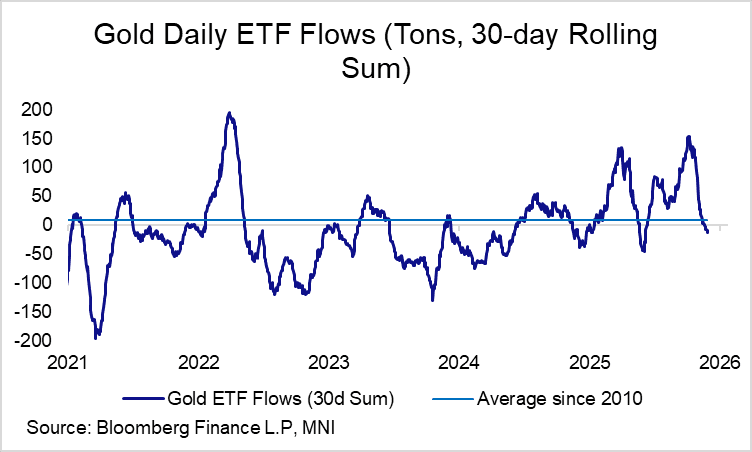

GOLD: Normalisation Of Retail Sentiment Could Support The Next Leg Higher

The 50-day EMA has contained downside in spot gold since the end of August, and remains a key support level. A bullish trend condition remains intact, with the Oct 20 – 28 pullback appearing to have been a correction. Renewed confidence in a Fed cut in December looks to have supported spot over the last week, with the emergence of Kevin Hasset as Fed Chair frontrunner bolstering expectations for easing to continue into next year.

- A reduction in retail account exposure was a key theme through the late-October selloff in gold. The 30-day rolling sum of daily ETF flows is below the 2010-2025 average for the first time since June, suggesting sentiment has normalised after an exuberant post-summer run.

- This provides a cleaner backdrop for those looking to re-engage longs and capture longer-term themes such as central bank reserve diversification and fiscal/monetisation concerns.

- Spot is little changed today at $4,157/oz. Initial resistance is the Nov 13 high at $4,245, clearance of which would expose the all-time high and bull trigger at $4,381.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

