EU FINANCIALS: Nykredit Realkredit: Q3 25 Results

(NYKRE; A1pos/A+/A+)

Small credit positive. 2025 guidance range narrowed towards top end of range and improved slightly. No obvious issues with Spar Nord integration. CET1 stable qoq.

Numbers are a bit busy with the acquisition of Spar Nord being fully integrated in Q3, while only 2 months of Q2. Q2 also contained elevated provisions from the acquisition and Q3 adds a DKK 1,352m bank shares value adjustment and DKK871m of integration costs.

Q3 numbers of Nykredit ex-spar Nord look Solid, with c.4% NII and c.14% non-interest income growth. The integration also seems to be going well, with 2025 guidance lifted slightly. Overall cost of risk remains low.

The combined banks CET1 ratio was 17.4% in Q3 (+0.1% QoQ)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

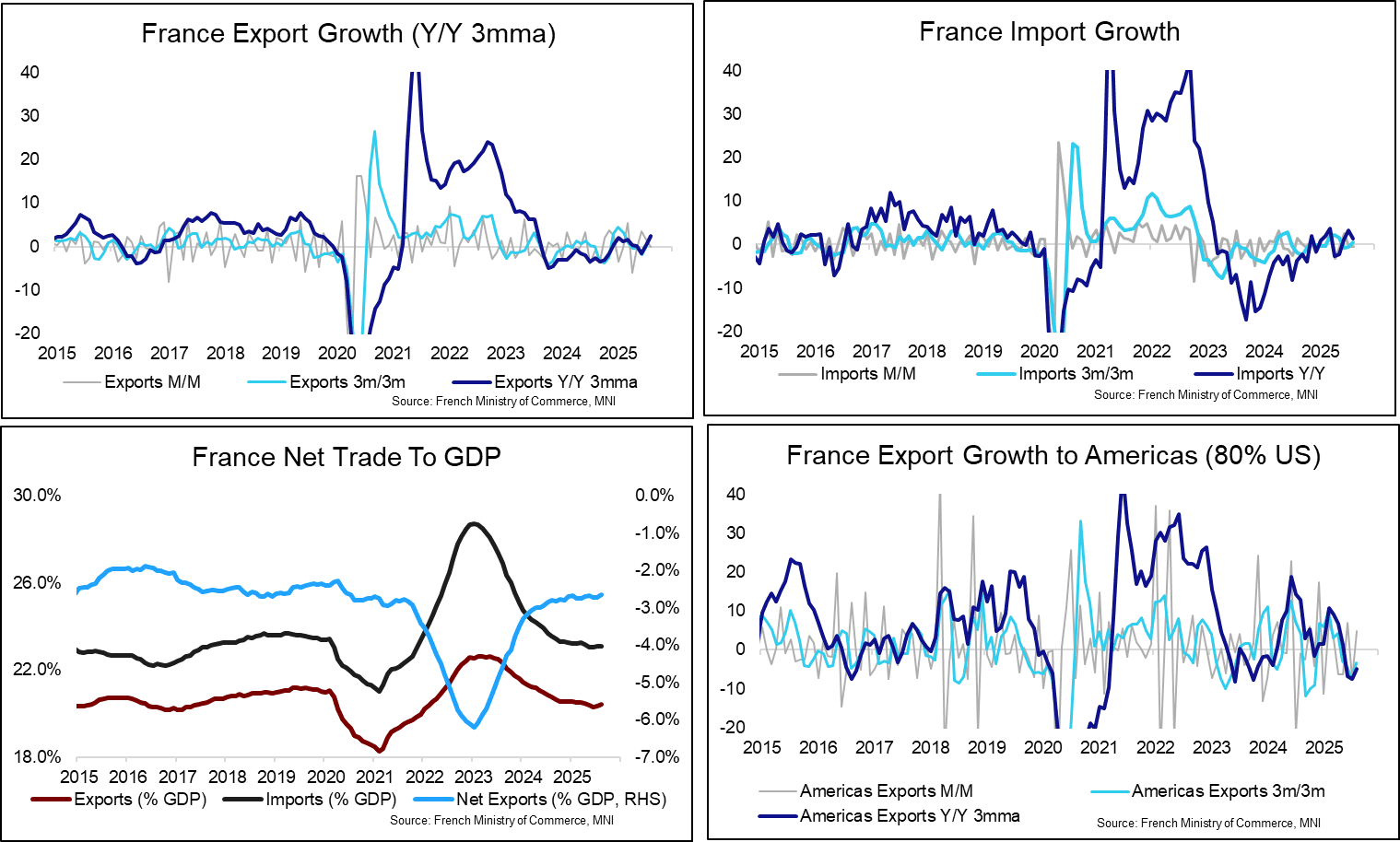

FRANCE DATA: Export Growth Recovering But Momentum Weak

The French trade deficit was E5.53bln in August, down from E5.74bln in July (revised from E5.56bln initial) and a year-to-date high of E7.42bln in February. Assuming unchanged nominal GDP growth of ~0.5% Q/Q in Q3, this implies a steady goods trade deficit of around 2.7% GDP.

- Imports fell 0.4% M/M for the second consecutive month, a sign of continued weakness in domestic demand against a backdrop of ongoing political/fiscal/economic uncertainty. However, Y/Y import growth continues to slowly recover from the 2023 lows, trending back toward pre-covid growth rates.

- Total exports fell 0.1% M/M in August, after two solid months of 3.5% and 1.7% growth in June and July. Like imports, a recovery in annual export growth from the 2023 lows is intact, though momentum is lacking. This may reflect the direct impact of US tariffs, even with trade policy uncertainty having declined since the EU-US trade agreement was struck in August. Although exports to the US rose 4.9% M/M in August, 3m/3m and Y/Y 3mma growth remains negative.

- September’s PMI round was in fitting with this theme:

- Manufacturing PMI: “Exports were also a drag on overall orders during the latest survey period, with companies mentioning US tariffs and generally sluggish market conditions as reasons for lower overseas demand.”

- Services PMI: “French service providers closed out the third quarter with another decline in new business from abroad. Albeit softer than August's year-to-date record, the contraction remained solid”.

BUNDS: Block trade

Bund Block trade, suggest buyer:

- RXZ5 3k at 128.37.

EGBs are lifted off their lows, Bobl is bought in 5k cumulative Volumes, BTP 1.7k and OAT 1k.

EURIBOR OPTIONS: More Call Condor Buyer

- ERM6 98.37/98.50/98.75/98.87c condor, bought for 1 in 5k.

This was also bought Yesterday in 14k.