OIL: North Sea BFOET Loadings to Dip to 537kb/d in September

North Sea combined BFOET loadings are scheduled to edge down to 537k b/d in September from 542k b/d in August, according to Bloomberg loading schedules. A drop in Troll loadings to the lowest since September 2024 is set against a recovery in Forties loadings.

- The five main grades of Brent, Forties, Oseberg, Ekofisk and Troll will load a total of 23 cargoes in September, compared to 24 cargoes in August.

- Brent: 1 cargo in September vs 2 in August; 23k b/d down from 45k b/d

- Forties: 7 cargoes vs 4; 164k b/d up from 91k b/d

- Oseberg: 3 cargoes vs 3; 70k b/d up from 68k b/d

- Ekofisk: 10 cargoes vs 11; 233k b/d down from 248k b/d

- Troll: 2 cargoes vs 4; 47k b/d down from 90k b/d

Johan Sverdrup loadings are scheduled to recover to 723k b/d with 21.7mbbl on 20 cargoes in September, compared to 703k b/d in August.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Analyst Views on Further Dollar Depreciation

- *Goldman Sachs: The fast USD depreciation trajectory is very much in line with other large depreciation episodes from the peak. Beyond this point, the move has often become slower and choppier across historical episodes.

- A clearer dovish tilt from the Fed on the back of more visible weakening in the upcoming labour market data could be an important near-term catalyst, sparking further Dollar weakness versus majors such as EUR and JPY.

- Absent that, a more gradual grind weaker in the Dollar is still the most likely outcome, supporting EM carry strategies, and a steady move stronger in CNY, with implications across Asia.

- *JP Morgan cites the main anchors of their bearish USD view remaining unchanged. Specifically, moderation in US growth, global longs in US equities (or assets), growth-supportive fiscal and monetary policies outside the US, and higher probability of a structural USD weakening, which deserves a dollar discount.

- To JPM, conditions are favourable for EM currencies to outperform the US dollar and past experience indicates that once initiated, dollar bear cycles can persist for a while. In their latest FX weekly publication, JPM remain bullish the euro- and Antipodean bloc FX.

- *ING say the balance of risks remains tilted to the downside for the dollar, but their calls for only a gradual slowdown in payrolls and an inflation bump in the coming months imply that markets have overshot on dovish pricing. A September cut may be ultimately priced out, and some short-term support for the dollar should emerge. Conversely, a major payrolls disappointment can send DXY below 96.0 even without the OBBBA and tariff factors.

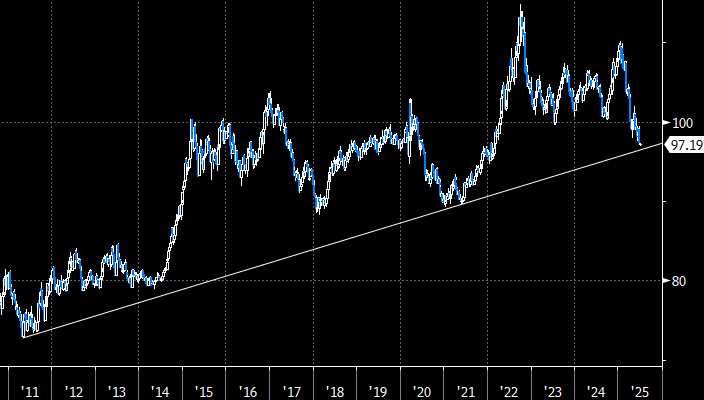

FOREX: Dollar Index Approaching Long-Term Trendline Support

- The dollar index resumed its downtrend last week, closing at its lowest weekly level since February 2022. Price action has propelled the likes of EURUSD above 1.17, GBPUSD above 1.37, while USDCHF has continued to plumb fresh 10-year lows below the psychological 0.8000 mark.

- Analysts have been quick to highlight that the latest greenback selling has notably been paired with an adjustment lower for the front-end of the US curve, which was pertinent alongside a significant reduction in geopolitical risk premia. This dynamic may place a greater focus than usual on this week’s US employment report, notably scheduled on Thursday owing to the July 4th holiday. Using EURUSD as a proxy for the potential dollar move, the break-even on a Thursday straddle sits at +/- 85 pips.

- Interestingly, the long-term uptrendline for the dollar index, drawn across the 2011 and 2021 lows, intersects around 80pips below current levels at 96.40, which remains a key medium-term target for the move. Options pricing might suggest this level as providing solid support on a first test and a potential obstacle to EURUSD’s well-forecasted move towards 1.20.

- With material changes in immigration flows under the Trump administration, breakeven rates of payrolls growth are likely much lower than last year. It should keep focus on the unemployment rate as a broad barometer of labour market slack even if it’s from the noisier household survey. Separately, ISM and JOLTS data will also provide important inputs into short-term expectations for Fed pricing.

Source: Bloomberg Finance L.P. / MNI

SPAIN AUCTION PREVIEW: On offer this week

Tesoro Publico has announced it will be looking to sell a combined E5-6bln of the following Bono/Obis at its auction this Thursday, July 3:

- the 2.40% May-28 Bono (ISIN: ES0000012O59)

- the 3.15% Apr-35 Obli (ISIN: ES0000012O67)

- the 3.50% Jan-41 Obli (ISIN: ES0000012O75)

Tesoro Publico has also announced it will be looking to sell E250-750mln of the the 1.15% Nov-36 Obli-Ei (ISIN: ES0000012O18) at that auction.

Additionally, Tesoro Publico has announced it will be looking to sell a combined E5-6bln of the following letras at its auction tomorrow, July 1:

- the 6-month Jan 9, 2026 letras

- the new 12-month Jul 10, 2026 letras