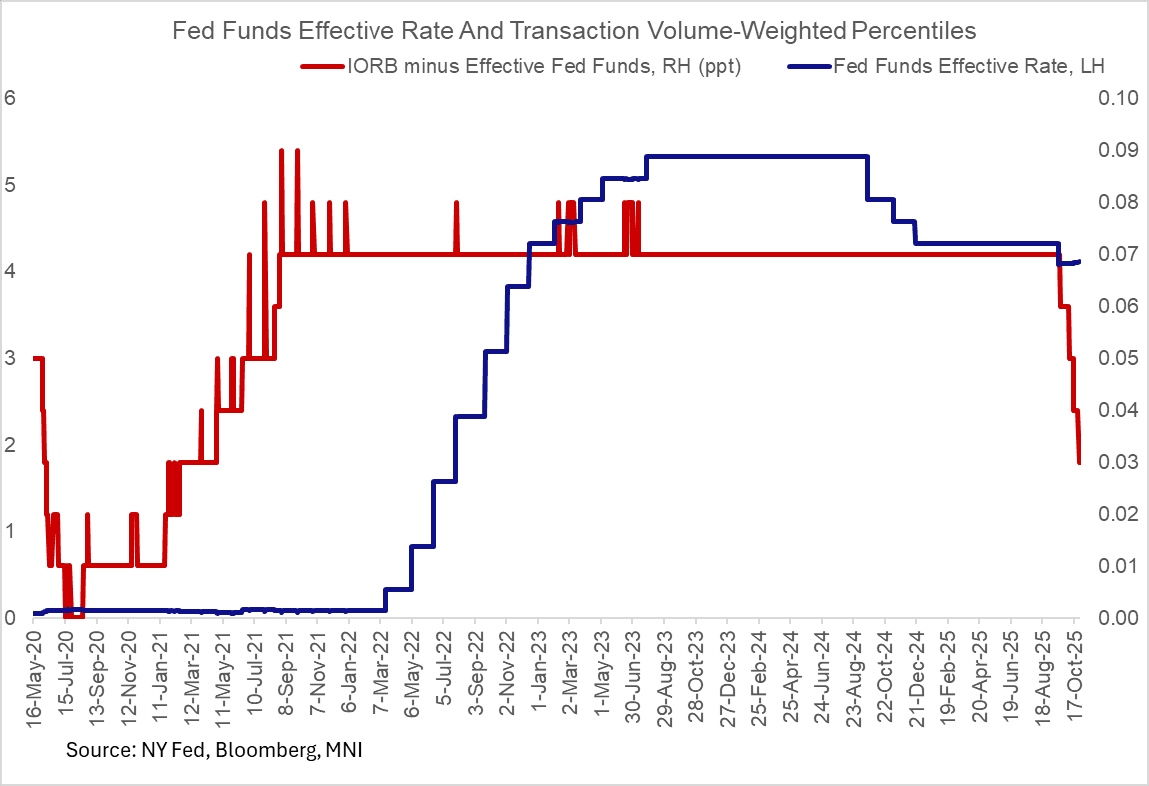

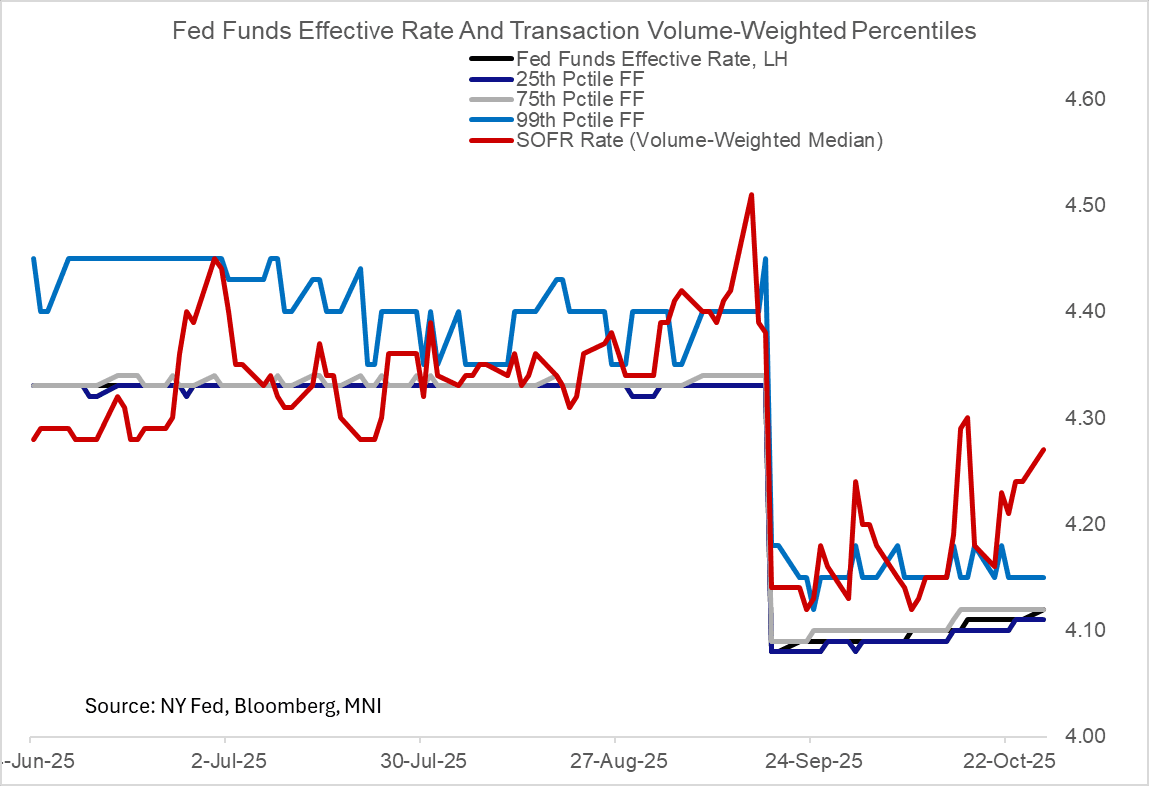

US TSYS/OVERNIGHT REPO: Rate Uptick Bolsters Case For QT End This Week

Money market / repo rates showed a notable uptick Monday, with the prints landing just as the FOMC sat down for its 2-day meeting to decide the next move on balance sheet runoff. SOFR, BGCR, and TGCR all rose 3bp, remaining stubbornly above the Fed's IORB rate suggesting that reserves are less ample than they had been.

