EU HEALTHCARE: Novo Nordisk: Q3 Results Headlines (NOVOB; Aa3/AA/NR)

Reduces guidance for FY again but M&A is the bigger topic.

• Q3 Sales DKK 74,976 +5% reported. A 2% miss vs Bloomberg consensus.

• Net Profit DKK 20bn -27% hit by large restructuring costs.

• EBITDA DKK 31.4bn -13%

• Gross margin fell to 76.1% from 84.1%

• R&D costs grew to DKK 15.4bn +62% as the company seeks a new winner.

• Guidance: Sales at CER +8-11% down from +8-14%. And Op Profit +4-+7% vs +10-16% (note restructuring charges).

• An agreement on TrumpRX expected soon.

• The bidding war for Metsera ~$10bn and the recent acquisition of Akera $4.7bn are the current focus. CEO says Metsera will not be blocked on anti-trust grounds.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITY OPTIONS: Estoxx Put Spread

SX5E (21st Nov) 5550/4800ps, bought for 66.3 in 4k vs 1.24k at 5660.00.

MNI: EUROZONE SEP CONSTRUCTION PMI 46.0 (46.7 AUG)

- MNI: EUROZONE SEP CONSTRUCTION PMI 46.0 (46.7 AUG)

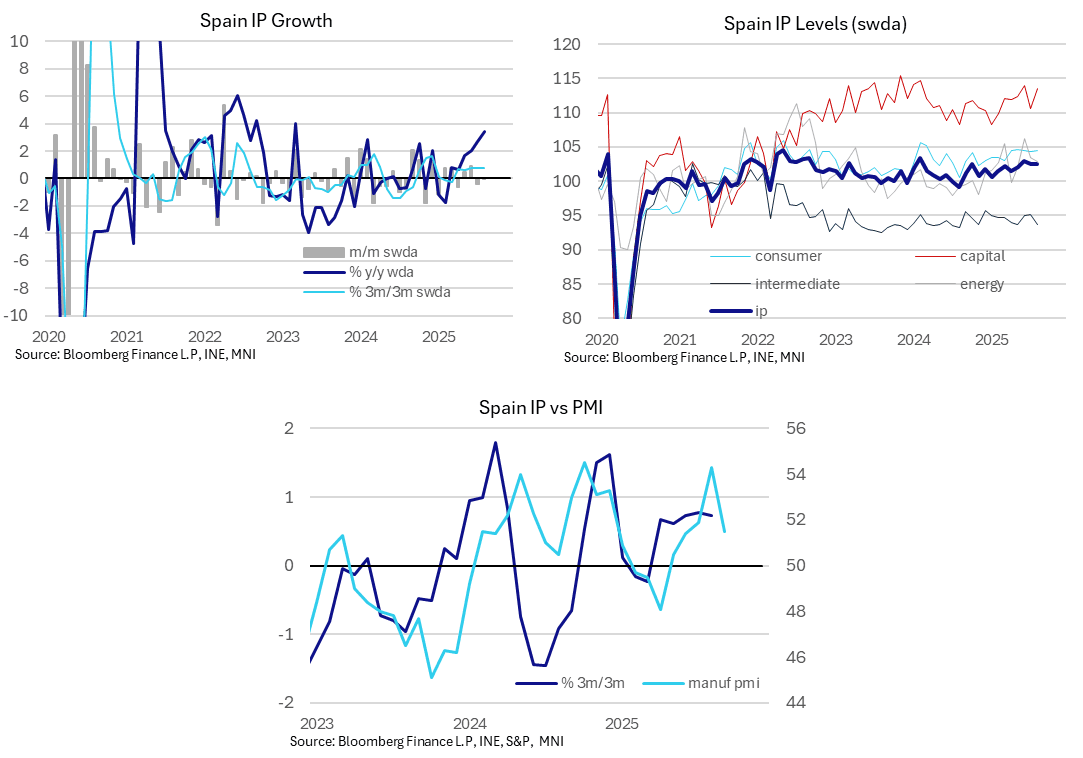

SPAIN DATA: Another Small Decline In IP, But Underlying Signals Remain Positive

Spanish industrial production fell 0.1% M/M SA in August, the second consecutive sequential decline. Only three analysts had submitted forecasts for the print, with estimates ranging from -0.2% to +0.7% M/M. Though sequential growth rates have been negative for two months now, 3m/3m and Y/Y comparisons remain in positive territory. Furthermore, signals from the manufacturing PMI suggests underlying IP momentum remains positive.

- Across sub-components, August’s M/M fall was centred in intermediate goods (-1.5% M/M) and energy (-0.7% M/M). There was a solid 2.6% increase in capital goods production, but this followed a 2.9% fall in July. Consumer goods production was +0.2% M/M, after -0.1% in July and -0.3% in June.

- Annual SA industrial production growth was 3.4% in August, up from 2.7% in July (revised up from 2.5% initial). This was the strongest Y/Y rate in over two years.