EU CREDIT SUPPLY: Nykredit : Priced

Market Sources ------------------------------------------------------------------------------- Issu...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

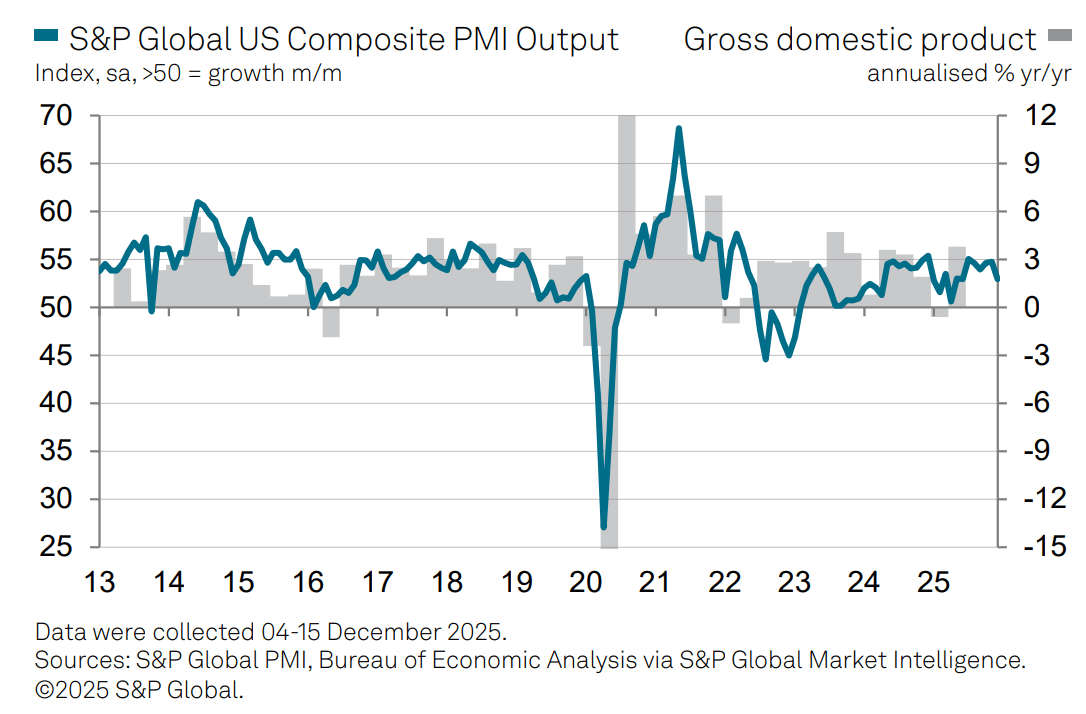

US DATA: Broad-Based Softening, Higher Prices Signaled By December Flash PMIs

Some highlights from the S&P Global flash December PMIs which were slightly below-expected (Manufacturing 51.8 vs 52.1 consensus and 52.2 prior; Services 52.9 vs 54.0 consensus and 54.1 prior):

- Activity: "US business activity continued to expand in December, according to early ‘flash’ PMI data. However, the rate of growth dropped to the weakest since June Composite: 52.9 vs 54.0 consensus, 54.1 prior), accompanied by the smallest rise in new business inflows for 20 months. Demand for services grew only modestly, rising at a sharply reduced rate, and new orders for goods fell for the first time in a year."

- Employment: "Employment growth also softened in December, falling to a marginal level that was the lowest since September. Although jobs growth edged up to the highest for four months in manufacturing, service sector employment came close to stalling, with firms reporting the smallest net gain to payrolls since April."

- Inflation: "Input cost inflation accelerated markedly in December, hitting the fastest since November 2022. Although manufacturers reported slightly slower inflation, the increase in input prices was historically elevated. In contrast, services cost inflation was the steepest in over three years. Cost increases were mostly blamed on tariffs alongside rising labor costs. Increased costs again fed through to higher selling prices, with the overall rate of inflation rising to the steepest since July and therefore amongst the greatest since the pandemic related price-surge of 2022."

MNI: US DEC FLASH MANUF PMI 51.8 (52.1 FCAST, 52.2 NOV)

- MNI: US DEC FLASH MANUF PMI 51.8 (52.1 FCAST, 52.2 NOV)

- US DEC FLASH SERV PMI 52.9 (54.0 FCAST, 54.1 NOV)

GILTS: Support Cluster Breached In Futures

Weakness in core global FI markets resumes after some vol. around the NFP release, with the noise and caveats surrounding that data (along with a firm U.S. retail sales control group reading) more than countering the initial dovish impact in Fed pricing & Tsys.

- Gilt futures base as 90.50 for now, piercing the initial support cluster at 90.62/53 in the process. Fresh extension lower would target the November 21 low (90.28).

- Yields 2.5-5.5bp higher, this morning’s bear steepening theme.

- 10-Year yields register the highest level of the month at 4.561%, with gilt bears targeting the November high (4.619%) next.

- Widening vs. Bunds maintained, 10s ~4.5bp wider at 168.5bp after failing to break below the September ’24 closing low in recent weeks (162.01bp).

- GBP STIRs extend on this morning’s data-driven (firm PMIs pointing to ongoing sticky inflation and firmer-than-market-expected wages data) hawkish repricing.

- Expectations for a cut at Thursday’s BoE decision remain intact (22bp priced), with 58.5bp of easing now priced through end ’26 (vs. 61.5bp late yesterday).

- SONIA futures flat to -6.0. December lows in SFIZ6 still 7.5 below prevailing levels.

- CPI data is due tomorrow. Our full preview of that release can be found here.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Dec-25 | 3.753 | -22.2 |

Feb-26 | 3.710 | -26.4 |

Mar-26 | 3.628 | -34.7 |

Apr-26 | 3.530 | -44.4 |

Jun-26 | 3.484 | -49.0 |

Jul-26 | 3.424 | -55.0 |

Sep-26 | 3.409 | -56.6 |

Nov-26 | 3.390 | -58.4 |

Dec-26 | 3.390 | -58.5 |