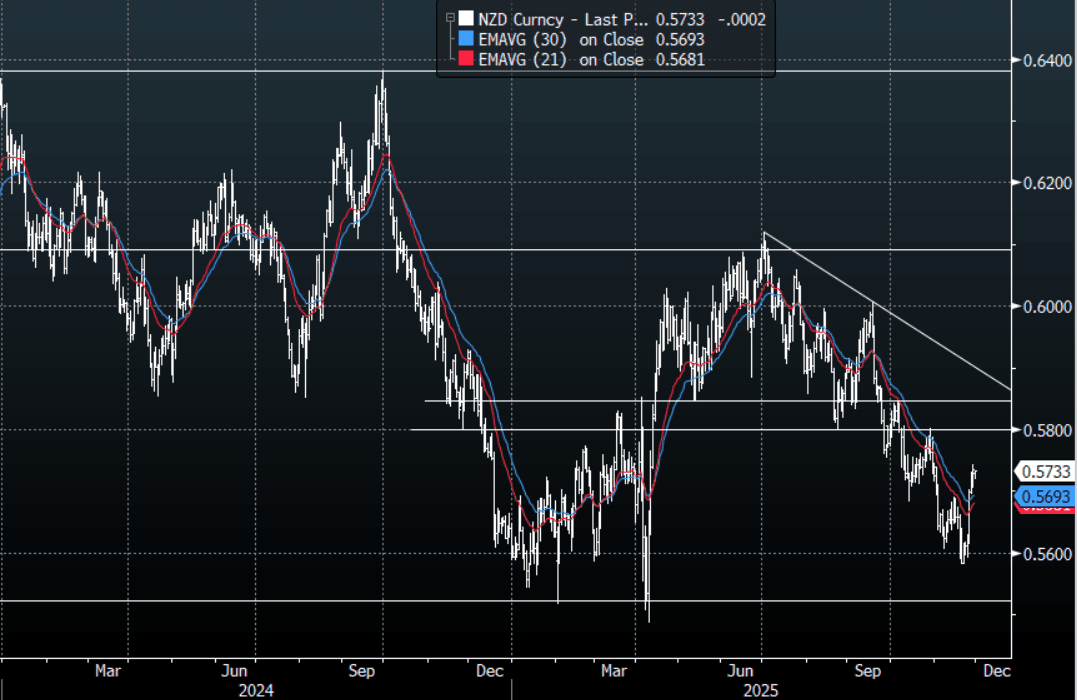

NZD: NZD/USD - Looking To Build Momentum Above 0.5700

The NZD/USD had a range Friday night of 0.5704 - 0.5744, Asia is trading around 0.5730. The NZD found some good demand back toward 0.5700 on Friday. Positioning still looks to be an issue in the short term. While the risk backdrop remains constructive this should provide further headwinds for the NZD shorts and I suspect we see more of the weaker hands pressured. On the day look for dips back toward 0.5680/0.5700 to potentially be supported, as the market turns its focus toward 0.5760 first then the more important 0.5800-50 resistance.

- MNI BRIEF: China November Manufacturing PMI Remains Below 50. China's Manufacturing Purchasing Managers Index rose by 0.2 points to 49.2 in November from October, remaining below the breakeven 50 mark for the eighth month.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5665(NZD309m), 0.5940(NZD427m). Upcoming Close Strikes : 0.5575(NZD547m Dec 3), 0.5700(NZD4356m Dec 2) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 41 Points

- Data/Event: Building Permits

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Gov Waller: Still Advocating For A December Rate Cut

Gov Waller, one of the FOMC's more prominent doves, makes clear in an appearance on Fox Business that he supports a follow-up rate cut in December. He makes reference to Chair Powell's press conference comment that the Fed could skip a cut at the December meeting due in part to a lack of official government data during the federal shutdown (Powell: “what do you do if you are driving in the fog? You slow down").

- Waller says today: "Right now, we know that the labor market has been weak... We know inflation is going to come back down. Inflation expectations are anchored, and in that world, the standard of central bank wisdom is to look through it and proceed with worrying about the labor market. So in my view, we should just look at what the data is telling us and proceed on policy that way.... So this is why I'm still advocating that we cut policy rates in December, because that's what all the data is telling me to do. The fog might tell you to slow down. It doesn't tell you to pull over to the side of the road. You still have to go. You may want to be careful, but it doesn't mean to stop, and ... the right thing to do with policy is to continue cutting."

- This is of particular interest since he appeared to suggest he would have a more cautious outlook on further easing after cutting in October.

USDCAD TECHS: Doji Candle Reversal Signal

- RES 4: 1.4200 Round number resistance

- RES 3: 1.4167 50.0% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.4111 High Apr 10

- RES 1: 1.4039/80 High Oct 24 / 16 and the bull trigger

- PRICE: 1.4018 @ 16:25 GMT Oct 31

- SUP 1: 1.3888 Low Oct 29 and key short-term support

- SUP 2: 1.3848 Bull channel base drawn from the Jul 23 low

- SUP 3: 1.3769 Low Sep 19

- SUP 4: 1.3727 Low Aug 29 and a bear trigger

A strong rally in USDCAD Thursday highlights a reversal of the corrective bear leg between Oct 14 - 29. Note that the climb suggests that Wednesday’s candle - a doji - is a valid pattern and therefore a potential reversal signal. The pair is holding on to its latest gains - a bullish signal. A continuation higher would open 1.4080, the Oct 16 high and a bull trigger. Key short-term support is at 1.3888, the Oct 29 low.

LOOK AHEAD: US Macro Week Ahead: Alternate Labor Data and ISM Surveys

- Next week sees another week of US government shutdown restricted data releases. That means no BLS nonfarm payrolls report for October (a second month now without one) but labor data will nevertheless see plenty of attention from alternative sources.

- That includes ADP private payrolls and Revelio Labs’ labor statistics along with the final version of the Chicago Fed's unemployment rate nowcast after its advance release penciled in 4.35% for little change from its 4.34% estimate for September after 4.32% in the actual BLS data for August.

- We will also continue to receive another set of state-level weekly jobless claims which can be used to reasonably accurately gauge a nationwide estimate. Latest claims data pointed to a five-week low for initial claims, coming a day after Fed Chair Powell drew “some comfort” from claims and vacancies data suggesting “maybe continued gradual cooling, but nothing more than that”.

- Elsewhere, October business surveys will be in focus, especially the ISM manufacturing and services releases. Flash PMIs from S&P Global suggested that US business activity growth accelerated in October to the second-fastest so far this year, accompanied by the largest rise in new business seen in 2025 to date. The PMIs have however been notably more optimistic than the ISM surveys for a few months now.

See MNI's updated guide to the next 7 days of US data releases here.