NZD: NZD/USD - Consolidates Above 0.5900

The NZD/USD had a range Friday night of 0.5916 - 0.5939, Asia is trading around 0.5925. US equities momentum higher seemed to stall and the USD drifted lower again into the weekend. The NZD/USD found some demand back towards 0.5900 and is consolidating just above there. While still firmly in the 0.5850-0.6150 range it's tough to discern any real direction. Risk has opened a little higher this morning, E-minis +0.10%, NQU5 +0.15%.

- RBNZ Decision(MNI) - The RBNZ meets on Wednesday August 30 and is likely to cut rates 25bp to 3.0%, the mid-point of its estimate of "neutral", after pausing at the July meeting. With measures of core inflation within the 1-3% target band, wages moderating and activity remaining subdued, the MPC is likely to determine that further easing is needed. It will also publish a revised outlook.

- (Bloomberg Economics) -- New Zealand’s monthly price indicators for July look worrying on the surface. Yet with most pressures coming from global forces and a deteriorating labor market at home, we still expect the RBNZ to cut rates — not just in August, but again in the fourth quarter and 1Q26.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5925(NZD400m Aug 20), 0.5980(NZD660m Aug 21). - BBG

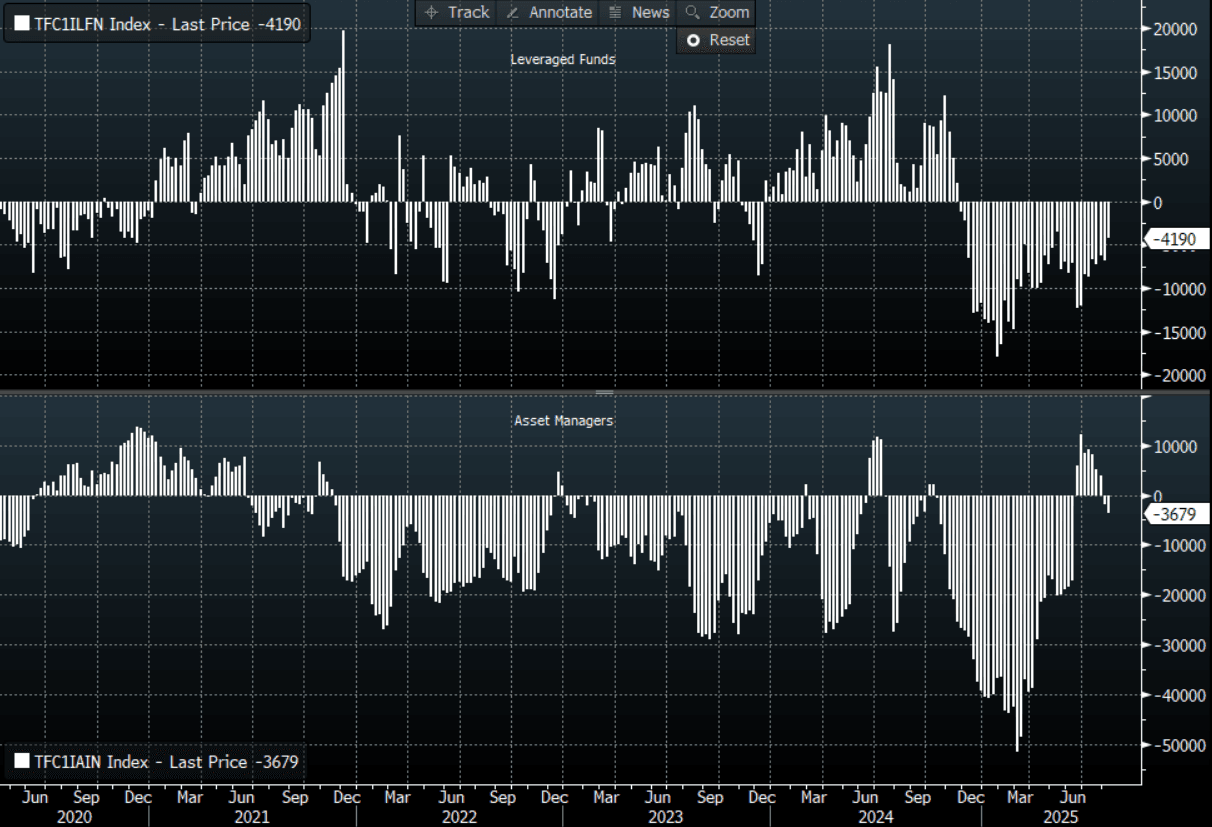

- CFTC Data shows Asset Managers have cut their longs completely and started to rebuild a short adding slightly in the NZD -3679(Last -1811), the Leveraged community though reduced their own shorts slightly -4190(Last -6778).