- A semi-surprise was the 4th increase in the Fed Funds effective rate since the September FOMC meeting, with a 1bp uptick to 4.12%. That's just 3bp below IORB after having been consistently 7bp below for most of the cycle. This move has been flagged as a risk for several sessions now, with the EFFR percentiles ticking higher (the published EFFR is a volume-weighted median of overnight fed funds transactions).

- As we noted in our Fed meeting preview, we expect the FOMC to end balance sheet runoff this week, as it assesses the reserve regime to have moved from "abundant" to at/near "ample" - the latest rate moves only reinforce the likelihood of a QT end.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.27%, 0.03%, $3019B

* Broad General Collateral Rate (BGCR): 4.24%, 0.03%, $1131B

* Tri-Party General Collateral Rate (TGCR): 4.24%, 0.03%, $1103B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.12%, 0.01%, volume: $88B

* Daily Overnight Bank Funding Rate: 4.11%, no change, volume: $176B

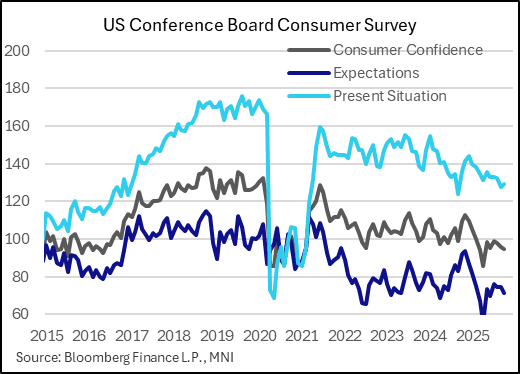

US DATA: Conf. Board Expectations Soft, Current Stable, Inflation Views Stubborn

The Conference Board's October survey largely mirrored weak sentiment seen in other readings, with overall Consumer Confidence falling to 94.6 from 95.6 (rev from 94.2; an 0.8pp drop to 93.4 had been expected). That was a 6-month low and marked a 3rd consecutive deterioration.

- The Present Situation reading improved (129.3, from 127.5 rev from 125.4), diverging from Expectations which fell to a 4-month low (71.5, from 74.4 rev from 73.4).

- As for the latter, consumers were more pessimistic about future business conditions, the labor market, and income prospects - however in what should probably be considered a better indicator of sentiment, respondents' views of current business conditions improved and appraisal of current job availability rose for the first time since December 2024. Overall most major sub-indices were largely steady from the prior month's, with no notable change we could detect in any single category.

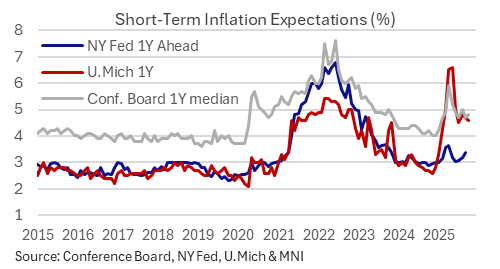

- We note a lack of further disinflationary progress in in 1Y inflation expectations, to an average 5.9% (5.8% prior) and median 4.8% (4.7% prior), keeping both gauges in the elevated range seen since the start of the year.

- Separately we noted a stabilization in the "labor differential" which was still suggestive of the weakest labor market conditions in over 4 years but not a sign of further deterioration in October.

- Conference Board Senior Economist Stephanie Guichard wrote the following of the anecdotal submissions to the report, with tariffs, inflation, jobs, and the federal government shutdown all making appearances: “Consumers’ write-in responses were led by references to prices and inflation, which continued to be the main topic influencing consumers’ views of the economy. References to tariffs declined further this month but remained elevated. Mentions of jobs and employment eased somewhat after picking up in September. The write-in comments remained mostly negative overall, but less so than in previous months. References to US politics were up notably, with the ongoing government shutdown mentioned multiple times as a key concern."

