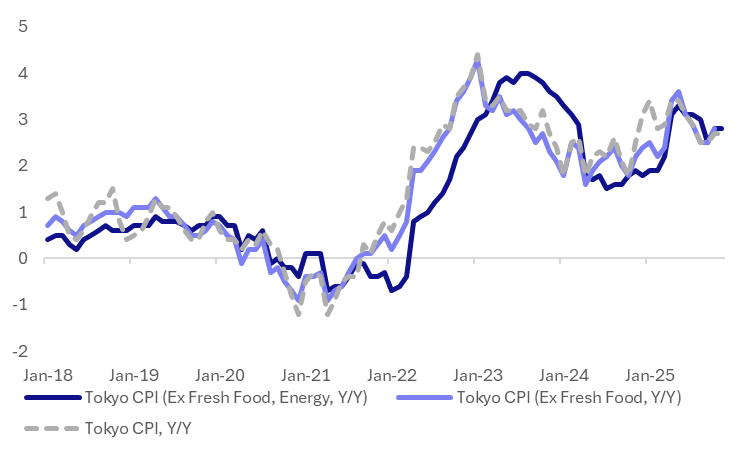

JAPAN DATA: Nov Tokyo CPI Close To Forecast, Services Y/Y Steady At 1.56%y/y

Japan's Nov Tokyo CPI print was fairly close to market expectations. Headline rose 2.7%y/y, in line with the consensus (while the Oct outcome was also revised down to this level, from 2.8%). Ex fresh food and energy printed 2.8%y/y (a touch above the 2.7% forecast), while the ex fresh food, energy measure was 2.8%y/y, in line with the prior and consensus forecast for today. The chart below plots the trend for these metrics in y/y terms. We are off earlier 2025 highs, but remain close to 3%.

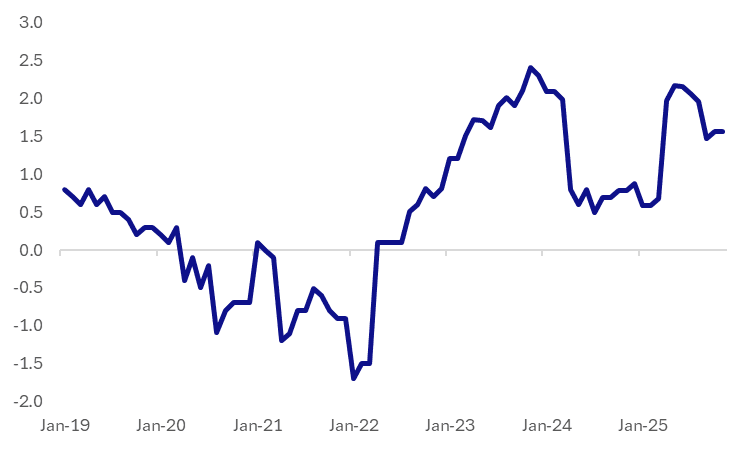

- The m/m outcomes still mostly showed firmness, albeit not as strong as the Oct gain. Services rose 0.2%m/m (after a 0.4% gain in Oct, while goods were up 0.5% (after a 0.9% rise in Oct). Services were little changed in y/y terms though at 1.56% (see the chart below).

- So whilst headline measures remain comfortably above the 2% inflation goal, services is still under this level. Hence today's data may not change much around Dec/Jan hike thinking from a BoJ standpoint. It has time to see if the recent tick up in services m/m momentum continues.

Fig 1: Tokyo CPI Y/Y Trends

Source: Bloomberg Finance L.P/MNI

Fig 2: Tokyo Services CPI Y/Y

Source: Bloomberg Finance L.P/MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGB TECHS: (Z5) Tilts Higher

- RES 3: 140.08 High Jun 13

- RES 2: 139.05 High Aug 4

- RES 1: 137.30 - High Sep 8 and key short-term resistance

- PRICE: 136.28 @ 15:48 GMT Oct 28

- SUP 1: 135.61 - Low Oct 08

- SUP 2: 135.39 - 1.618 proj of the Aug 4 - Sep 2 - Sep 8 swing (cont.)

- SUP 3: 134.69 - 2.000 proj of the Aug 4 - Sep 2 - Sep 8 swing (cont.)

Prices started the week well, growing the gap with next support into the 135.61 Oct 08 low. Despite this stability, prices remain inside the firm downtrend that’s dominated prices since mid-September, and prices will need to challenge resistance before signaling any broader reversal. Key short-term resistance has been defined at 137.30, the Sep 8 high. Further weakness would open 135.39 next, a Fibonacci projection.

JGBS: Futures Maintain Positive Bias, Back End Yields Lower, BoJ Seen On Hold

JGB futures maintained a positive bias post the Tokyo close on Tuesday, drifting up to 136.25, +.03 versus settlement levels. The lead from US Tsy was mildly positive, but recent ranges continue to hold ahead of the FED later. Anticipation is building ahead of a likely cut and possible decision to end QT. For JGB futures, we are above the 20-day EMA, but sub the 50-day (136.355), but more important resistance lies at 137.30. Dips under 136.00 remain supported at this stage.

- Focus remains on tomorrow's BoJ meeting outcome, with little hike risks seen. Market pricing only has 3bps worth of tightening priced in, while a full rate hike is nearly priced by March next year.

- In meetings with Japan officials, US Tsy Bessent avoided comments on the near term monetary policy outlook but noted sound monetary policy is important for anchoring inflation expectations and avoiding FX volatility. Earlier in the year Bessent remarked that the central bank was behind the curve from an inflation standpoint.

- In the cash JGB space, yields finished lower yesterday, particularly at the back end. The 10yr JGB under 1.65%, while the 30-yr near 3.07%, so again challenging 100-day EMA support. The 2/30s curve was a touch flatter at +212.5bps.

- Today we have Oct consumer confidence on tap for Oct.

GOLD: Gold Correction Continues As Safe-Haven Flows Moderate

Gold continued its correction on Tuesday that it began last week and is now down 9.3% from 20 October. It is overbought and participants are taking profits and drivers of safe-haven flows have eased. A US-China trade deal is expected to be formalised on Thursday by Presidents Trump and Xi. It looked through stronger US house price and survey data as a full 25bp rate cut remained priced in for Tuesday’s decision, but not more, and the USD BBDXY fell 0.1%.

- Bullion breached $4000/oz during the APAC session but trading below this level the rest of the day reaching a low of $3886.62, below support at $3900, before recovering to around $3950/60. It finished down 0.8% to $3952.14/oz and has started today around $3947.5.

- The breach of the 20-day EMA at $4045.9 opened up the 50-day EMA at $3838.2. Initial resistance is at $4161.4, 22 October high. Bank of America is forecasting prices to trough around $3800 in Q4 (Bloomberg).

- Bloomberg is reporting that ETFs have cut their gold holdings sharply in recent days.

- The decline in silver prices is seen as corrective and the trend remains bullish. It rose 0.4% to $47.054 on Tuesday to be up 0.9% in October. It fell to $45.557 early in European trading, holding just above the 50-day EMA at $45.542, and then rebounded to $47.268. It has started today around $47.05. Initial resistance is at $49.456, 23 October high.

- Equities were mixed with the S&P up 0.2% but Euro stoxx down 0.1% and the S&P e-mini is currently flat. Oil prices were lower with Brent -1.8% to $64.47/bbl. Copper was flat.