SCANDIS: NOKSEK Up 1.5% This Week, But Still Shy Of Key Resistance

NOKSEK is up 0.45% today at 0.9499, now 1.5% above Monday’s 0.9354 low. After selling off sharply in late-June (a combination of a dovish Norges Bank decision, pullback in brent crude and a technical break), the cross has consolidated between 0.9329 (June 26 low) and 0.9542 (July 3 high). A clear break of the July 3 high is required to signal a bullish theme.

- This week’s positive momentum has been a function of:

- Crude oil futures jumping on the new early August deadline for a Russia/Ukraine ceasefire, after Trump yesterday gave Russia 10 more days to halt fighting.

- Digestion of the weekend EU-US trade agreement. Although this reduces near-term policy uncertainty, it will exert a toll on Sweden’s export-sensitive economy.

- The weak Swedish flash Q2 GDP reading (0.1% Q/Q vs 0.3% cons). While the flash indicator should be taken with a handful of salt, the broad message of subdued growth momentum is supportive of market expectations for one more Riksbank cut this year.

- Swedish consumer confidence saw a notable improvement to 90.7 in July (vs 84.9 prior) this morning, but this wasn’t a market mover.

- EURNOK is down 0.2%, piercing support at the 50-day EMA (11.7647 today) at typing. A clear breach of this average would expose 11.6946, the 50% retracement of the June 18 - July 17 rally.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

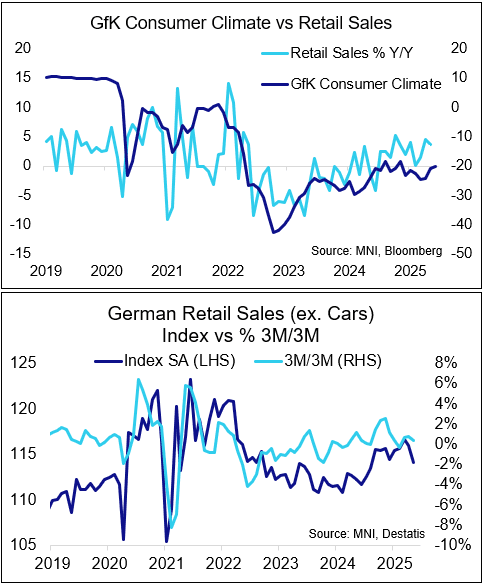

GERMAN DATA: May Retail Sales Underscore Disappointing Consumer Sector

German May Retail Sales came in at -1.6% M/M (real, seasonally-adjusted) underperforming vs consensus of -0.5%, even considering a 0.5pp upward revision to the April data (to -0.6% M/M; 0.2pp of that revision was already known). On a 3m/3m comparison, retail sales printed +0.3% in May - underscoring that on a broader view, since mid-2024, retail sales have seen no gains in Germany.

- Sentiment in the consumer sector has been lagging recent upticks in the business sector - the GfK consumer climate continues to print well in negative territory, at around -20 for a couple of months now, so the outlook here remains subdued.

- Looking at the individual categories, May's decrease appears broad-based, with food sales down 1.3% M/M, and non-food sales down 2.2%.

STIR: J.P.Morgan Recommend Buying SFRU5 95.875 Puts Vs. ERU5 98.125 Puts

Late on Friday J.P.Morgan recommended buying SFRU5 95.875 puts vs. ERU5 98.125 puts, given their view on risks surrounding ECB and Fed pricing, while they are also wary of upside surprises in this week’s U.S. labour market data.

CROSS ASSET: MONTH END EXTENSIONS

Bond extensions are small for this Month.

Bloomberg Bonds:

- US Tsys: +0.07yr (small).

- EU Govies: +0.06yr (small).

- UK Govies: -0.04yr (non event).

MS Bonds:

- US Tsys: +0.04yr (small).

- EU Govies: +0.05yr (small).

- UK Govies: -0.03yr (non event).

Barclays FX:

- They see moderate USD selling vs most Majors, weaker against the EUR.

CITI FX:

- They see moderate USD selling, but weaker signal vs the GBP.

BofA FX:

- They see rebalancing flows into the USD and GBP.