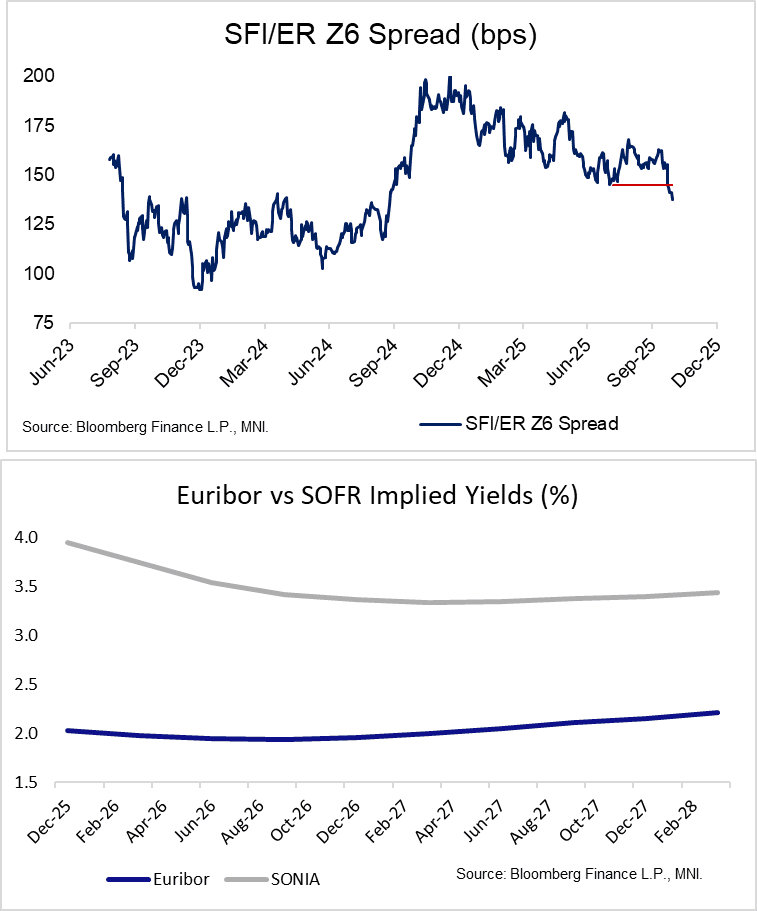

STIR: Raised Bar To Further Near-Term Narrowing In SFI/ER Z6 Spread

The bar to further near-term downside in the SONIA/Euribor Dec’26 spread has likely been raised following this month’s impressive 21bp narrowing. Although recent UK data has driven a warranted repricing at the front of the BOE curve, it is still questionable how far below 3.50% some MPC members will want to take the terminal rate. More data will likely be required to catalyse a fresh dovish move, while the upcoming Nov 26 budget remains a focus for all market participants. Meanwhile, risks to the Euribor-implied terminal rate have become more balanced ahead of the ECB decision, Q3 flash GDP and October flash inflation releases later this week.

- The spread is down another 4bps today to 137bps, comfortably pushing through the previous year-to-date low of 145bps seen in August. Today’s SONIA outperformance has been driven by a soft BRC shop price index print overnight (in particular a pullback in food inflation), alongside spillover from the Gilt market on the latest OBR/fiscal developments (see earlier posts for more colour).

- The SONIA Z6 future has rallied almost 30 ticks since October 10, but the May 1 high at 96.70 has still contained upside for now.

- Meanwhile, the Euribor Z6 future is back at 98.04, after reaching a multi-month high of 98.16 on October 17. The stronger-than-expected October flash PMIs have driven the unwind of early-October dovish repricing. Although some signals from policymakers and MNI’s ECB sources suggest risk to near term inflation and activity data are tilted to the downside, President Lagarde will likely strike a balanced tone at Thursday’s decision.