- Data/Event : Non resident Bond Holdings

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CANADA: July BOC Cut Pricing: From Distinct Possibility To Negligible This Week

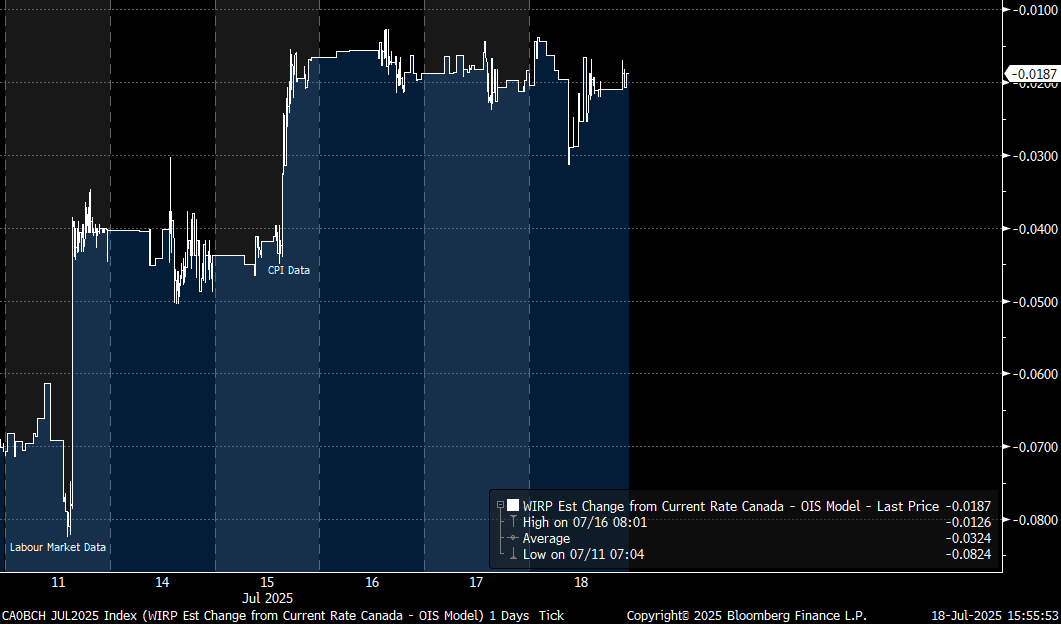

The implied probability of a July BOC rate cut has gone from a distinct possibility to negligible this week, following Tuesday's firmer-than-expected core inflation data.

- The accompanying chart shows implied pricing (in percentage points) for July's BOC decision - it dropped from around 30% implied (7+bp) prior to the labour market report last Friday, to under 20% going into CPI (4+bp), reducing after that to under 10% (<2bp).

- For the year as a whole, markets have priced out about 15bp of cuts through those two data points - now seeing about 15bp of easing through December. As such, it's very much in question whether the BOC's easing cycle is already at an end.

- Apart from the ongoing US-Canada trade negotiations, next week's scheduled highlight will be the BOC's Business Outlook Survey out Monday, followed by May Retail Sales out Thursday which will be the final major input into the macro puzzle for the BOC going into its decision on July 30.

| Meeting | Current | Last week's close (Jul 09) | Change since then | Cumulative Change From Current Rate (bp) |

| Jul 30 2025 | 2.74 | 2.68 | 5.6 | -1.9 |

| Sep 17 2025 | 2.69 | 2.60 | 9.3 | -6.0 |

| Oct 29 2025 | 2.65 | 2.53 | 12.1 | -10.5 |

| Dec 10 2025 | 2.61 | 2.45 | 15.7 | -14.6 |

USDCAD TECHS: Has Pierced The 50-Day EMA

- RES 4: 1.3920 High May 21

- RES 3: 1.3862 High May 29

- RES 2: 1.3798 High Jun 23

- RES 1: 1.3747/74 50-day EMA / High Jul 17

- PRICE: 1.3715 @ 16:56 BST Jul 18

- SUP 1: 1.3639/3557 Low Jul 08 / 03

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

USDCAD is trading closer to its recent highs. Attention is on resistance at 1.3747, the 50-day EMA. It has been pierced. A clear break of it is required to highlight a possible stronger short-term reversal. This would open 1.3798, the Jun 23 high. For now, a bear trend remains firmly in place. A resumption of weakness would refocus attention on key support at 1.3540, the Jun 16 low. Clearance of this level would confirm a resumption of the downtrend.

US: Macro Week Ahead: A Quieter Data Week Headlined By Flash PMIs

From our US Macro Weekly (here):

- It’s a quiet economic calendar next week, headlined by flash PMIs, durable goods orders, home sales and a latest weekly update for jobless claims.

- With the start of the FOMC blackout, Fed Chair Powell’s welcome remarks on Tuesday won’t touch on monetary policy.

| Date | ET | Impact | Event |

| 22 Jul | 0830 | ** | Philadelphia Fed Nonmanufacturing Index |

| 22 Jul | 0830 | Fed Chair Jerome Powell | |

| 22 Jul | 0855 | ** | Redbook Retail Sales Index |

| 22 Jul | 1000 | ** | Richmond Fed Survey |

| 22 Jul | 1300 | Fed Vice Chair Michelle Bowman | |

| 23 Jul | 0700 | ** | MBA Weekly Applications Index |

| 23 Jul | 1000 | *** | NAR existing home sales |

| 23 Jul | 1300 | ** | US Treasury Auction Result for 20 Year Bond |

| 24 Jul | 0830 | *** | Jobless Claims |

| 24 Jul | 0945 | *** | S&P Global Manufacturing Index (Flash) |

| 24 Jul | 0945 | *** | S&P Global Services Index (flash) |

| 24 Jul | 1000 | *** | New Home Sales |

| 24 Jul | 1100 | ** | Kansas City Fed Manufacturing Index |

| 24 Jul | 1300 | ** | US Treasury Auction Result for TIPS 10 Year Note |

| 25 Jul | 0830 | ** | Durable Goods New Orders |