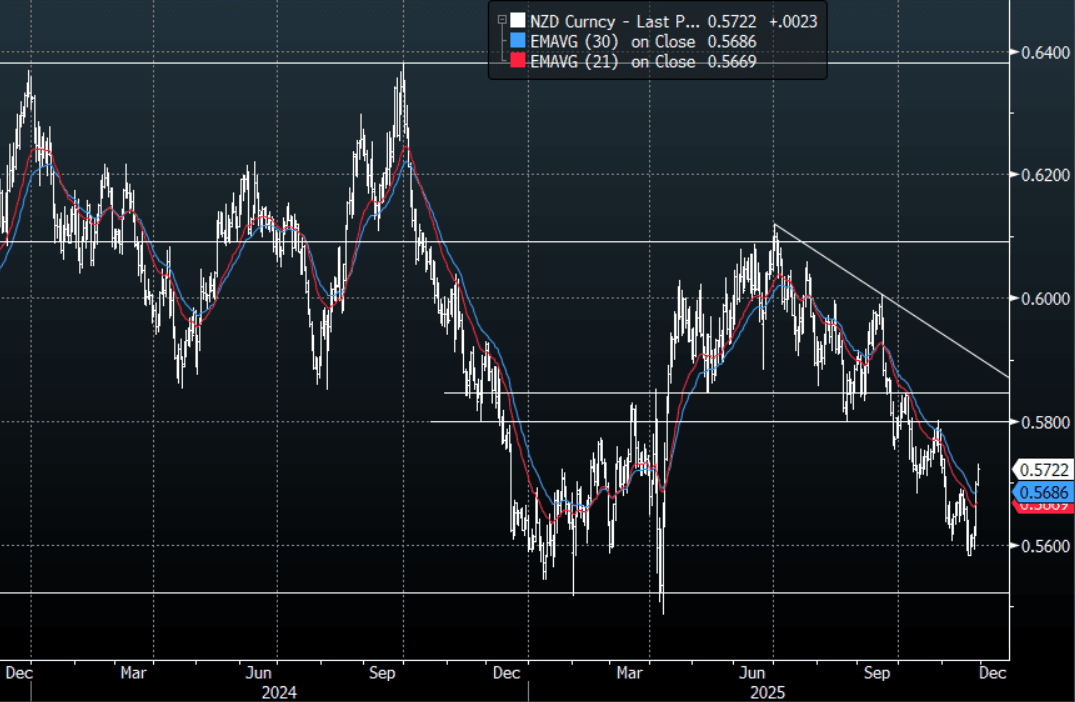

NZD: NZD/USD - Holds Above 0.5700

The NZD/USD had a range overnight of 0.5709 - 0.5730, Asia is trading around 0.5722. A very quiet overnight session with the US out. Positioning still looks to be an issue in the short term. While the risk backdrop remains constructive this should provide further headwinds for the NZD shorts and I suspect we see more of the weaker hands pressured. On the day I suspect dips back toward 0.5680/0.5700 will be supported, as the market turns its focus toward 0.5760 first then the more important 0.6800-50 resistance. I think it should be a quiet day all things being equal.

- MNI INTERVIEW: RBNZ Sees Short-Term Hike Highly Unlikely. Risks to the Reserve Bank of New Zealand’s 2.25% Official Cash Rate remain balanced, with policy likely to stay on hold for the foreseeable future and a hike in the near term highly unlikely, Chief Economist Paul Conway told MNI, emphasising that the RBNZ retains full flexibility to adjust rates in either direction depending on economic developments.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5650(NZD300m), 0.5550(NZD300m). Upcoming Close Strikes : 0.5575(NZD547m Dec 3), 0.5940(NZD427m Dec 1) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 47 Points

- Data/Event: ANZ Consumer Confidence Index: It fell 2.3% in October and has not been able to hold a move above the breakeven 100-mark for more than a month since Q3 2021. Filled Jobs: This will be the first data on the labour market for Q4. It signaled that employment had stabilised in Q3 but the RBNZ will be looking for it to improve to begin absorbing excess capacity in the labour market.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

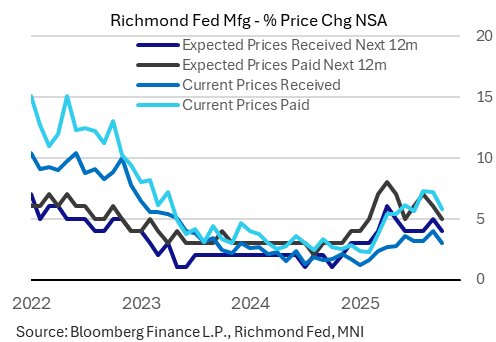

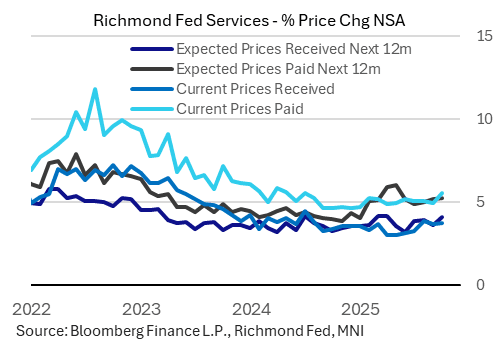

US DATA: Richmond Services Inflation Showing Some Signs Of Picking Up (2/2)

For Richmond Services inflation gauges, expressed in one-year lookback terms, current prices paid jumped to 5.5% from 5.0% to mark a joint-17 month high; meanwhile prior prices received picked up only slightly (to 3.8% from 3.7%, around recent levels).

- Conversely, expected prices received rose 0.5pp to 4.1% for a 6-month high, with expected paid steady at 5.2%.

- This stood out vs fairly flat readings in recent months, as well as the other 4 major regional Fed services surveys that all saw current prices paid gauges fall in October vs September.

- In manufacturing, though, current prices paid fell to a 3-month low 5.8% (7.2% in the prior 2 months), with received also pulling back (to 3.0%, a 5-month low, from September's 27-month high 4.0%). Expected prices paid and received (next 12 months) also fell 1.0pp apiece, to 5.0%/4.0% respectively.

- This stood out: only Richmond and Dallas saw prices paid diminish vs September (NY, Philly, KC all accelerated on the month).

- Overall we would characterize inflation in regional manufacturing as elevated but diminishing from 2025's highest rates, while services inflation has remained relatively steady but shows some signs of picking up.

AUDUSD TECHS: Recovery Extends

- RES 4: 0.6660/6707 High Sep 18 / 17 and a bull trigger

- RES 3: 0.6646 2.0% 10-dma Envelope

- RES 2: 0.6629 High Sep 30 & Oct 01 and key short-term resistance

- RES 1: 0.6586 High Oct 28

- PRICE: 0.6584 @ 16:05 GMT Oct 28

- SUP 1: 0.6440 Low Oct 14

- SUP 2: 0.6415 Low Aug 21 / 22 and a bear trigger

- SUP 3: 0.6373 Low Jun 23

- SUP 4: 0.6357 Low May 12

Tuesday gains in AUDUSD put the price through resistance into the 0.6574 key Fib retracement, tilting the near-term outlook bullish toward 0.6629 resistance. Attention remains on the Oct 14 reversal pattern - a hammer candle. It signals the end of the bear cycle that started Sep 17. The pair has traded through the 50-day EMA - a bullish development. Key support lies at 0.6440, the Oct 14 low. A break of this level would cancel the reversal pattern and reinstate a bear threat.

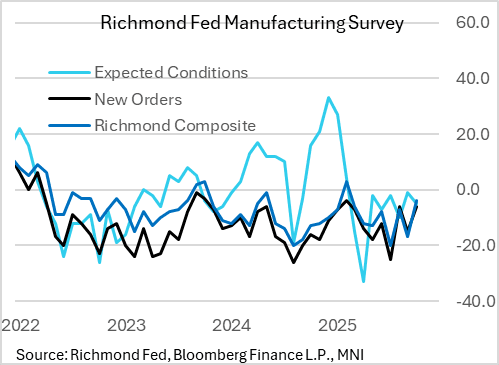

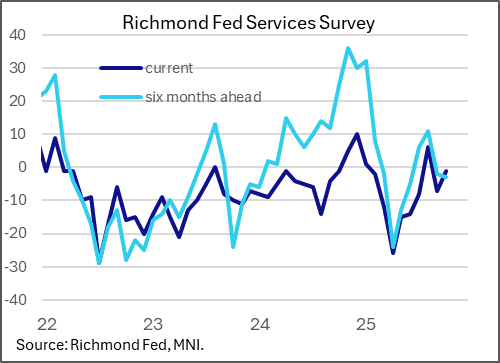

US DATA: Richmond Fed Manufacturing Aligns With National Improvement (1/2)

The Richmond Fed's Fifth District sectoral surveys showed improvement in activity in October, but very divergent inflation sequential developments across Manufacturing vs Services.

- Starting with activity, the manufacturing survey's Composite Index showed a strong improvement in October to -4 from -17 prior, marking the best reading since February and much better than the -12 consensus expectation, albeit still in soft territory (the report characterizes it as "slow" activity). New orders picked up to -6 from -15 (joint highest since February) and employment and shipments rose, though expectations fell to -5 from -1.

- This was generally in line with other regional Feds that saw manufacturing conditions improve in October vs September (joined by NY, KC, and Dallas, with Philadelphia coming in weak).

- Meanwhile the Services Composite recorded its second-highest print (-1) since January, after an unexpected setback to -7 in September after what had been 4 consecutive improvements. This index reading was very slightly above the 5-year average for the index. Meanwhile the 6-month outlook deteriorated to -3 from -2, for a 4-month low but basically steady.

- Overall the improvement bucked the broader trend, with NY, Philly and Dallas services weakening in the month (KC also improved).